The Plate Fraud Playbook: Five Categories of UAE Plate Fraud and How Each One Actually Works

April 14, 2026

Dubai

LicensePlate.ae Team

This is how plate fraud works in the UAE in 2026. Not dramatically. Not through shadowy actors in back rooms. Through social media accounts that look professional, listings that feel plausible, prices that are credible enough to generate emails but attractive enough to generate movement, and payment requests that look exactly like the payment requests of legitimate brokers. The scale is real: the UAE Financial Intelligence Unit reported AED 1.2 billion in total fraud losses between 2021 and 2023, with vishing, phishing, and smishing cited as the dominant categories. In April 2024 alone, Dubai Police arrested 494 individuals across 406 separate fraud cases. Plate fraud is a small subset of that total, but it is real, growing, and largely invisible to casual buyers until it happens to them.

This article is the investigative companion to our existing plate scams safety guide. The safety guide tells you what to do to stay safe. This article tells you what is actually happening mechanically when fraud occurs, which is a different question. If you understand how the five categories of UAE plate fraud work at a structural level, you stop treating fraud as a single undifferentiated threat and start treating it as five specific threats with five specific countermeasures. You also stop protecting against the category that almost never happens (fake physical plates, which fail ANPR and Salik gantries within hours) and start protecting against the category that actually does (registration misrepresentation, which is invisible without specific due diligence).

Below, the five categories in order of prevalence. For each, we describe the mechanics, the named case history, the verification steps that stop it, and the reporting channel to use if it has already happened to you. A full pre-transaction verification workflow is laid out in our complete plate due diligence checklist, and every fraud vector here ultimately closes the same way: you do not pay until the RTA traffic file has been checked against the seller’s Emirates ID in front of you.

The Scale of UAE Plate Fraud in 2026, Stated Plainly

Before the categories, the numbers that define the problem. These figures come from primary UAE government sources and established cybersecurity reporting, and they set the context for everything that follows.

AED 1.2 billion ($326 million) in total fraud losses recorded by the UAE Financial Intelligence Unit between 2021 and 2023, with phishing, smishing, and vishing identified as the dominant vectors. This is the total across all fraud categories, not plate-specific, but plate fraud uses the same attack infrastructure as the rest.

494 arrests across 406 cases by Dubai Police in April 2024 alone, covering the full fraud landscape. Plate fraud arrests are included in this number but not separately disclosed. The pattern of enforcement action is monthly, not one-off.

144+ domains identified by Resecurity in December 2024 as infrastructure for the Smishing Triad campaign impersonating Dubai Police. The same infrastructure is reused across UAE consumer fraud categories, including plate-adjacent scams.

AED 109 million cleared in a single RTA auction in December 2025 across 90 plates. This is the legitimate market. It also establishes the scale of cheques that plate fraud attempts to redirect. When a single auction evening moves AED 100 million of verifiable capital, the fraud attempting to intercept adjacent flows does not need to be large to be damaging.

Up to AED 3 million in fines plus deportation for foreign nationals convicted of cybercrime offences under Federal Decree-Law 34 of 2021 on Countering Rumours and Cybercrimes. The penalty framework is real. Enforcement is active. The legal ceiling is high enough to deter most organised operators and to provide meaningful recovery in cases where perpetrators can be identified and traced.

The takeaway: plate fraud in the UAE operates inside a well-resourced enforcement environment with serious penalties, but the enforcement activates after the fact. Prevention is the reader’s responsibility, and prevention requires understanding the five categories below.

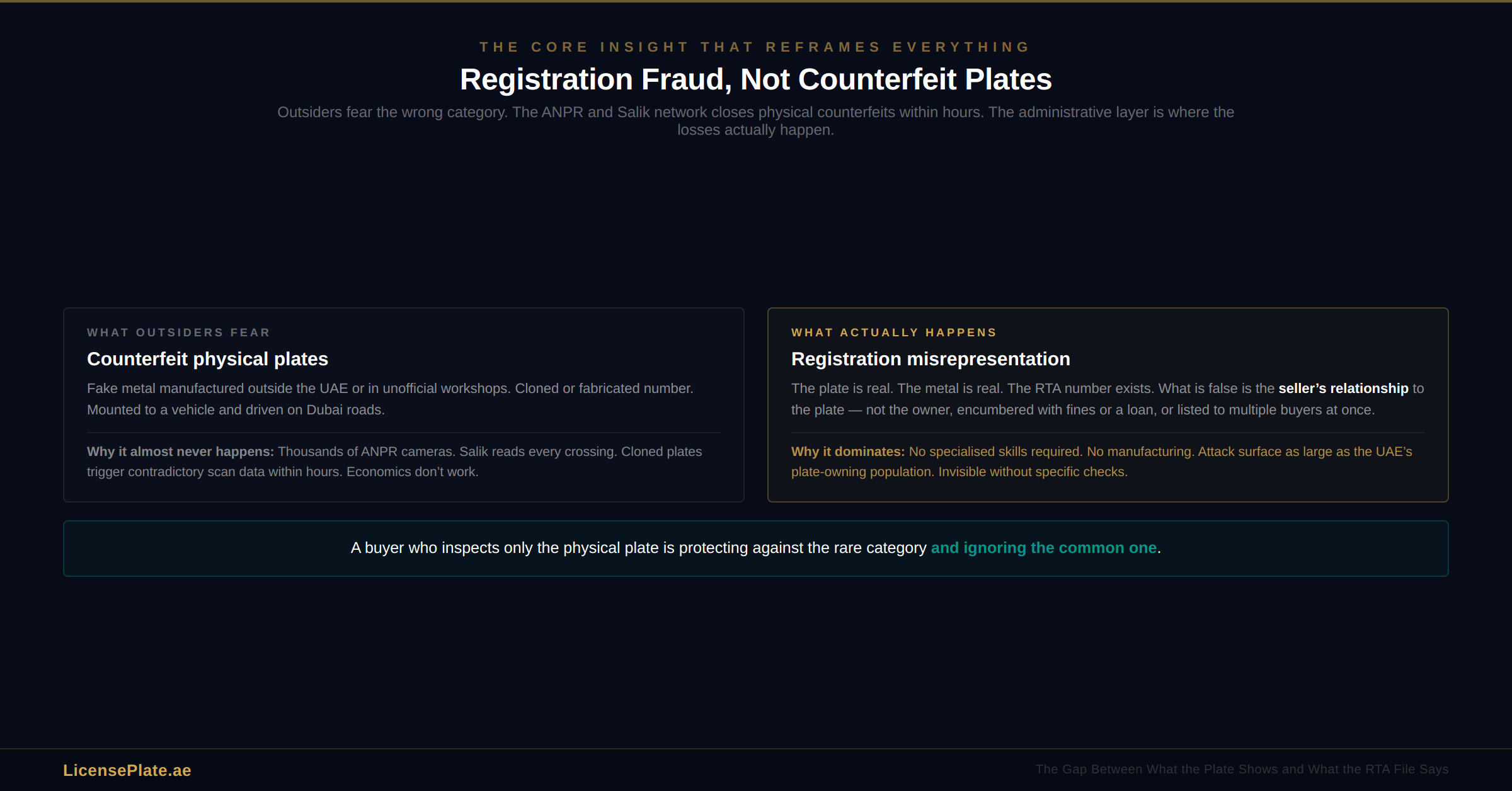

The Core Insight: Registration Fraud, Not Counterfeit Plates

The Core Insight: Registration Fraud, Not Counterfeit PlatesHere is the piece of analysis that separates this article from every other UAE plate safety piece written to date. The category of fraud that outsiders and first-time buyers fear most — someone manufacturing a fake physical plate and selling it as real — is the category that almost never happens at meaningful scale. The reason is structural. The UAE has one of the densest Automatic Number Plate Recognition networks in the world. Dubai alone operates thousands of ANPR cameras across its road network. Salik toll gantries read plates at every crossing. Every RTA-registered vehicle is scanned dozens of times a day. A counterfeit physical plate that does not match a real traffic file will generate inconsistencies within hours and trigger a police investigation within days. The economics of manufacturing and moving counterfeit plates in a jurisdiction with this level of real-time plate verification do not work.

The fraud that actually happens is registration fraud, the administrative layer where the ownership record, the fines status, the mortgage status, or the seizure flag of a plate is misrepresented between buyer and seller. The plate is real. The metal is real. The number on it exists in the RTA traffic file. What is false is the relationship between the seller and the plate. The seller does not own it. Or the seller owns it but it is encumbered (unpaid fines, a loan against it, a court-ordered seizure). Or the seller owns it clean but is selling simultaneously to multiple buyers and plans to transfer to whoever pays first while cashing the deposits of the others. All of these vectors exploit the gap between what the physical plate shows (a legitimate UAE plate) and what the RTA traffic file actually says (encumbered, disputed, or not the seller’s to sell).

A buyer who inspects only the physical plate and agrees to pay is protecting against the rare category and ignoring the common one. A buyer who runs the plate through the RTA traffic file, cross-references it to the seller’s Emirates ID, and confirms zero encumbrances before transferring money is protecting against the category that actually matters. The verification workflow is not optional. It is the entire defence against 80%+ of UAE plate fraud. Our cross-emirate transfer guide and sell-your-car guide both walk through the RTA verification mechanics in full operational detail.

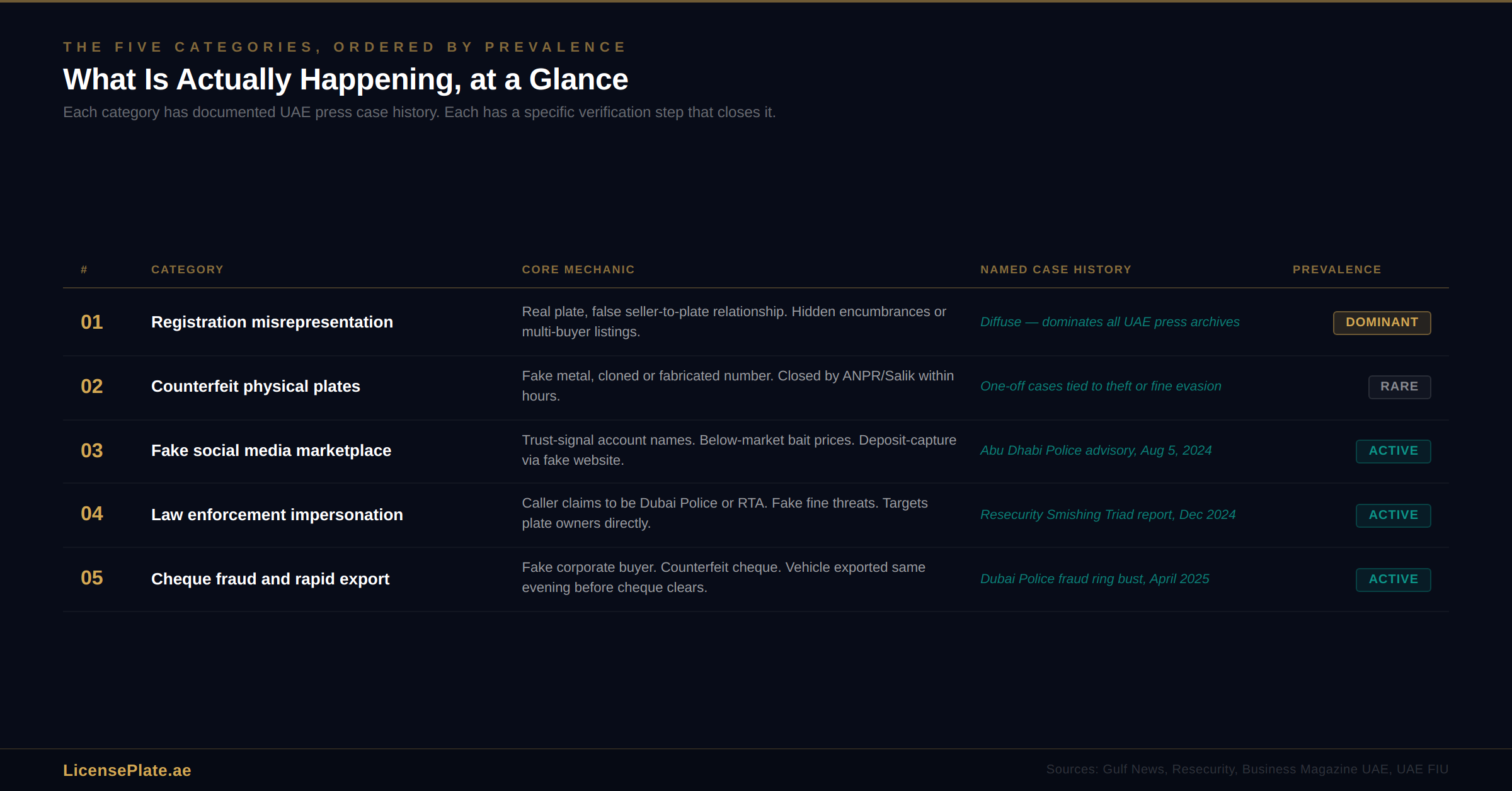

Category 1: Registration Misrepresentation (The Most Common Vector)

How it works mechanically

A seller lists a plate through a classifieds site, a WhatsApp group, or a social media account. The plate exists. The plate number is real. The seller’s Emirates ID is real. What is false is one of three things. First, the plate is not in the seller’s traffic file — it belongs to a family member, a former spouse, or a partner in a business dispute, and the seller does not have the authority to transfer it. Second, the plate is in the seller’s traffic file but is encumbered — unpaid Salik, unpaid Dubai Police fines from previous vehicles, a bank loan against the plate, or a court-ordered seizure flag that prevents transfer until settled. Third, the plate is clean but the seller has listed it on three platforms simultaneously and plans to transfer to whichever buyer pays fastest while absorbing the deposits of the others.

Why it is the most common category

This category dominates because it requires no specialised skills, no counterfeit manufacturing, and no social engineering beyond a credible listing. The seller has a real plate somewhere in their family or business circle. They list it. They take deposits. They either transfer (leaving one buyer holding a plate worth less than expected due to hidden encumbrances) or vanish (leaving multiple buyers fighting over a deposit pool). The attack surface is exactly as large as the UAE’s plate-owning population, which is in the millions. The category also feeds directly into several of the ten expensive mistakes first-time plate buyers make, because first-time buyers are the segment least likely to demand traffic-file verification before paying.

How to spot it

Three verification steps stop this category entirely. Run the plate through the Dubai Drive app using UAE Pass. Confirm the Emirates ID of the person transferring the plate matches the name on the traffic file. Check for outstanding fines or encumbrance flags before paying the full amount. A seller who refuses any of these three steps is functionally identifying themselves as a fraud risk. Legitimate sellers welcome verification because verification closes the transaction. Our pre-transaction due diligence checklist runs through the exact sequence.

Legal recourse

Registration misrepresentation falls under Federal Decree-Law 34 of 2021 on Countering Rumours and Cybercrimes if the listing was digital, and under the UAE Penal Code for in-person transactions. Penalties include fines up to AED 3 million and, for foreign nationals, deportation as an additional sanction. Report through the for Dubai-based incidents, or through the MOI eCrime service (www.moi.gov.ae) for incidents crossing emirate boundaries.

Category 2: Counterfeit Physical Plates (The Category That Rarely Happens)

How it works mechanically

A physical plate is manufactured outside the UAE or through an unofficial local workshop. The plate carries a number and code that either matches a real UAE traffic file (cloning) or is entirely fabricated (forgery). The plate is physically mounted to a vehicle. The vehicle is driven on UAE roads.

Why it is rare in practice

The ANPR and Salik infrastructure catches cloned and forged plates fast. A cloned plate produces contradictory scan data (the same plate recorded at two physically impossible locations), which flags for investigation. A forged plate with a fabricated number produces no traffic file match, which flags on the first toll gantry read. The Dubai Police’s implementation of blockchain-based evidence storage in 2025 has further tightened the digital evidence chain, making cloned or forged plate cases easier to investigate and harder for defendants to dispute. The economics do not work for sustained operations. Most counterfeit plate cases in UAE press archives involve one-off incidents tied to vehicle theft or evasion of specific fines, not organised fraud against plate buyers.

Why it still matters to buyers

It still matters because an individual buyer presented with a physical plate cannot tell by looking whether the plate matches the traffic file the seller claims. The defence is identical to Category 1: verify the plate in the official system, confirm the traffic file identity, refuse to accept the physical plate as evidence of ownership. A plate that cannot be verified digitally is not a plate you should pay for, regardless of how real the metal looks.

Legal recourse

Counterfeit plate manufacture and use falls under the UAE Penal Code’s provisions on forgery and impersonation, with penalties that can include imprisonment. If a buyer has received a counterfeit plate through a transaction, the primary reporting channel is the Dubai Police Anti-Fraud Centre of the Criminal Investigation Department, which handled the April 2025 fraud ring case involving counterfeit cheques and rapid vehicle export. For non-Dubai incidents, report through the Ministry of Interior’s eCrime portal or through the Abu Dhabi Police Aman Service (8002626).

Category 3: Fake Social Media Marketplace (The Category Abu Dhabi Police Named in 2024)

How it works mechanically

An Instagram, TikTok, Facebook, or WhatsApp account is created with professional-looking branding. The account name incorporates trust signals (“Dubai Plates Official,” “Abu Dhabi Premium Numbers,” names that mimic legitimate brokers). The account posts listings with real photographs of real plates sourced from legitimate auction coverage or other platforms. Prices are set credibly below market — not low enough to be implausible, but attractive enough to generate inquiries. When a buyer engages, the account directs them to a website (often hosted on a newly-registered domain that mimics a government or broker URL) to pay a deposit or a full amount. The website accepts the payment. The plate does not exist. The account deactivates. The website goes offline within 48 hours. A buyer who first runs the listed plate through our Dubai plate price check would see the gap between the bait price and the actual market range immediately.

The Abu Dhabi Police case

This is the exact pattern Abu Dhabi Police warned about in August 2024, naming distinctive Abu Dhabi plates as the specific bait and hefty deposits as the specific monetisation mechanism. For Abu Dhabi-specific buyers, our complete Abu Dhabi plate guide covers the legitimate TAMM verification pathway and the DMT’s September 2025 rules requiring clear ownership certificates for distinguished plates. The UAE Government Cyber Security Council has issued parallel warnings about phishing scams that use exaggerated offers and imaginary deals as bait. The infrastructure for this category overlaps directly with the Smishing Triad operation documented by Resecurity in December 2024, which used 144+ short-lifespan domains to impersonate Dubai Police for fake fine payments. The same actor infrastructure is reusable for plate-specific variants.

How to spot it

Four tells, any one of which is enough. First, the account has fewer than six months of posting history or high-velocity follower growth inconsistent with a legitimate business. Second, the account directs buyers off-platform to a website for payment rather than using a verified escrow or RTA transfer process. Third, the website’s domain was registered recently (WHOIS lookups are free). Fourth, the seller asks for a deposit before any verification step involving the RTA system. Real brokers and platforms complete plate verification before payment, not after. If you are being asked to pay first and verify later, you are in Category 3. A cross-check through our guide to checking any plate’s value online will surface the authentic price band for the specific plate in question within minutes.

Legal recourse

This category falls cleanly under Federal Decree-Law 34 of 2021 because the fraud occurs entirely in digital space. Report through the Dubai Police eCrime portal with full evidence (screenshots of the account, the listing, the website, the payment transaction). Include the WHOIS data for the domain if you can access it. The Dubai Police Anti-Fraud Centre and the MOI’s cybercrime unit coordinate actively. Recovery timelines for large-scale fraud are 2–3 months according to UAE cybercrime legal practice, but the case numbers are real and the pipeline is active.

Category 4: Law Enforcement Impersonation and Fake Fine Vishing

How it works mechanically

This is not strictly a plate-buyer fraud, but it targets plate owners and it uses the plate registration system as leverage. A caller identifies themselves as a Dubai Police officer, RTA inspector, or Ministry of Interior representative. They claim the victim has outstanding traffic fines, unpaid Salik, or a registered plate that has been flagged for investigation. They demand immediate payment to a specified bank account or a linked online portal, under threat of vehicle seizure, licence revocation, or travel ban. The victim, confronted with the official-sounding threat against assets they actually own, pays. The caller vanishes.

The documented case

Resecurity’s December 2024 report on the Smishing Triad includes a full transcript of one such call. The fraudster spoke with an Indian accent against typical call-centre background noise. He introduced himself as an inspector. He instructed the victim to check a mobile inbox where he had sent a fabricated investigation file number. He threatened licence revocation and vehicle seizure. The tooling, Resecurity established, was offered by a Chinese-speaking threat actor on Telegram, with operational members from Indonesia, Vietnam, and other jurisdictions. The infrastructure uses inexpensive generic top-level domains registered in volume. Infosecurity Magazine’s coverage of the same campaign noted a detected spike in fraudulent activity around UAE National Day (Eid Al Etihad, December 2–3).

How to spot it

Dubai Police, RTA, and MOI never request payment over the phone. Full stop. Any caller who claims authority and demands immediate payment is operating Category 4 fraud regardless of how convincing the scripting is. Real UAE enforcement contacts via official channels: the Dubai Police app, the MOI UAE mobile app, registered SMS from short codes, or physical letters. Real fines can be checked by the citizen themselves through the Dubai Drive app or the Ministry of Interior e-services portal. If you suspect a fine is real, hang up, open the official app, and check for yourself. If the fine exists, you can pay through the app. If it does not exist, you have just defeated the fraud.

Legal recourse

Law enforcement impersonation is covered by Federal Decree-Law 34 of 2021 with some of the heaviest penalties in the UAE cybercrime framework, because the impersonation of a government authority is treated as an aggravating factor. Report immediately through the Dubai Police eCrime portal (ecrime.ae) or the Aman Service on 8002626. Do not engage with the caller. Do not attempt to string them along. Hang up, preserve screenshots of any SMS or email, and report within 24 hours for the best case trace.

Category 5: Cheque Fraud and Rapid Export (The April 2025 Dubai Police Case)

How it works mechanically

This category inverts the buyer-fraud pattern. Here the seller is the victim and the fraudster is the buyer. A buyer contacts a seller (usually a car-and-plate listing on a well-known online marketplace) and expresses interest in a premium vehicle that includes a distinctive plate. The buyer presents themselves as representing a reputable company. Payment is made via counterfeit cheque. The ownership transfer completes. The buyer uses the newly registered ownership documents to export the vehicle overseas the same evening. When the seller attempts to cash the cheque within the standard 2–3 business day clearing window, the cheque fails. By that point the vehicle is already in transit, outside UAE jurisdiction, and the new registration has been administratively severed. The plate, if it was a distinctive one, may have been transferred off the vehicle before export. The target profile for this category skews toward cars and plates that change hands at premium prices, the tier that shares an economic band with the Most Noble Number 2026 auction lots, though these fraud attempts happen in the private market rather than at public auction.

The Dubai Police ring case

Dubai Police broke up exactly this operation in April 2025. Business Magazine UAE’s coverage documented the mechanics: one suspect called sellers pretending to be a corporate purchasing agent, a second pretended to be a corporate representative to complete the transfer, counterfeit cheques were presented, the vehicles were exported the same evening, and victims only discovered the fraud when cheques bounced. The Anti-Fraud Centre of the Criminal Investigation Department investigated and the ring was dismantled. The case establishes the pattern: this is a professional operation targeting premium listings and requiring professional countermeasures from sellers.

How to spot it (as a seller)

The tells are specific. First, any buyer who insists on completing the transfer before the cheque has cleared is operating Category 5, regardless of how credible the corporate credentials appear. Second, any buyer who requests immediate same-day export documentation is operating Category 5. Third, any buyer who declines to use bank-certified drafts or direct bank transfer and insists on a personal or corporate cheque is operating Category 5. The defence is simple: do not transfer ownership until payment has cleared. Bank transfer with confirmed receipt is the safest mechanism. Certified bank drafts are acceptable. Personal cheques and corporate cheques from unverified entities are not acceptable payment for vehicles with premium plates.

Legal recourse

Cheque fraud is covered under both Federal Decree-Law 34 of 2021 (for the digital elements of the operation, including impersonation and fabricated documentation) and the UAE Commercial Transactions Law (for the bounced cheque itself). Rapid export complicates recovery because the vehicle is outside UAE jurisdiction, but the Dubai Police Anti-Fraud Centre coordinates with Interpol for cross-border cases and has documented success rates in similar operations. File the complaint immediately — the first 24 hours after discovery are the most valuable for tracing.

The Verification Stack That Stops All Five Categories

Each of the five categories is closed by a specific verification step. Taken together, the five steps form a single pre-transaction workflow that a buyer or seller can run through in about fifteen minutes and that eliminates the overwhelming majority of fraud risk. This workflow is our complete due diligence checklist in compressed form.

Step 1: Run the plate in the official RTA system. Use the Dubai Drive app via UAE Pass, or visit a Customer Happiness Centre at Umm Ramool, Al Barsha, or Deira. Confirm the plate exists in the RTA traffic file. Confirm the registered owner’s name. For Abu Dhabi plates, use the TAMM platform (tamm.abudhabi). For other emirates, use the Ministry of Interior portal or the respective emirate’s traffic department.

Step 2: Cross-reference the Emirates ID. The name on the RTA record must match the name on the seller’s Emirates ID. If it does not match, the transaction cannot legally proceed regardless of any paperwork the seller provides. Spouses, business partners, and family members sometimes claim authority to transfer on behalf of the registered owner; treat these claims as red flags and require the actual owner’s presence for the transfer.

Step 3: Check for encumbrances. Unpaid Salik, outstanding Dubai Police fines, bank loans against the plate, and court-ordered seizure flags all prevent transfer and all transfer to the new owner if not resolved before purchase. The seller must resolve every encumbrance before transfer. Pay only the pre-transfer agreed deposit (if any) until encumbrances are fully cleared.

Step 4: Verify the sales channel itself. A platform like LicensePlate.ae or a broker with a verifiable UAE trade licence operates under Department of Economic Development oversight and is accountable in ways that Instagram accounts and WhatsApp groups are not. Check for the trade licence number. Verify the company exists. If the transaction is peer-to-peer, require in-person meetings at an RTA centre for the transfer itself. For any plate where the asking price feels off in either direction, run it through the LicensePlate.ae plate calculator to anchor the negotiation in a defensible valuation band before you commit.

Step 5: Use traceable payment. Bank transfer with confirmed receipt, UAE Pass-verified platform payments, or certified bank drafts only. Personal cheques, corporate cheques from unverified entities, crypto, and cash transfers above AED 55,000 (which triggers UAE anti-money-laundering reporting under Federal Decree-Law 20 of 2018) should all be declined. Traceable payment is both a fraud defence and a legal protection.

Running all five steps takes fifteen minutes for a typical transaction and longer only when the plate is high-value enough to warrant additional checks. The fifteen minutes are the single best investment any UAE plate buyer or seller can make.

The Complete Legal and Reporting Framework

If fraud has already happened, the UAE’s legal framework is active, penalties are substantial, and reporting channels are accessible. Know them in advance so you do not have to find them in a panic.

The governing law

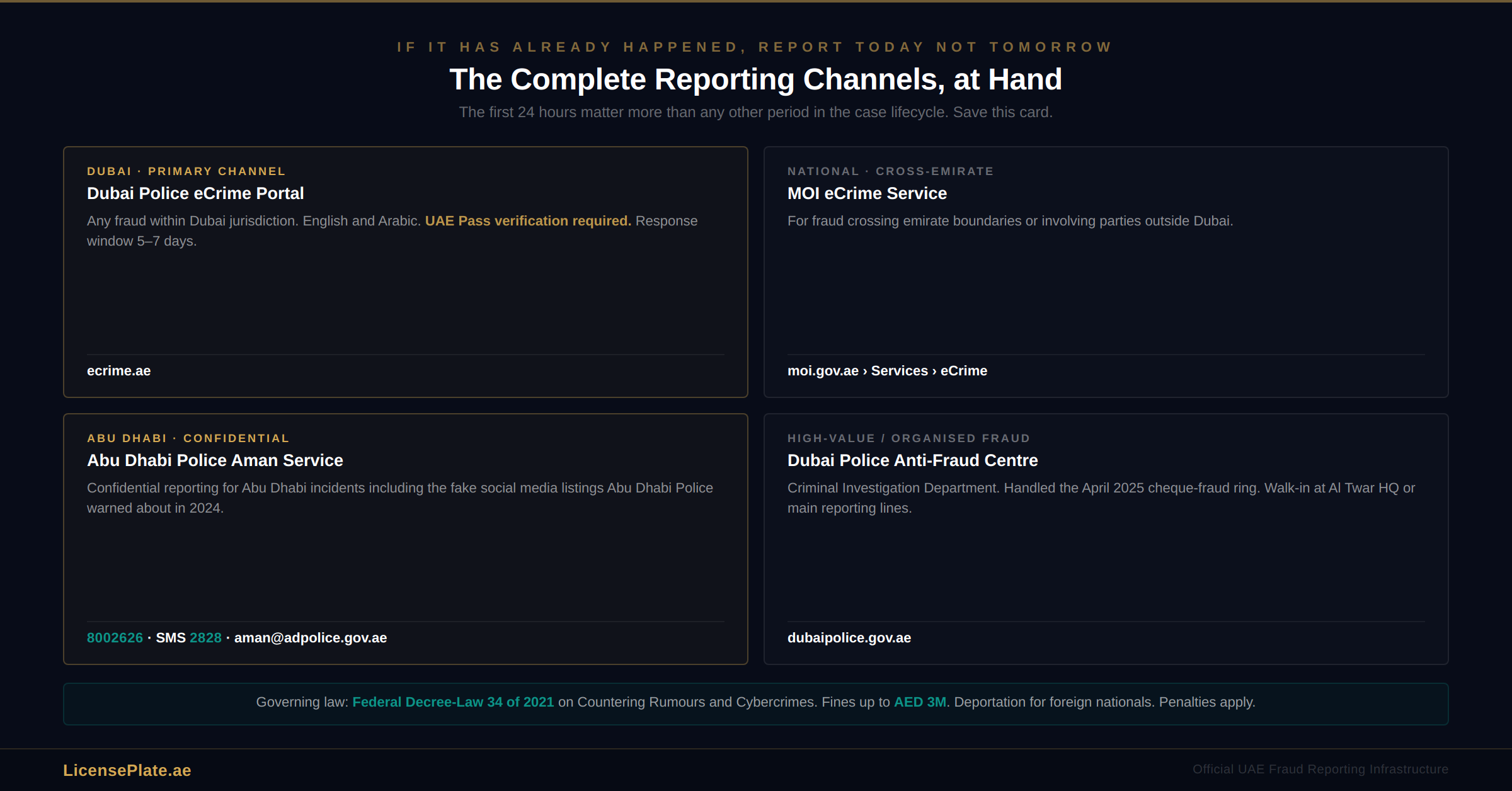

Federal Decree-Law 34 of 2021 on Countering Rumours and Cybercrimes is the primary instrument for any plate fraud that occurs in digital space (which is most of it). Penalties include fines up to AED 3 million, imprisonment for serious categories, and — for foreign nationals — deportation as an additional sanction. The law covers fraud, identity theft, impersonation of authority, phishing, smishing, and vishing. For in-person fraud, the UAE Penal Code applies with parallel penalties. The UAE Commercial Transactions Law adds the specific framework for cheque fraud under Category 5.

The reporting channels

Dubai Police eCrime portal (ecrime.ae). Primary channel for any fraud within Dubai jurisdiction. Accepts complaints in English and Arabic. Requires UAE Pass verification. Response window is 5–7 days.

Ministry of Interior eCrime service (www.moi.gov.ae). National channel for cross-emirate fraud or fraud involving parties outside Dubai. Same UAE Pass verification, same 5–7 day response window.

Abu Dhabi Police Aman Service. Call 8002626, SMS to 2828, or email aman@adpolice.gov.ae. The confidential reporting channel for Abu Dhabi-based incidents, including the specific category of fake social media plate listings.

Dubai Police Anti-Fraud Centre, Criminal Investigation Department. For high-value cases and organised fraud rings. This is the unit that handled the April 2025 cheque fraud case. Accessible through the main Dubai Police reporting lines and through direct walk-in at Dubai Police headquarters in Al Twar.

UAE Government Cyber Security Council. Publishes ongoing public advisories on active fraud patterns. Follow for early warning of new campaigns and new tactics.

The evidence to preserve

For any report, the UAE cybercrime reporting process requires specific evidence that a well-prepared victim will have ready. Screenshots of every listing, message, and website. The seller’s claimed name, phone number, Emirates ID details, and social media handles. Bank statements showing the attempted or completed transaction. WHOIS data for any website involved. Any audio recordings of phone calls (UAE law permits recording calls to which you are a party for evidence purposes). Case reference numbers from any prior interactions with the fraudster. The more complete the evidence package at filing, the faster the case processes.

Frequently Asked Questions

Q: What is the single most common type of UAE plate fraud in 2026?

Registration misrepresentation, where the plate is real but the seller’s relationship to the plate is false. The seller may not own the plate, the plate may be encumbered with unpaid fines or a bank loan, or the seller may be listing the plate to multiple buyers simultaneously. Verification through the RTA traffic file against the seller’s Emirates ID stops this category entirely.

Q: Are fake physical UAE plates a real risk?

Rare in practice. The UAE’s ANPR and Salik infrastructure catches cloned and forged plates within hours because the plate either produces contradictory scan data or no traffic file match at all. The economics of counterfeit plate manufacturing do not work in a jurisdiction with real-time plate verification. The buyer-side defence is identical to Category 1 registration fraud: verify the plate in the official RTA system before paying.

Q: What did Abu Dhabi Police warn about in August 2024?

Abu Dhabi Police issued a public advisory on August 5, 2024, warning against fake social media accounts offering distinctive Abu Dhabi plates at prices below the actual auction range. Victims were being directed to fake websites to pay deposits for plates that did not exist. The pattern has recurred multiple times since the original advisory, with new fake accounts replacing ones that get taken down. Readers unfamiliar with what “distinctive” means in the Abu Dhabi context can consult our visual decoder for UAE plate codes to see what authentic premium plates look like, and our complete Dubai plates guide for the equivalent breakdown of the Dubai market.

Q: What is the Smishing Triad and does it target plate owners?

The Smishing Triad is a cross-border fraud operation documented by cybersecurity firm Resecurity in December 2024. It uses 144+ short-lifespan domains to impersonate Dubai Police and extract payments for fake traffic fines. It targets anyone with a UAE phone number, which includes most plate owners. The operation is run by Chinese-speaking actors on Telegram with operational members in multiple countries. The toolkit has been documented and the reporting infrastructure is known.

Q: What is the maximum penalty for plate fraud in the UAE?

Under Federal Decree-Law 34 of 2021, fines can reach AED 3 million plus imprisonment for serious categories. Foreign nationals convicted under the law typically face deportation as an additional penalty. In-person fraud covered under the UAE Penal Code can carry parallel penalties. Cheque fraud (Category 5) adds specific provisions under the UAE Commercial Transactions Law. The penalty ceiling is high enough that organised operations treat UAE enforcement seriously.

Q: How do I report UAE plate fraud if it has already happened to me?

For Dubai-based incidents, use the Dubai Police eCrime portal (ecrime.ae) with UAE Pass verification. For cross-emirate incidents, use the Ministry of Interior eCrime service through www.moi.gov.ae. For Abu Dhabi incidents specifically, call the Aman Service on 8002626, SMS 2828, or email aman@adpolice.gov.ae. Response windows are 5–7 days. For high-value or organised fraud, escalate directly to the Dubai Police Anti-Fraud Centre of the Criminal Investigation Department.

Q: Can I recover funds lost to UAE plate fraud?

Recovery is possible and documented. The April 2025 Dubai Police cheque fraud ring case resulted in arrests and prosecution. The critical factor is reporting speed — the first 24 hours after discovery are the most valuable for tracing. If funds moved through a UAE bank, tracing is faster. If the transaction involved cryptocurrency or overseas accounts, timelines extend and Interpol coordination may be required. Recovery timelines for large-scale fraud typically run 2–3 months.

Q: Is buying from social media accounts ever safe for UAE plates?

Social media can be the entry point for finding a listing, but the transaction itself must move off-platform to a verified RTA process. A legitimate seller found through Instagram or WhatsApp will welcome an in-person meeting at an RTA Customer Happiness Centre, will show their Emirates ID, and will allow a pre-payment verification check through the Dubai Drive app. A seller who insists on completing the transaction entirely within the social platform or on a separately-linked website is operating one of the five fraud categories. The platform is not the risk. The absence of RTA verification is the risk.

Q: Does using a platform like LicensePlate.ae eliminate fraud risk?

It substantially reduces risk by placing the transaction inside a Department of Economic Development-licensed commercial framework rather than an informal peer-to-peer one. The platform verifies listings, operates under UAE commercial law, and provides escrow or verified-transaction mechanisms. The buyer’s pre-transaction verification responsibilities remain (Steps 1–5 of the verification stack above), but the platform accountability adds a layer that Instagram and WhatsApp sellers cannot provide. Our comparison of RTA auction versus secondary market trade-offs walks through the channel choice in full.

Q: What should a seller do to protect against Category 5 cheque fraud?

Never transfer ownership until payment has cleared. Bank transfer with confirmed receipt is the safest mechanism. Certified bank drafts from recognised UAE banks are acceptable. Personal cheques and corporate cheques from unverified entities are not acceptable payment for vehicles with premium plates. Any buyer who insists on completing the transfer before cheque clearance or who requests immediate same-day export documentation is operating Category 5 fraud. The verification workflow is the same whether you are buying or selling: use traceable payment, verify identity, run the RTA checks, and only transfer when payment is confirmed.

A Final Thought, Returning to the August 2024 Advisory

Abu Dhabi Police published their warning in August 2024 and the fake accounts came back within a month. This is the permanent condition of UAE plate fraud in 2026. The enforcement is real. The penalties are severe. The reporting channels are active and staffed. And the fraud comes back anyway, because the economics of setting up a fake Instagram account and running it for 48 hours before deactivating are low enough that individual operators can keep trying. The only durable defence is the buyer’s own verification habit.

The good news: the verification habit is simple. Run the plate in the RTA system. Cross-reference the Emirates ID. Check for encumbrances. Use a verified channel. Pay through traceable means. Five steps, fifteen minutes, the overwhelming majority of fraud closed. The five categories above account for nearly every documented case in UAE press archives from 2021 through 2026, and every one of them falls when the five-step stack is run. A plate transaction done correctly is one of the safest luxury asset purchases available in the UAE. A plate transaction done without verification is one of the most exposed. The difference between those two outcomes is a quarter-hour of attention before you transfer the money.

If you are about to transact and this article has surfaced a concern, run the verification stack before you proceed. If you have already transacted and the signals above describe what happened to you, report to Dubai Police eCrime or the Aman Service today, not tomorrow. The first 24 hours matter more than any other period in the case lifecycle. For readers new to UAE plate ownership altogether, our expat eligibility and buying guide walks through the administrative basics that sit underneath every safe transaction, and our Dubai plate listings show what a verified, platform-accountable marketplace looks like in practice.

Delete Comment?

Are you sure you want to delete this comment? This action cannot be undone.

Delete Article?

Are you sure you want to delete this article? This will also delete all comments. This action cannot be undone.