Plates for Business Owners: How UAE Entrepreneurs Use Premium Number Plates as Branding, Marketing, and Asset-Class Tools

May 06, 2026

Abu Dhabi

LicensePlate.ae Team

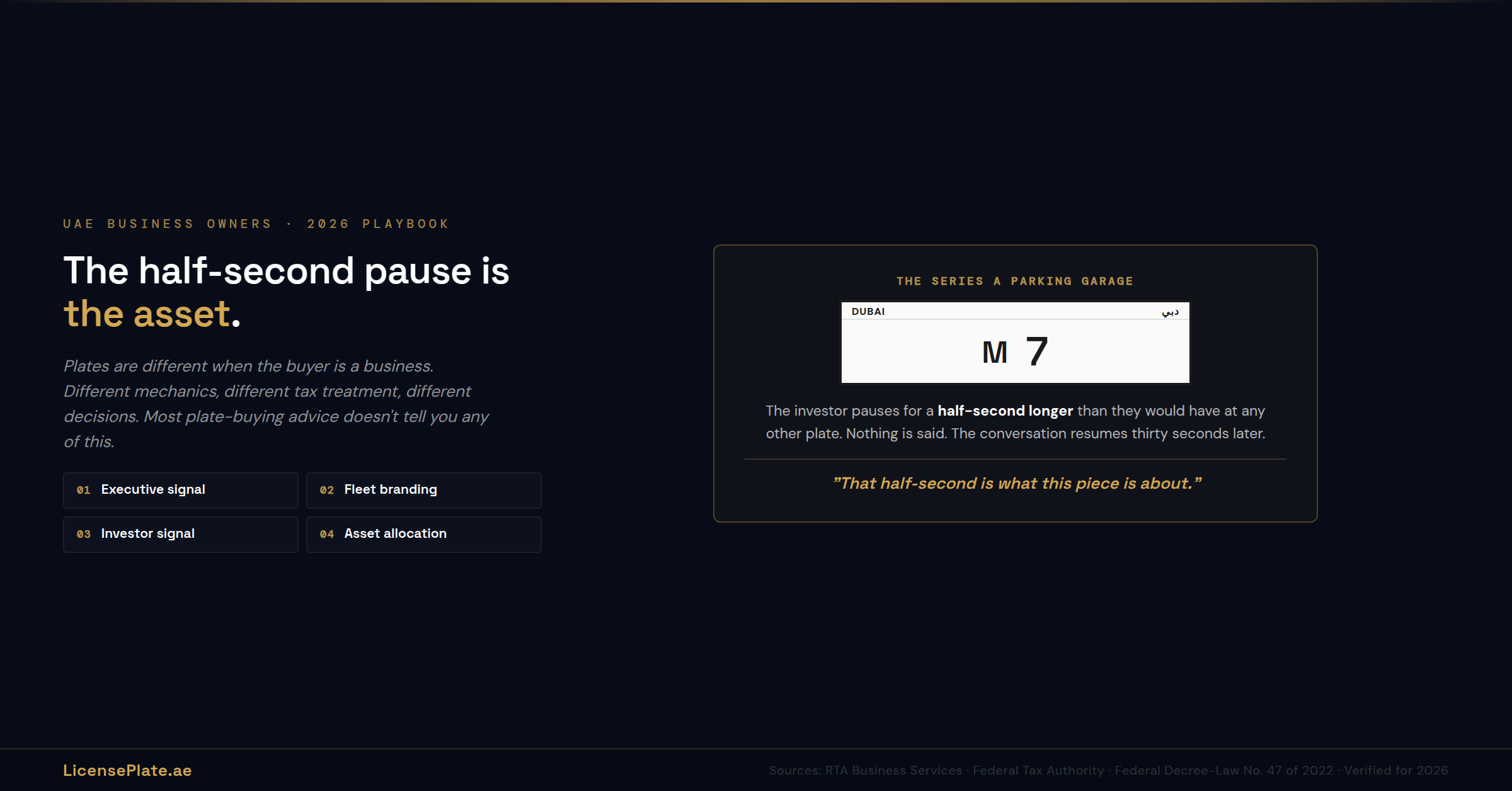

A founder closes a Series A in Dubai. The investor who led the round visits the office a week later. They walk to the parking garage together. The founder's car is parked in the executive bay. The plate reads M 7. Single-letter code, single digit. The investor pauses for a half-second longer than they would have at any other plate. Nothing is said. The conversation about the company's next milestone resumes thirty seconds later. The investor leaves.

That half-second pause is what this piece is about. UAE plate culture has built a vocabulary that business owners can use in ways individual buyers cannot. A premium plate on a company executive vehicle is not just a status display. It is, depending on how the company structures it, a corporate asset on the balance sheet, a branding instrument for client-facing meetings, an investor-signal device that operates without saying anything, and a fleet-policy choice that compounds across multi-vehicle businesses.

None of this is obvious from the plate-buying content that exists online. Almost every UAE plate guide is written for individual buyers. The decisions, mechanics, and tax treatment that apply to a business owner buying a plate through their company are materially different from the decisions, mechanics, and tax treatment that apply to a private buyer. This piece publishes the business-buyer playbook for the first time.

Three audiences will get the most from this piece. Founders and SME owners considering a premium plate for their executive vehicle. Family-business operators thinking through how plates fit a multi-vehicle, multi-generational company. Free-zone company directors and corporate fleet managers evaluating whether the plate-as-asset logic survives an honest cost-benefit analysis. The framework below applies to all three. The specific answers depend on which one you are.

First, Who Owns the Plate? Personal Name vs Company Trade License

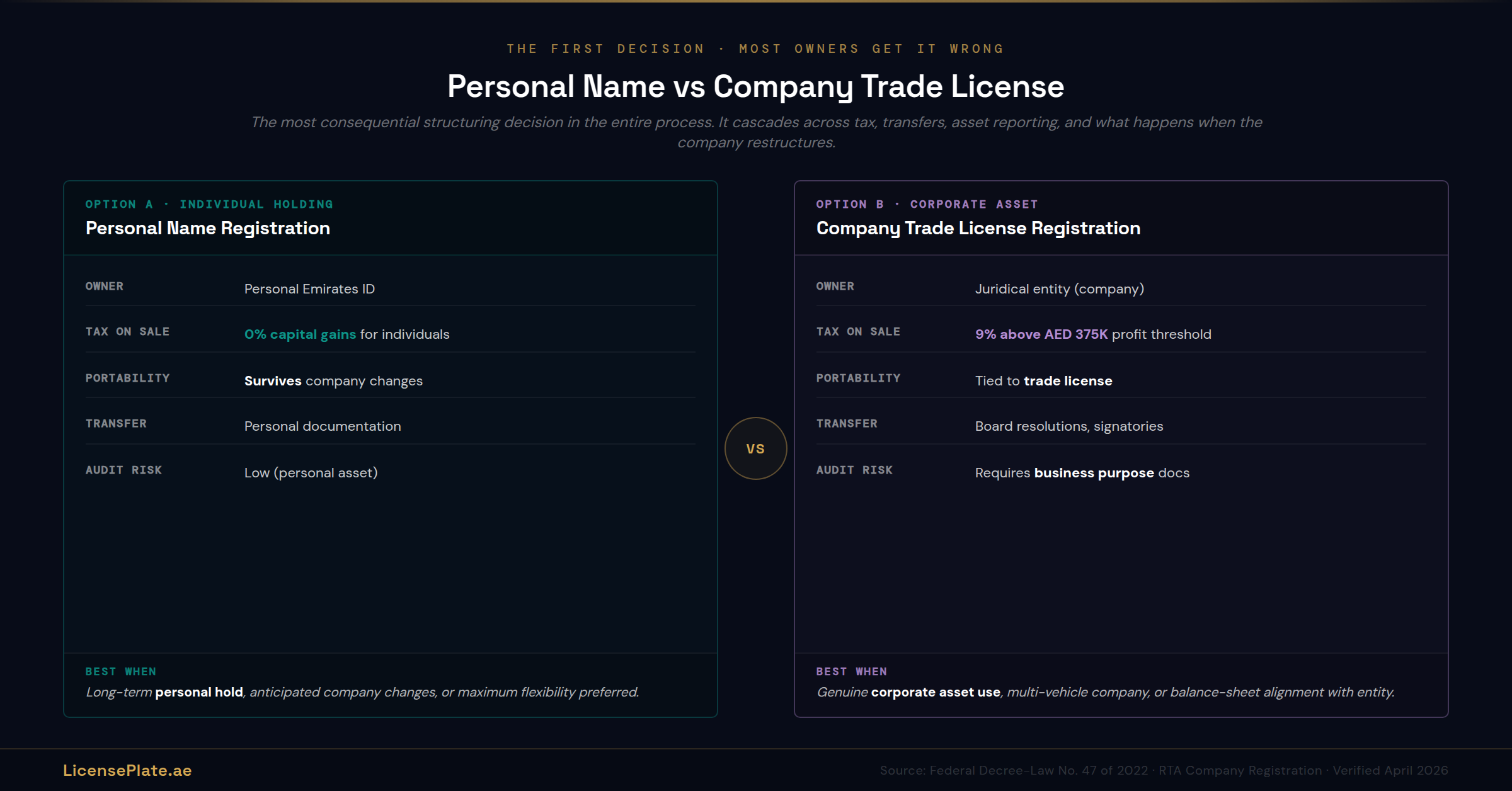

The most consequential decision in the entire process happens before the plate is bought, and most business owners get it wrong. The question is whose name the plate is registered under: yours personally, or the company's trade license.

Per the RTA's company registration documentation and the corporate vehicle services portal, a UAE company can register vehicles in its own name with a valid trade license and an authorisation letter. The same applies to plate ownership. The Plate Ownership Certificate can be issued to a juridical person (the company) rather than a natural person (the individual owner). This single distinction has cascading consequences across tax, asset reporting, transferability, and what happens when the company restructures.

Personal-name registration

How it works: The plate is registered in your personal Emirates ID. The vehicle the plate is mounted on may be company-owned or personal. Ownership of the plate transfers with you regardless of company changes.

Tax treatment: The plate is a personal asset. Per the existing UAE Corporate Tax and Plate Investors article, personal plate ownership generally falls outside the corporate tax framework unless plate trading rises to the level of a business activity. There is no immediate corporate tax deduction available because the asset is not held by a taxable person. There is also no capital gains tax in the UAE on plate sales by individuals.

When this makes sense: Owner-operators who want maximum flexibility and asset portability. Founders who anticipate multiple company changes over the plate's lifetime. Anyone who values the plate as a personal asset rather than a company resource.

Company trade license registration

How it works: The plate is registered in the company's name via the trade license. The Plate Ownership Certificate is issued to the juridical entity. Transfers and ownership changes flow through company processes (board resolutions, authorised signatories) rather than personal documentation.

Tax treatment: Per the PwC analysis of UAE Corporate Tax deductions and the Aurifer Tax practical guide, capital expenditure is not immediately deductible. The plate, when held as a corporate asset, is treated as capital and subject to depreciation over its useful life under standard accounting standards. This means the company does not get a same-year tax shield on the AED 200,000 plate purchase, but rather amortises the cost over the asset's accounting life.

When this makes sense: Companies with multiple executive vehicles where plate ownership rotates with role changes. Family businesses planning multi-generational vehicle transfers. Companies where the plate genuinely functions as a brand asset (the four use cases in the next section), not just a personal preference disguised as a company expense.

Note: This piece provides general information about UAE corporate tax positioning of plates. It is not a substitute for advice from a qualified UAE tax adviser. Federal Decree-Law No. 47 of 2022 and its associated Cabinet and Ministerial Decisions are the authoritative source. The Federal Tax Authority’s published guidance evolves; verify with a tax adviser before making capital allocation decisions based on tax treatment.

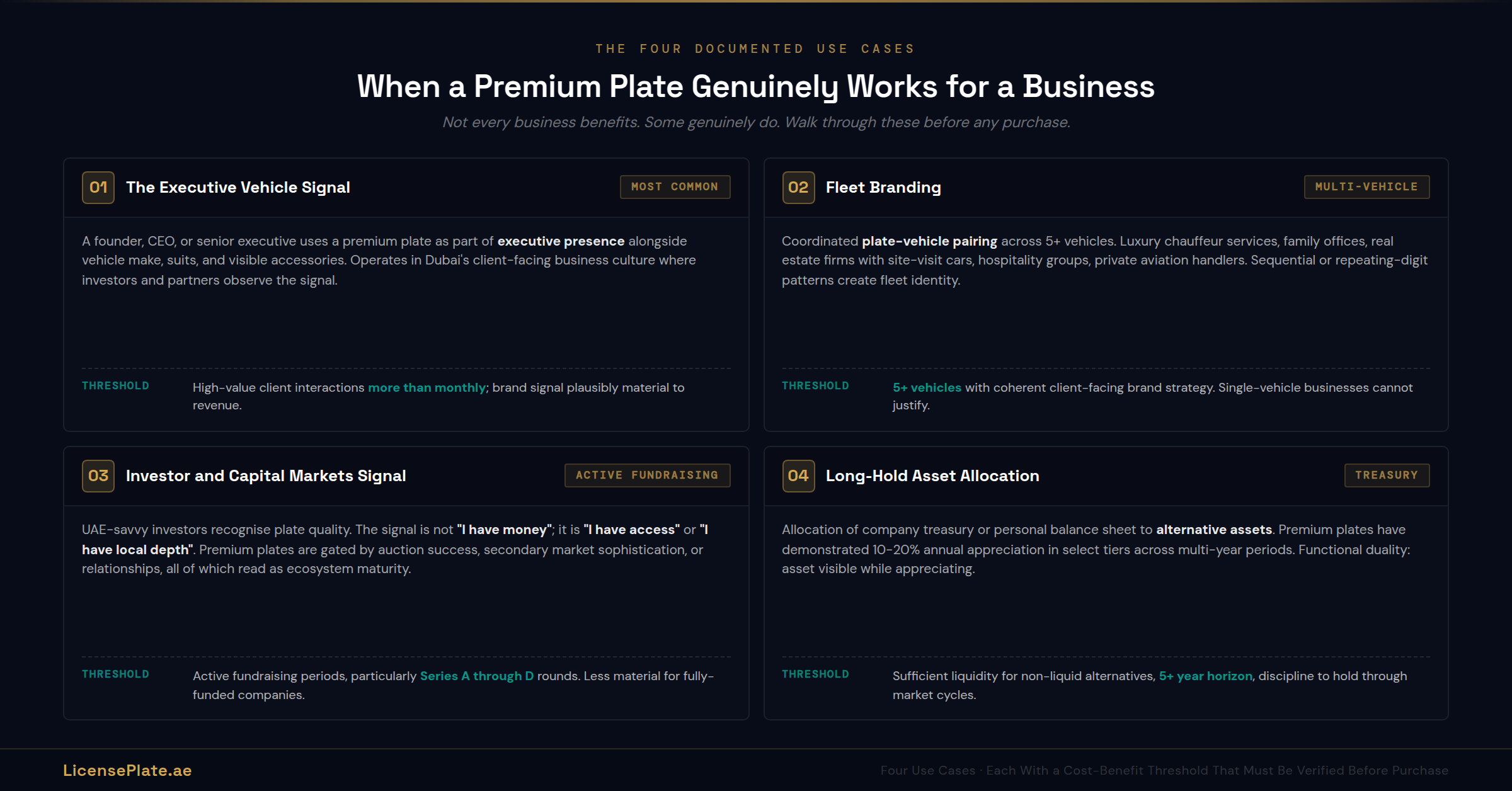

The Four Use Cases: When a Premium Plate Genuinely Works for a Business

Not every business benefits from a premium plate. Some genuinely do. The honest framework: there are four use cases where the cost is defensible, and several where it is not. Walk through these before any purchase.

Use Case 1: The Executive Vehicle Signal

The most common use case. A founder, CEO, or senior executive uses a premium plate on their company-provided vehicle as part of the role's compensation package and brand expression. The plate is part of the executive-presence calculus that includes the vehicle make, model, and visible accessories.

Why it works: In Dubai's client-facing business culture, executives meet partners, investors, and clients at locations where the executive's vehicle is visible (DIFC parking garages, Emirates Towers, valet parking at restaurants and clubs). The plate photography economy article documents the structural fact that premium plates are visible signals in Dubai car culture. Executives operating in this environment benefit from the same signal mechanics that apply to luxury watches, suits, and offices.

Cost-benefit threshold: Generally justifies the spend when the executive interacts with high-value clients or investors regularly (more than monthly), where the brand signal is plausibly material to revenue or capital outcomes, and where the plate is a small fraction of the overall executive compensation package.

Use Case 2: Fleet Branding for Client-Facing Companies

Some UAE companies operate fleets where every vehicle is part of the brand experience: luxury chauffeur services, family offices with branded vehicles, high-end real estate firms with site-visit cars, hospitality groups, private aviation handlers. For these companies, plates can become a coordinated brand asset.

Why it works: If a company operates 5-15 vehicles that all interact with high-net-worth clients, sequential plate numbers (the AA 11, AA 12, AA 13 pattern) or coordinated repeating-digit plates create a recognisable fleet identity. Per the existing car-plate pairing economics article, coordinated plate-vehicle pairing carries cultural value in Dubai car culture. A fleet of company-coordinated plates extends that pairing logic from the individual to the corporate level.

Cost-benefit threshold: This use case requires multiple vehicles (5+) and a coherent client-facing brand strategy. Single-vehicle businesses generally cannot justify the fleet-branding logic.

Use Case 3: Investor and Capital Markets Signal

UAE founders raising capital from regional or international investors operate in an environment where investors observe behavioural signals across many touchpoints. The premium plate on the founder's vehicle is one of dozens of signals (office quality, hire quality, public visibility, social presence) that investors aggregate into their pattern recognition about the founder.

Why it works: UAE-savvy investors recognise plate quality. A founder driving a M 1 or AA 22 plate is communicating something specific about their position in the local business ecosystem. The signal is not 'I have money' (any luxury vehicle communicates that). The signal is 'I have access' or 'I have local depth.' Premium plates are gated by either auction success, secondary market sophistication, or relationships, all of which read as ecosystem maturity.

Cost-benefit threshold: Active fundraising periods, particularly Series A through D rounds, where founder signals materially affect investor confidence. Less material for fully-funded companies or owner-operated businesses without external capital.

Use Case 4: Long-Hold Asset Allocation

Some UAE entrepreneurs allocate a portion of company treasury or personal balance sheet to alternative assets including plates. Per the existing plates as alternative asset class article and the investment guide, premium UAE plates have demonstrated 10-20% annual appreciation in select tiers across multi-year periods. For founders treating plates as a treasury allocation, the plate's cosmetic role on a vehicle is secondary to its long-term value preservation.

Why it works: UAE plates offer something most asset classes do not: documented appreciation, zero capital gains tax for individuals, low correlation to traditional asset classes, and (uniquely) the ability to use the asset visibly while it appreciates. The asset is on a vehicle, not in a vault. This functional duality justifies the holding cost in ways static assets cannot.

Cost-benefit threshold: Founders with sufficient liquidity to lock capital in non-liquid alternative assets, with a multi-year holding horizon (5+ years minimum), and with the discipline to hold through market cycles. Not appropriate for businesses with capital constraints or short-term cash flow priorities.

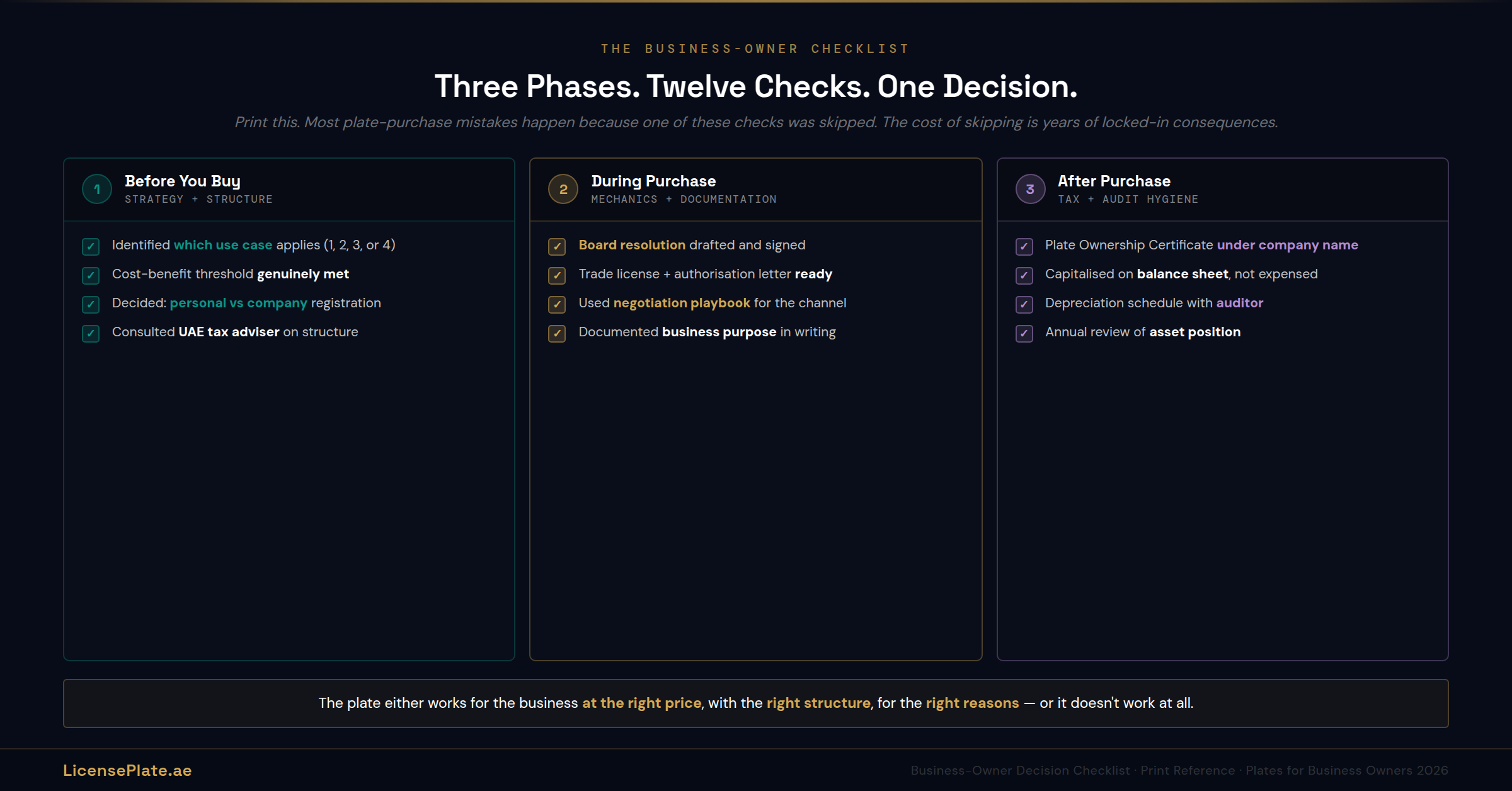

How to Register a Premium Plate Under a Company

The procedural side. Once the decision is made (use case identified, cost-benefit verified, ownership structure chosen), the registration sequence runs through RTA's company-registered vehicle channels. Three documented paths exist.

Path 1: Auction Purchase Under Company Name

RTA online and hall auctions accept company bidders. The auction registration requires the company's trade license rather than (or in addition to) the individual's Emirates ID. The RTA online auction system supports company accounts with appropriate authorisation documentation.

Documents required: Trade license (active and valid), Memorandum of Association or company formation documents, board resolution authorising plate purchase, authorisation letter naming the bidding individual, the individual bidder's Emirates ID, the AED 5,000 (online) or AED 25,000 (hall) security cheque made out to RTA.

Tactical note: Per the plate negotiation playbook, company bidders face the same auction dynamics as individual bidders but often have greater capital flexibility. The bidding tactics (set maximum, bid late, walk away when threshold hits) apply identically.

Path 2: Secondary Market Purchase Under Company Name

Marketplace transactions on platforms like LicensePlate.ae accept both individual and corporate buyers. The how to buy on LicensePlate.ae article covers the marketplace mechanics. For corporate purchases, the buyer side documentation includes the trade license, board resolution, and authorisation letter naming the transaction signatory.

Tactical note: Marketplace listings typically do not differentiate price between individual and corporate buyers. The 15-25% negotiation room documented in the negotiation playbook applies equally. The handover and Plate Ownership Certificate issuance are the only steps where corporate registration meaningfully differs from individual registration.

Path 3: Transfer from Founder's Personal Name to Company

If a founder owns a premium plate personally and wants to transfer it to the company's books (often for tax-positioning or balance-sheet reasons), the standard plate transfer process applies. The anatomy of a plate transaction article covers the full transfer mechanics. The key adjustment for personal-to-company transfers: this is technically a sale from the individual to the company, which has implications for the company's capitalisation of the asset and potentially for the individual's reporting if the plate was held as a business activity.

Tactical note: Personal-to-company plate transfers should be priced at fair market value (using the plate calculator and recent comparables) and documented properly. Below-market transfers may attract scrutiny under transfer pricing rules per the FTA's published transfer pricing guidance. Consult a qualified tax adviser before executing.

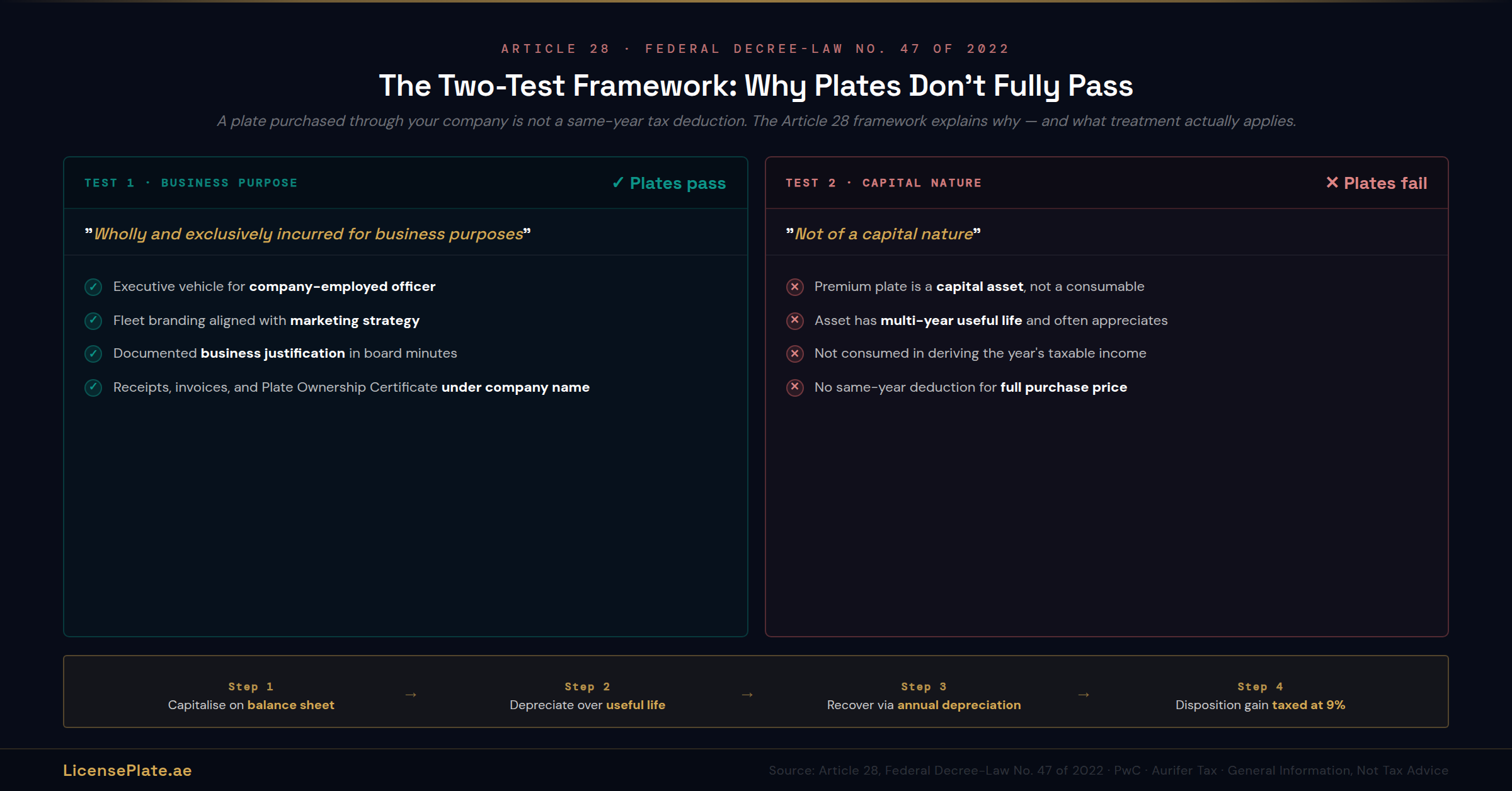

The Corporate Tax Position: What's Deductible, What's Capital, What's Not

This is the section most business owners get wrong. The intuition that a plate purchased through the company is 'a business expense and therefore deductible' is incorrect for most plate purchases. Walk through the actual treatment carefully.

The Article 28 framework

Per Article 28 of the UAE Corporate Tax Law, an expense is deductible only if it is 'wholly and exclusively incurred for business purposes' and is 'not of a capital nature.' Both conditions matter. Most premium plate purchases satisfy the first (the plate is for the business) but fail the second (the plate is a capital asset).

Capital expenditure treatment

Per the Aurifer Tax 2025 deductibility guide, capital expenditure is recovered through depreciation or amortisation over the asset's useful life under standard accounting standards. A plate purchased for AED 500,000 is not a AED 500,000 deduction in the year of purchase. It is depreciated against company income over the plate's accounting life.

The accounting question becomes: what is a plate's useful life? Plates are unusual capital assets because they do not physically degrade. They appreciate rather than depreciate in many cases. UAE accounting standards have not published specific guidance for plate-as-capital-asset depreciation, which means most companies amortise plates conservatively over 10-20 years following standard intangible-asset guidance, or treat them as non-depreciating capital assets that recover cost only on disposition.

Disposition and capital gains positioning

When a company sells a plate, the gain (sale price minus original cost minus accumulated depreciation) is taxable corporate income at the standard 9% rate above AED 375,000 of total company profit. Companies with low overall profitability may have plate disposition gains absorbed by other losses. Companies with high profitability face the 9% on plate gains. The UAE Corporate Tax and Plate Investors article covers the broader gain-treatment framework in detail.

Critically: the 0% capital gains tax that applies to individual plate sales does NOT apply to company sales. This is one of the strongest arguments for personal-name registration when the holding is intended as a long-term appreciating asset.

Free zone company nuances

Per the Federal Tax Authority's qualifying free zone person framework, qualifying free zone persons (QFZPs) can benefit from a 0% rate on qualifying income. Whether plate-related gains fall within qualifying income depends on the specific free zone, the nature of the company's activities, and whether plate trading constitutes a 'qualifying activity' under the relevant decree. Most free zone companies do not have plate trading as a qualifying activity, which means plate gains may be taxable at 9% even within a free zone structure.

The free zone advantage applies to the 0% rate on qualifying income, not to plate-specific tax treatment. A free zone company buying a plate as a corporate asset still treats it as capital expenditure, still depreciates it (or doesn't, depending on accounting choice), and still pays 9% on disposition gains if those gains fall outside qualifying income.

A Critical Distinction: Premium Private Plates vs RTA Commercial Plates

Most business owners considering 'a plate for the business' conflate two very different categories. Understanding the distinction prevents serious mistakes.

RTA Commercial Plates

Per the RTA's commercial license plate service and Shory's commercial plate guide, commercial plates are a specific RTA category for vehicles operating commercially: trucks, vans, taxis, delivery vehicles, courier fleets, transport-licensed companies. These plates have a different visual design (typically red text on white background or coloured backgrounds depending on category) and serve a regulatory function distinct from premium private plates.

Critically: Commercial plates are not premium plates and do not appreciate as alternative assets. They are operational regulatory items issued at standard fees. The RTA assigns commercial plate numbers based on vehicle type and licensing classification. There is no auction, no premium pricing, no investment thesis.

Premium Private Plates Registered to Companies

This piece is about premium private plates (single-letter codes A-Z, double-letter codes AA-DD, low digit counts) that happen to be registered under company ownership rather than individual ownership. These are the plates with auction premiums, secondary-market value, and the four use cases described above. They are mounted on private vehicles (typically executive-class cars: S-Class, 7-Series, Range Rover, etc.) registered under the company's name.

The visual distinction: A premium private plate looks like an individual's premium plate. The plate code, format, and design are identical. The only difference is the ownership record in RTA's system: the Plate Ownership Certificate names the company rather than the individual.

This article addresses the second category. Commercial plates, while important to fleet operators, are a separate procedural topic covered by RTA commercial vehicle services and not the subject of this piece.

Six Mistakes UAE Business Owners Make With Premium Plates

Mistake 1: Treating a premium plate as a same-year tax deduction. It is not. Per Article 28 of the Corporate Tax Law, capital expenditure is recovered through depreciation over the asset's useful life, not deducted immediately. Companies that book plate purchases as full-year operating expenses face FTA risk on audit.

Mistake 2: Registering the plate under the company when the long-term holding strategy is personal. Personal-name registration preserves the 0% individual capital gains treatment on eventual sale. Company registration converts the plate to a corporate asset taxable at 9% on disposition above the AED 375,000 profit threshold. For founders intending to hold the plate for personal long-term value, personal registration is materially better tax-positioned.

Mistake 3: Confusing premium private plates with commercial plates. Different categories, different procedures, different appreciation profiles. Commercial plates are operational. Premium private plates are alternative assets. Mixing the two leads to misallocated capital and incorrect operational expectations.

Mistake 4: Registering a plate under the company without a board resolution. UAE corporate governance requires board-level authorisation for material asset purchases. A AED 200,000+ plate purchase should be documented with a board resolution naming the asset, the purchase price, the authorised signatory, and the business justification. Skipping this creates audit risk and complicates eventual disposition.

Mistake 5: Failing to document the business purpose. Per Article 28, deductibility (and depreciation eligibility) requires the expenditure be 'wholly and exclusively for business purposes.' A plate that is registered under the company but used solely for the founder's personal driving does not satisfy this test cleanly. Documentation that demonstrates business use (executive role on the vehicle, client-facing meetings, fleet branding strategy) protects the corporate-asset position.

Mistake 6: Not consulting a UAE tax adviser before purchase. UAE corporate tax is new (effective from 1 June 2023), and the FTA's published guidance evolves. The general framework in this piece is accurate as of publication, but specific structuring decisions should run through a qualified UAE tax adviser. The cost of advice (typically AED 2,000-10,000 for a structuring review) is small relative to the multi-year tax exposure of a poorly-structured plate purchase.

Frequently Asked Questions

Q: Can a UAE company own a premium number plate?

Yes. RTA company registration accepts trade license-based plate ownership with appropriate authorisation documentation. The Plate Ownership Certificate is issued to the juridical entity (the company) rather than a natural person. Required documents include the active trade license, board resolution authorising the purchase, authorisation letter, and the individual signatory's Emirates ID.

Q: Is a premium plate purchased through my company tax-deductible?

Not as an immediate deduction. Per Article 28 of the UAE Corporate Tax Law, the plate is capital expenditure (not of a non-capital nature) and is recovered through depreciation or amortisation over the asset's useful life under standard accounting standards. The company does not get a same-year tax shield equal to the plate's purchase price. Consult a qualified UAE tax adviser for specific structuring.

Q: Should I register the plate personally or through my company?

It depends on your intent. Personal registration preserves 0% capital gains on eventual sale and offers maximum portability. Company registration enables corporate balance-sheet treatment, depreciation, and aligns the asset with the entity that benefits from it. For long-term personal holdings, personal registration is generally tax-better. For genuine corporate-asset use cases (fleet branding, executive vehicle in a multi-vehicle company), company registration is structurally appropriate.

Q: How does this differ from RTA commercial plates?

Commercial plates are a different RTA category for vehicles operating commercially (trucks, vans, taxis, delivery, transport-licensed companies). They have different visual design and serve a regulatory function. They are not premium plates and do not appreciate as alternative assets. This article addresses premium private plates registered to companies, not commercial plates.

Q: What if my company is a free zone entity?

Free zone companies can register plates under their trade licenses the same way mainland companies can. The corporate tax treatment depends on whether the free zone company is a Qualifying Free Zone Person and whether plate-related gains fall within qualifying income. Most free zone companies do not have plate trading as a qualifying activity, meaning plate disposition gains may be taxable at 9% even within a free zone structure. Verify with a tax adviser specific to your free zone.

Q: Can I transfer a plate I own personally to my company?

Yes. The standard plate transfer process applies. The transfer should be priced at fair market value (using the calculator and comparables) and documented properly. Below-market transfers between related parties may attract scrutiny under transfer pricing rules. Document the transfer with a board resolution and consult a tax adviser on the personal-side reporting if the plate was held in connection with business activity.

Q: Does a premium plate make sense for a small business with under AED 1 million revenue?

Generally no. The four use cases (executive signal, fleet branding, investor signal, balance-sheet asset) require either a client-facing role with regular high-value interactions, multiple vehicles, active capital markets engagement, or substantial liquidity for long-term alternative-asset allocation. Small businesses without these characteristics rarely justify the capital lockup. The plate as a personal preference is fine; the plate as a business asset is harder to justify at smaller scales.

Q: What documentation should I keep for an audit?

Board resolution authorising the purchase, the RTA Plate Ownership Certificate naming the company, the purchase invoice or auction confirmation, evidence of the business purpose (executive role assignment, fleet policy document, marketing brand strategy referencing the plate, balance-sheet allocation rationale), and the depreciation schedule or accounting treatment applied. Annual review with the company's external auditor or tax adviser strengthens the audit position.

UAE plate culture has built one of the most sophisticated alternative-asset markets in the region, and UAE entrepreneurs sit at the centre of it. The decisions a business owner makes about plate ownership ripple across tax positioning, balance sheets, brand expression, and investor signals in ways that individual buyers do not encounter. Most of those decisions are made without the framework above, and most of them end up locked in for years before the consequences become visible.

The framework is not complicated. Pick the use case that genuinely applies to your business. Decide whether personal or company registration is structurally appropriate. Run the auction or marketplace mechanics with the documentation in hand. Treat the plate as a capital asset for tax purposes, not as an operating expense. Consult a UAE tax adviser before significant capital allocation. Document the business purpose so the position holds at audit. Hold for the time horizon that matches the use case, not the time horizon that matches your patience.

For procedural depth, the RTA buy guide and the anatomy of a plate transaction cover the operational steps. For valuation, the plate calculator and price check article anchor the math. For tax positioning, the UAE Corporate Tax and Plate Investors article extends the framework above. For the broader cultural context, the plate photography economy article covers why premium plates work as visible business assets in Dubai specifically. Together these pieces form a complete decision-support stack for the UAE business owner thinking seriously about a premium plate.

The plate is on the car. The car is in the parking garage. The investor pauses for a half-second. The half-second is the asset. Whether the asset is worth what it costs depends on the framework above, applied honestly to your specific company.

Delete Comment?

Are you sure you want to delete this comment? This action cannot be undone.

Delete Article?

Are you sure you want to delete this article? This will also delete all comments. This action cannot be undone.