UAE Corporate Tax and Plate Investors: When Flipping Becomes Business Activity

April 29, 2026

Dubai

LicensePlate.ae Team

⚠ Important: This article is general informational content, not tax advice. UAE Corporate Tax law is complex and the FTA's interpretation of natural-person business activity continues to evolve. Anyone whose plate activity may approach or cross the AED 1 million turnover threshold, or who is structuring a holding entity, should consult a UAE-licensed tax advisor before relying on any framework in this piece. The ultimate authority is the Federal Tax Authority's published guidance and the Federal Decree-Law No. 47 of 2022, not this article.

If you bought one premium plate three years ago, held it, and sold it last month for double what you paid, the UAE Federal Tax Authority’s answer is straightforward: that gain is personal investment income, not business activity, and not subject to UAE Corporate Tax. If you bought twelve plates in the last eighteen months, held them for an average of four months each, advertised them on a website you operate, and made AED 1.4 million in turnover from the resale activity, the answer changes. You are now potentially conducting a business as a natural person, which means registration with the Federal Tax Authority, annual returns, and 9% Corporate Tax on profits above AED 375,000.

The line between those two scenarios is not a number. It is a multi-factor test the FTA published in November 2023 in the Corporate Tax Guide on Taxation of Natural Persons (CTGTNP1), refined through subsequent Cabinet Decisions and FTA bulletins through 2025. Most plate buyers in the UAE have read none of this material. Most plate flippers operating at scale have not adapted their practices to it. This piece exists to close that gap.

It is structured around three questions: what the rules actually are, where the line sits for plate-specific activity, and what to do if your activity may already cross it. It is not tax advice. The framework here is the publishing equivalent of orientation, not opinion. Anyone whose plate turnover may approach AED 1 million in a Gregorian calendar year, or anyone considering a Free Zone or DIFC structure for plate holdings, should consult a UAE-licensed tax advisor before acting on anything in this piece.

What the Law Actually Says

The UAE introduced federal Corporate Tax effective for financial years starting on or after 1 June 2023 under Federal Decree-Law No. 47 of 2022. The headline rate is 9% on taxable income above AED 375,000 per financial year, with 0% on the first AED 375,000. Most public attention has focused on companies. The provision that catches plate flippers off guard is the rule for natural persons.

The natural-person threshold

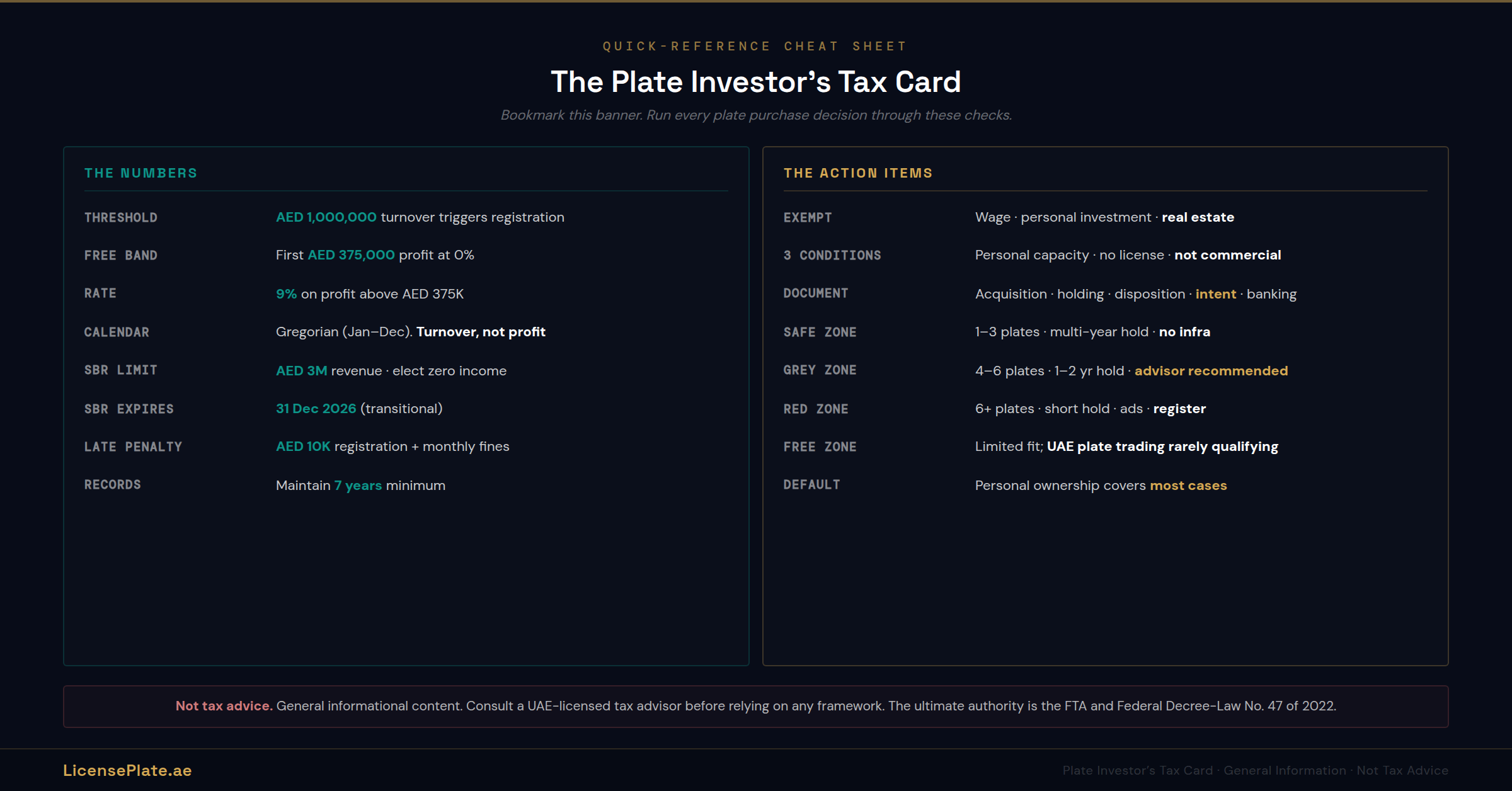

Per the FTA’s Corporate Tax Topics page, a natural person is subject to Corporate Tax in the UAE only when total turnover derived from business or business activities exceeds AED 1 million within a Gregorian calendar year (January to December). Below AED 1 million, no registration is required and no Corporate Tax is owed on that activity. Above AED 1 million, registration is required, an annual return must be filed, and Corporate Tax applies to profits at the 0%/9% structure described above.

The threshold is on turnover (gross revenue), not profit. A plate that sells for AED 800,000 against a purchase cost of AED 600,000 produces AED 800,000 of turnover and AED 200,000 of profit. The AED 1 million threshold counts the AED 800,000, not the AED 200,000.

What does NOT count toward the threshold

This is the piece most plate buyers do not realise. Three categories of income are explicitly excluded from the AED 1 million calculation under the FTA's Natural Persons Guide CTGTNP1:

Wage income. Salary, bonuses, and director’s fees from employment. Excluded entirely.

Personal investment income. Investment activity that a natural person conducts for their own account, not through a business license, not considered a commercial activity under the Federal Decree-Law No. 50 of 2022 issuing the Commercial Transactions Law, and not requiring a license to be conducted lawfully.

Real estate investment income. Income from sale, lease, sub-lease, or rental of land or real estate property in the UAE, where the activity is not conducted (and not required to be conducted) through a license issued by a UAE Licensing Authority.

For a plate buyer, the relevant exclusion is personal investment income. The question becomes: when does plate buying-and-selling qualify as personal investment, and when does it cross into business activity?

The Test the FTA Actually Applies

Per Hourani & Partners' analysis of the FTA Natural Persons Guide, the FTA does not apply a single bright-line test. Personal investment income is exempt only when all of these conditions are met:

Condition 1: The activity is conducted in personal capacity. Not through a sole-proprietorship trade license. Not through a company. Personal name, personal traffic file.

Condition 2: The activity does not require a Licensing Authority license. If the activity, by its nature or scale, would require a UAE Licensing Authority to issue a license, it is not personal investment regardless of whether you actually obtain the license. The relevant question: under the Commercial Transactions Law, would this activity be classified as commercial trading?

Condition 3: The activity is not a commercial business under the Commercial Transactions Law. Federal Decree-Law No. 50 of 2022 defines commercial activity. The classic markers, internationally referred to as “badges of trade,” apply: frequency of transactions, profit-seeking intent at acquisition, holding period, organisation of the activity, advertising and marketing, and use of supporting infrastructure (websites, agents, employees).

If any of these conditions fail, the income is not personal investment income. The activity counts toward the AED 1 million threshold and may trigger Corporate Tax registration even below that turnover if the activity is conducted under a license.

FTA's published examples adapted to plates

The FTA Natural Persons Guide includes worked examples of personal investment versus business activity for general asset classes. Adapting them to the plate market produces the following framework. These examples illustrate the spectrum and are not definitive determinations.

Example A (clear personal investment): A UAE resident buys one premium plate at AED 1.5M as a long-term hold. Holds for five years. Sells at AED 2.4M. Files no advertising, runs no website, conducts no other plate transactions in the year. The gain is personal investment income. No Corporate Tax obligation.

Example B (clear personal investment): A UAE resident inherits a plate from a parent. Sells two years later at market value. The transaction is personal asset disposition. No Corporate Tax. The inheritance guide covers the procedural mechanics.

Example C (likely business activity): A UAE resident operates a website advertising 30+ plates for sale, transacts 18 plates in the calendar year, and earns AED 1.6M in turnover from those sales. The activity has frequency, organisation, advertising infrastructure, and profit-seeking intent. The FTA would likely classify this as business activity. Registration required, returns required, Corporate Tax on profit above AED 375,000.

Example D (the grey zone): A UAE resident buys four premium plates over two years, sells two of them in the third year for AED 950,000 of total turnover, holds the other two. No website, no advertising. The plates were marketed via word of mouth and a single classified posting on an existing marketplace platform. This is the grey zone. Below the AED 1M turnover threshold; no advertising infrastructure; but four transactions and clear profit-seeking intent. The FTA assessment depends on whether the activity is viewed as occasional personal portfolio rebalancing or systematic commercial trading. A licensed tax advisor would be appropriate before assuming personal investment treatment.

Where the Line Likely Sits for Plate Activity Specifically

Plates are an unusual asset class for tax purposes. Real estate has a clear exclusion under the Real Estate Investment carve-out (provided no license is required for the activity). Securities held in personal investment accounts have their own treatment. Plates fit closest to other personal collectibles and tangible personal assets.

Three factors push plate activity toward personal investment:

Factor 1: Plate ownership does not currently require a Licensing Authority license. There is no “plate dealer license” required to buy, hold, or occasionally sell plates as a private individual. The activity itself is not licensed. This satisfies one of the FTA’s three exemption conditions.

Factor 2: Plates are tangible personal assets registered to a traffic file. Like other personal assets (jewellery, art, classic cars), occasional sales by an individual for personal financial reasons are typically personal investment.

Factor 3: The market structure favours individual buyers. Most plate transactions in the UAE are individual-to-individual. The auction versus secondary market piece covers the channel structure. Family offices and dealers are a minority of total transactions.

Three factors push plate activity toward business:

Factor 1: Frequency and turnover. Multiple plate transactions in a calendar year, particularly if turnover approaches or exceeds AED 1 million, raises business-activity flags.

Factor 2: Advertising infrastructure. If you operate a website, run paid ads, build a customer database, or use a brand to attract plate buyers, you have built business infrastructure. This is a strong indicator of commercial activity.

Factor 3: Short holding periods with profit-seeking intent. Buying with the explicit purpose of resale at profit, holding for short periods (weeks to months rather than years), and treating the activity as a profit-generating undertaking aligns with commercial trading regardless of turnover level.

The honest answer for most plate buyers: if you hold one to three plates for multi-year periods and sell occasionally, you are almost certainly in personal investment territory. If you transact six or more plates per year, advertise actively, and have any month where turnover exceeds AED 100,000, you are in territory where a tax advisor consultation is appropriate. The Portfolio Construction framework includes the architecture for staying in personal investment territory while building meaningful exposure.

Structuring Options for Active Plate Investors

If your plate activity does cross into business territory, or if you anticipate it crossing in the next two to three years, structure becomes the relevant question. Several options exist, each with different tax, operational, and cost profiles. None of these are tax advice; each requires legal and tax review specific to the individual circumstances.

Option 1: Personal ownership, accept Corporate Tax

Continue holding plates personally. Register with the FTA when turnover approaches AED 1 million. File annual returns. Pay 9% on profits above AED 375,000. Simplest structure. Lowest setup cost. Suitable when the volume is just above threshold and the administrative burden is acceptable.

Practical note: registration deadlines are strict. Per the FTA Corporate Tax Topics page, late registration carries penalties of AED 10,000. Returns must be filed within 9 months of the tax period end. Maintain financial records for at least 7 years.

Option 2: Sole Proprietorship trade license

Establish a sole-proprietor trade license (mainland or appropriate Free Zone). Operate plate trading as a licensed activity. The income is from a Taxable Person and subject to Corporate Tax under the same 0%/9% structure. Adds operational legitimacy and the ability to deduct business expenses (office, marketing, professional fees, travel related to plate sourcing). Higher annual cost than personal ownership (license fees, office requirement). Suitable when the operation has genuine commercial scale.

Option 3: Free Zone entity (Qualifying Free Zone Person)

Establish a Free Zone company. Per Chambers Partners' Corporate Tax 2025 guide and the Ministry of Finance's QFZP requirements, a Qualifying Free Zone Person can benefit from 0% Corporate Tax on Qualifying Income. Conditions include adequate economic substance in the UAE (staff, premises, expenses), compliance with transfer pricing rules, and earning Qualifying Income (typically international transactions, intra-Free Zone transactions, and specific qualifying activities).

The catch for plate dealers: trading plates with UAE mainland customers (which is what most plate dealers actually do) is generally not Qualifying Income. It would be subject to standard 9% Corporate Tax on the non-qualifying portion. The Free Zone benefit primarily helps when the structure also conducts qualifying activities such as international portfolio management, holding company functions, or intellectual property licensing. For a pure plate-trading operation focused on UAE customers, Free Zone structuring offers limited tax advantage and adds significant overhead.

Option 4: DIFC or ADGM holding structure

For high-net-worth individuals with substantial plate portfolios (typically AED 5 million or more), a DIFC or ADGM holding entity (often a foundation or family investment company) provides estate planning, succession, and cross-border tax planning benefits in addition to UAE Corporate Tax considerations. These structures are sophisticated, expensive to establish (typically AED 50,000–250,000+ in setup), and only make sense at scale. They are mentioned here for completeness; pursuing them requires specialist legal and tax advice.

Option 5: Small Business Relief

Per the DIAC corporate tax guide, Small Business Relief allows businesses with revenue at or below AED 3 million per tax period to elect zero taxable income. Available for tax periods ending on or before 31 December 2026 as a transitional measure. For plate flippers operating just above the AED 1M registration threshold, this relief can effectively eliminate Corporate Tax liability for the relief period. Election is not automatic; it must be claimed on the annual return. After 31 December 2026, this relief expires unless extended.

Documentation That Protects You Either Way

Whether your plate activity sits clearly in personal investment territory or in the grey zone, documentation is the single most important practice. The FTA's position is fact-driven; documentation is what establishes the facts. Five categories of records matter:

1. Acquisition records. For every plate purchased: date of purchase, purchase price, channel (auction, secondary market, broker), seller identity, RTA Plate Ownership Certificate dated to the transaction. The Anatomy of a Plate Transaction article covers the full transaction documentation lifecycle.

2. Holding records. Annual records confirming continued ownership (Mulkiya, traffic file printouts, insurance certificates listing the plate). These establish holding period, which is relevant to the personal-investment versus business-activity distinction.

3. Disposition records. For every plate sold: date of sale, sale price, channel, buyer identity (where disclosed), the new RTA Plate Ownership Certificate showing the transfer. Bank records of payment receipt.

4. Intent documentation. This is unconventional but valuable. A simple investment memorandum at the time of acquisition stating the rationale for the purchase (long-term capital appreciation, philanthropic plans, identity asset, etc.) creates contemporaneous evidence of intent. The FTA assesses business-activity classification partly on intent; documenting investment intent at the time of purchase is consistent with personal investment treatment.

5. Banking and financial records. Bank statements showing how purchases and sales were funded and where proceeds went. Personal investment proceeds typically flow back into personal accounts and personal use. Business proceeds typically flow into operating accounts that fund further inventory.

Maintain these records for at least seven years per the FTA's record retention requirement. The records protect you if FTA classification is ever questioned and provide the audit trail for any tax advisor reviewing the activity.

When DIY Analysis Stops and Professional Advice Starts

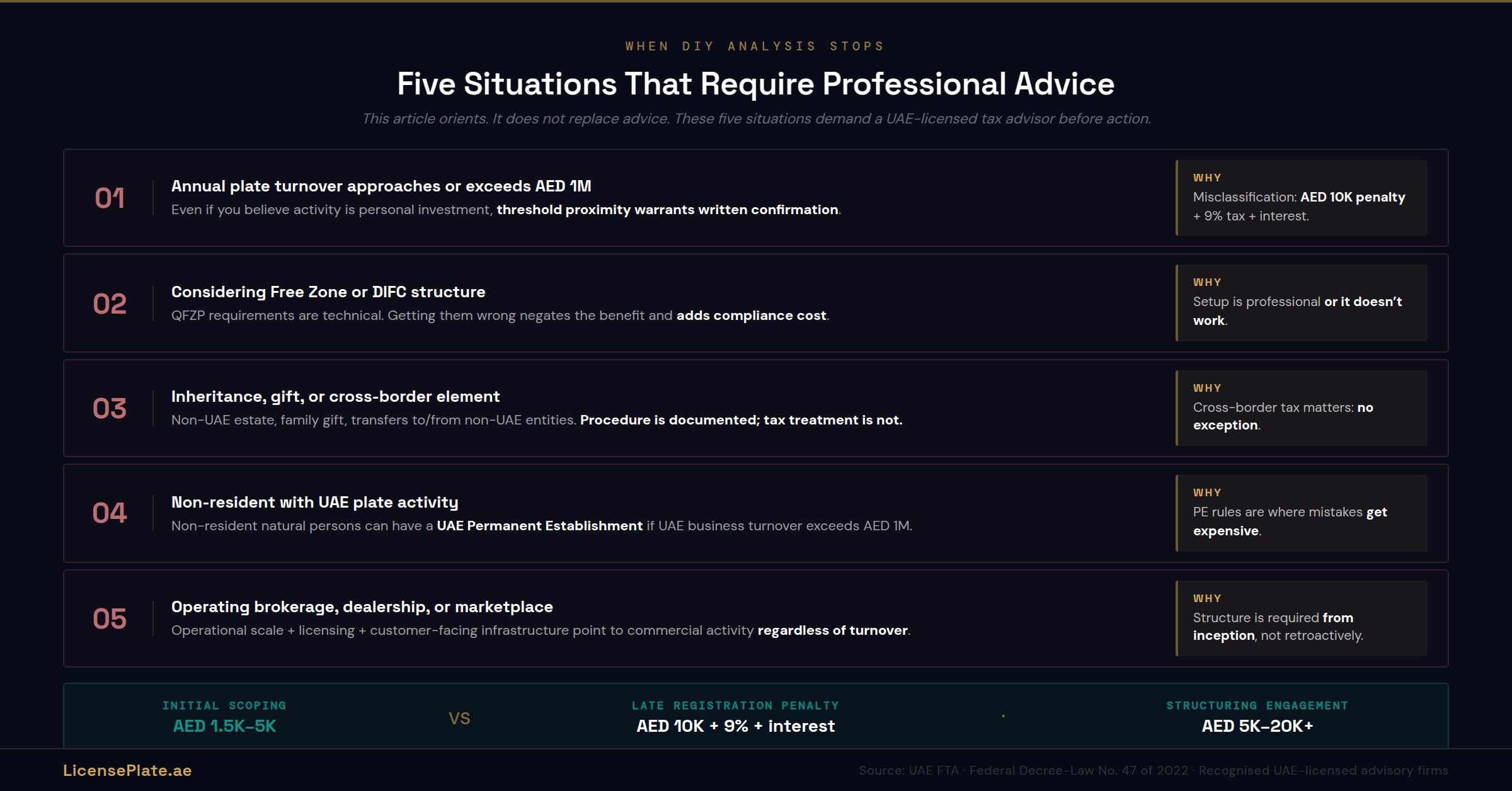

This piece exists to orient. It does not replace professional advice. Five specific situations require a UAE-licensed tax advisor consultation before acting, regardless of how much you have read on the topic:

Situation 1: Annual plate turnover approaches or exceeds AED 1 million. Even if you believe the activity is personal investment, the threshold proximity warrants written professional confirmation. Misclassification carries AED 10,000 late-registration penalty plus 9% on profits above AED 375,000 plus interest.

Situation 2: You are considering a Free Zone or DIFC structure. These structures are sophisticated, the QFZP requirements are technical, and getting them wrong negates the tax benefit and adds compliance cost. Professional setup is essential.

Situation 3: You have plate inheritance, gift, or cross-border elements. Inheritance from a non-UAE estate, plates gifted between family members, plates transferred to or from non-UAE entities all introduce complexity. The inheritance guide covers the procedural mechanics, but the tax treatment requires advisor input.

Situation 4: You are a non-resident with UAE plate activity. Per DLA Piper's analysis of the FTA Non-Resident Persons Guide, non-resident natural persons can have a UAE Permanent Establishment if their UAE business turnover exceeds AED 1 million. Cross-border plate activity is where mistakes get expensive.

Situation 5: You are operating a plate brokerage, dealership, or marketplace. The operational scale, the licensing question, and the customer-facing infrastructure all point to commercial business activity regardless of turnover. Sole-proprietor or company structuring is required from inception, not retroactively.

UAE-licensed tax advisors who handle natural-person Corporate Tax matters charge typically AED 1,500–5,000 for an initial scoping consultation and AED 5,000–20,000+ for structuring engagements. The cost is small relative to the AED 10,000 late-registration penalty plus the 9% rate plus interest that incorrect classification can trigger.

Frequently Asked Questions

Frequently Asked Questions

Q: If I sell one plate this year for AED 800,000, do I need to register for Corporate Tax?

Almost certainly not, if the plate was held as personal investment, you do not operate a website or marketing infrastructure for plate sales, and this is not a regular pattern. Personal investment income is exempt from Corporate Tax and does not count toward the AED 1 million threshold per the FTA's Natural Persons Guide. If unclear, consult a tax advisor before completing the sale.

Q: What counts toward the AED 1 million threshold?

Turnover (gross revenue, not profit) from business or business activities conducted in the UAE within a Gregorian calendar year (January to December). Wages, personal investment income, and real estate investment income are explicitly excluded from the calculation. The threshold is per natural person, not per activity, so multiple business activities are aggregated.

Q: I bought four plates over the last two years. Am I a business?

Probably not, if the four plates were held for capital appreciation, you have not operated a website or paid advertising, and the activity has the character of building a personal collection rather than running a trading operation. Four transactions over two years (two per year) is typically too low frequency to constitute commercial trading. If turnover from the resales approaches AED 1 million in any calendar year, professional advice is appropriate.

Q: Can I avoid Corporate Tax by structuring through a Free Zone company?

Possibly, but with conditions. Free Zone Persons can benefit from 0% Corporate Tax on Qualifying Income, but UAE-mainland plate trading typically does not qualify. A Free Zone structure works best when the entity also has substantial international or qualifying-activity income. For pure UAE plate trading, the Free Zone benefit is limited and the operational cost (license fees, substance requirements) is real. Professional structuring advice is essential before establishing such an entity.

Q: Does Small Business Relief apply to plate flippers?

Yes, if eligible. Businesses with revenue at or below AED 3 million per tax period can elect Small Business Relief and effectively pay no Corporate Tax for that period. Available for tax periods ending on or before 31 December 2026 as a transitional measure. Election is not automatic and must be claimed on the annual return. Suitable for plate flippers operating just above the AED 1M registration threshold.

Q: What happens if I do not register and the FTA later determines I should have?

Late registration penalty is AED 10,000. Late filing penalty is AED 500 per month for the first 12 months, AED 1,000 per month thereafter. Plus the underlying Corporate Tax owed plus interest. The FTA can assess up to five years backward. Registration is a one-time administrative step; the cost of missing it compounds quickly.

Q: Are plates inherited from family members taxable?

No, the inheritance itself is not taxable in the UAE. The Personal Investment exclusion covers plates received as inheritance and any subsequent sale by the heir is treated as personal investment disposition. The mechanics of plate inheritance are covered in the inheritance guide. Tax advisor input is appropriate where the estate has cross-border elements or where the heir already operates plate-trading activity.

Q: I am a non-UAE resident. Does Corporate Tax apply to my UAE plates?

Possibly, depending on the structure of your activity. Per the FTA Non-Resident Persons Guide, a non-resident natural person can have a UAE Permanent Establishment if UAE business turnover exceeds AED 1 million. Passive ownership of plates as personal investment typically does not trigger this. Active plate trading by a non-resident likely does. Cross-border tax matters require professional advice without exception.

The UAE remains one of the most tax-efficient jurisdictions for personal investment in the world. The 0% personal income tax, 0% capital gains tax on personal assets, and the broad personal investment exemption from Corporate Tax mean that the typical plate buyer holding one to three plates for capital appreciation owes zero tax on appreciation gains. That advantage is real and durable.

What the 2023 Corporate Tax framework changed is the treatment of plate activity that has commercial characteristics: high frequency, advertising infrastructure, profit-seeking intent at acquisition, and turnover approaching AED 1 million. For that activity, registration, returns, and 9% Corporate Tax above AED 375,000 are obligations, not options.

Most plate buyers do not need to act on this article. A small minority do. The piece exists to help readers identify which group they belong to and to give the smaller group enough orientation to know what questions to ask their tax advisor. Read the Investment Guide for the foundational tier and returns analysis. Read the Portfolio Construction framework for multi-plate architecture that supports personal-investment classification. Use the plate calculator for any plate you are evaluating. And when your activity grows past two or three transactions per year, build the relationship with a UAE-licensed tax advisor before you need it.

⚠ Important: This article is general informational content, not tax advice. UAE Corporate Tax law is complex and the FTA's interpretation of natural-person business activity continues to evolve. Anyone whose plate activity may approach or cross the AED 1 million turnover threshold, or who is structuring a holding entity, should consult a UAE-licensed tax advisor before relying on any framework in this piece. The ultimate authority is the Federal Tax Authority's published guidance and the Federal Decree-Law No. 47 of 2022, not this article.

Delete Comment?

Are you sure you want to delete this comment? This action cannot be undone.

Delete Article?

Are you sure you want to delete this article? This will also delete all comments. This action cannot be undone.