The Plate Investment Portfolio Construction Framework: How to Build a Diversified UAE Plate Holding

April 27, 2026

Dubai

LicensePlate.ae Team

If you own one plate, you have a transaction. If you own three plates that are all four-digit Dubai plates on mid codes, you have three transactions in the same exposure. The plates are different numbers but the same bet. That is not a portfolio. That is a concentrated position dressed up as diversification.

This is the gap that nobody writing about UAE plates has addressed properly. The library has explained how individual plates appreciate, what tiers exist, how returns differ across digit counts. The UAE plates as investment guide lays out the foundation. The 20% returns analysis documents the actual data. The plates vs gold vs real estate piece benchmarks the asset class. What no piece has done yet is move from single-asset analysis to multi-asset architecture, which is the question every serious investor reaches once they own more than one plate.

This article publishes that framework for the first time. It is built for investors holding three or more plates or planning to build to that threshold. Family offices treating plates as an alternative-asset allocation. Dealers building inventory positions. High-net-worth individuals who have already bought their identity plate and now want to construct a meaningful holding. The framework draws on portfolio-construction principles from comparable alternative-asset classes (classic cars, fine wine, art) but adapts them to the structural realities that make plates different from any of those markets.

Why Plates Are Not a Category Exposure

Before any allocation framework, the structural difference. In equities, you can own “the market” through an index fund. In gold, you can own “gold” through a bullion holding. In classic cars, the Hagerty Blue Chip Index tracks an aggregate basket. In fine wine, the Liv-ex 1000 gives you an index-level exposure. Each of these markets has aggregate instruments that let an investor express a view on the asset class without picking individual assets.

UAE plates have nothing equivalent. There is no Dubai Plate Index. There is no securitised vehicle that holds a basket of plates. Every transaction is an individual plate purchased at an individual price. The buyer takes on the full idiosyncratic risk of that specific number on that specific code in that specific emirate. If the number falls out of cultural favour, no diversification within the same code helps. If the emirate authority changes the issuance pattern (as Sharjah did with its 2026 design transition), every plate in that emirate is affected simultaneously.

This makes plate portfolio construction structurally closer to coin collecting than to equity investing. The diversification that actually reduces risk happens across three dimensions: across tiers (different supply-demand dynamics), across emirates (different regulatory regimes and demand pools), and across codes within an emirate (different cohort effects and cultural associations). Buying two three-digit AA-code plates is not diversification. It is concentration.

Once that point is internalised, the rest of the framework follows naturally.

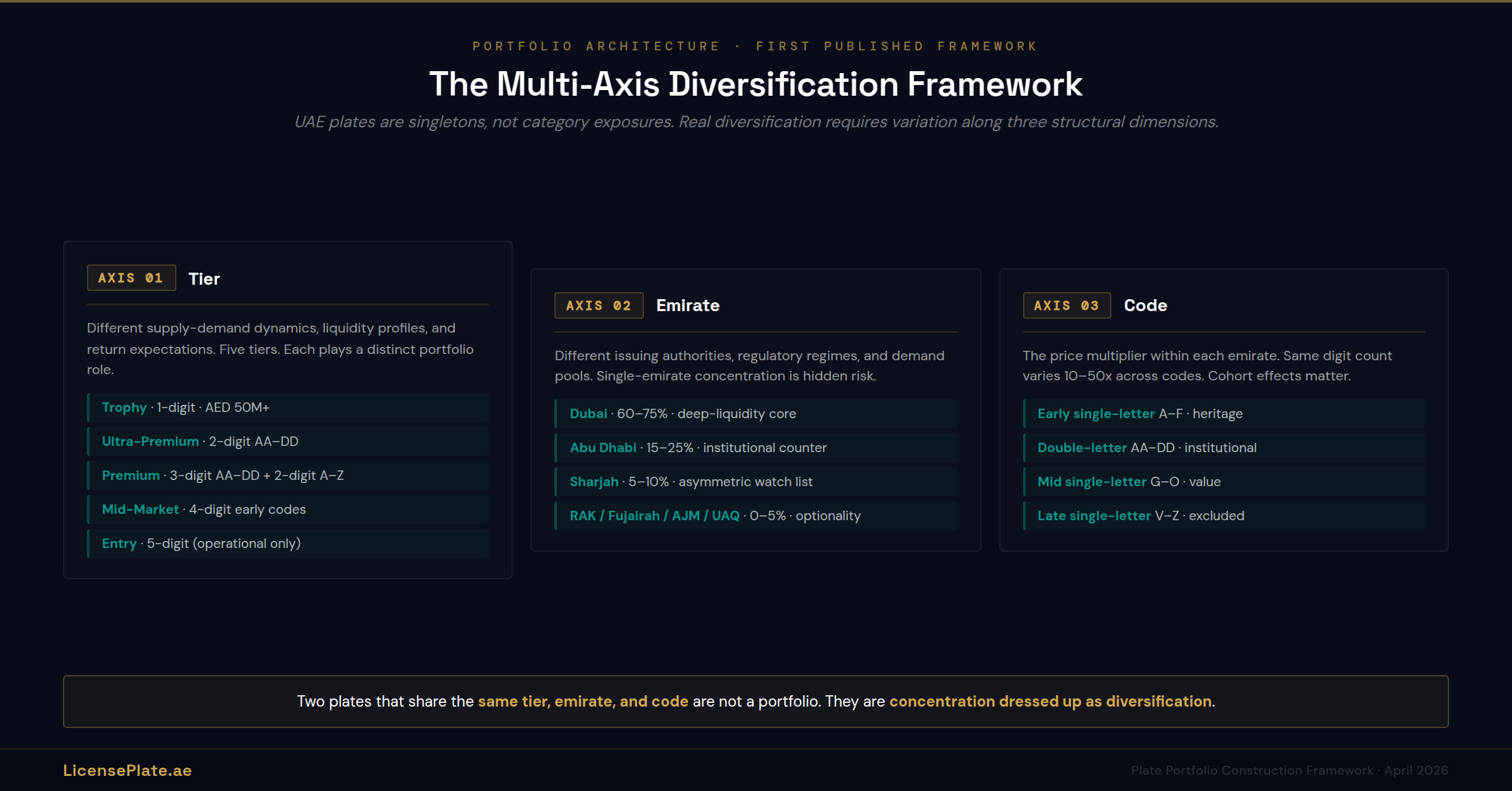

Axis 1: Tier Allocation

The five-tier framework that runs through the entire library is the first axis of portfolio construction. Each tier has different supply-demand dynamics, different liquidity profiles, different return expectations, and different roles in a multi-plate holding. The full tier definitions are in the plate glossary, and the tier-by-tier 2026 benchmarks are documented in the Half-Year Review. Here is how each tier should function within a portfolio:

Trophy Tier (1-digit plates, AED 50M+): 0% allocation for most investors

Trophy plates are not investments in the conventional sense. They are identity-and-philanthropy assets purchased by ultra-high-net-worth individuals at charity auctions where bid dynamics are driven by social positioning, not return expectations. The Most Noble Number 2026 event cleared DD 6 at AED 37M against an event total of AED 1.136 billion including pledges. For a portfolio investor with AED 5M to deploy across plates, a single Trophy Tier plate would be 100% of their capital and zero diversification. Allocate 0% unless you are a UHNW principal whose portfolio holds Trophy as a separate identity asset distinct from your investment exposure.

Ultra-Premium Tier (2-digit plates on AA/BB/CC/DD, AED 5–40M): 10–20% allocation for AED 10M+ portfolios

Ultra-Premium plates function as the portfolio’s store-of-value layer. Liquidity is moderate (these plates do trade, but transaction frequency is measured in months, not days). Returns track sideways to slightly higher year-over-year, with the March 2026 DD-code repricing (DD 16 at AED 9M, DD 99 at AED 8.9M) confirming that newer double-letter codes now trade at par with older BB/CC codes. For portfolios above AED 10M, Ultra-Premium represents the appropriate “vault” allocation. Below AED 10M, this tier is too capital-intensive and concentration becomes unavoidable.

Premium Tier (3-digit plates on AA/BB/CC/DD + 2-digit on A–Z, AED 200K–6M): 40–60% allocation, the portfolio core

This is the investment sweet spot. The price check article documents the tier benchmarks: AA 707 at AED 3.31M (April 2025), BB 777 at AED 6M (September 2025), DD 100 at AED 5.1M (March 2026). Premium plates have the best combination of return potential, liquidity, and tier depth. Multiple plates can be held within this tier without concentration because the underlying numbers and codes vary enough to provide intra-tier diversification. For most serious portfolios, Premium is the largest single allocation. The car-plate pairing economics piece documents why three-digit plates with model-number significance (458, 911, 770) command additional resale premiums.

Mid-Market Tier (4-digit plates, AED 30K–250K): 20–30% allocation, the growth layer

Mid-Market is where percentage returns are highest historically (the Investment Guide documents 4-digit plates that tripled from AED 5K to AED 25K) but tier-quality matters enormously. Only early codes (A through D) carry the fixed-supply dynamic that drives appreciation. Mid-codes (H through N) trade in the AED 30K–80K band but are vulnerable to RTA fixed-price supply releases (the May 2025 release of 4-digit plates on codes L and M at AED 95K is a documented example). Late codes (V through Z) should be excluded from a portfolio at this tier. The 20–30% allocation goes specifically to early-code Mid-Market plates, not generic 4-digit plates.

Entry Tier (5-digit plates, AED 3–15K): 0–5% allocation, only for completeness

Entry Tier plates are functional registrations, not investments. The library’s ten expensive mistakes article identifies treating five-digit late-code plates as appreciating assets as one of the most common errors. The only reason to include Entry Tier in a portfolio is if you need a plate registered to a specific vehicle for operational reasons (the Anatomy article covers the lifecycle), and you happen to hold it long enough that incidental appreciation occurs. For pure investment allocation, target 0%.

Axis 2: Emirate Diversification

The seven emirates run plate systems that are structurally similar but operationally independent. Different issuing authorities, different code formats, different cultural hierarchies, different demand pools. A pure-Dubai plate portfolio is exposed to any single regulatory or cultural shift in Dubai. Diversifying across emirates is the second axis.

Dubai: 60–75% allocation, the deep-liquidity core

Dubai is the most liquid, most traded, and most documented plate market in the UAE. Every tier benchmark in this article comes from Dubai data because Dubai data is the most reliable. The 60–75% allocation reflects the tradeoff: Dubai concentration is a risk, but Dubai liquidity is a benefit. The Dubai number plates complete guide covers the code system, auction calendar, and secondary market mechanics in full.

Abu Dhabi: 15–25% allocation, the institutional counter-weight

Abu Dhabi runs a different category system (numerical category codes rather than letter codes), uses Emirates Auction as the primary secondary-market platform, and has documented institutional buyer behaviour at scale. The Abu Dhabi Mobility Most Noble Number online auction in March 2026 cleared AED 119.4M across 555 plates with a different distribution profile than Dubai’s concentrated event. The Abu Dhabi plates complete guide covers the category system. For portfolio purposes, Abu Dhabi exposure provides regulatory diversification: a Dubai-only portfolio shares regulatory risk; a Dubai-plus-Abu-Dhabi portfolio does not.

Sharjah: 5–10% allocation, the asymmetric watch list

Sharjah’s 2026 design transition created a fixed-supply dynamic on pre-2025 design plates that the secondary market has not yet priced in. The Sharjah design analysis projects that pre-transition plates will develop a collector premium over multi-year holds, similar to how UK plate format transitions produced premiums on pre-1963 and pre-2001 issuance. Allocating 5–10% to Sharjah captures this asymmetric upside without overcommitting to a thesis that has not yet played out. Browse current Sharjah listings for entry pricing.

RAK, Ajman, Fujairah, Umm Al Quwain: 0–5% allocation, the optionality bucket

The smaller emirate plate markets are illiquid but offer optionality. RAK is the most interesting given the Wynn Al Marjan Island development and the RAK number plates guide covers the demand thesis. Fujairah has the East Coast tourism angle covered in the Fujairah guide. Ajman and Umm Al Quwain are small enough that the Ajman vs UAQ comparison treats them as a single pair. Allocate to these emirates only if your portfolio is large enough that 5% represents meaningful capital deployment, and only if you have a specific thesis on the emirate’s growth trajectory.

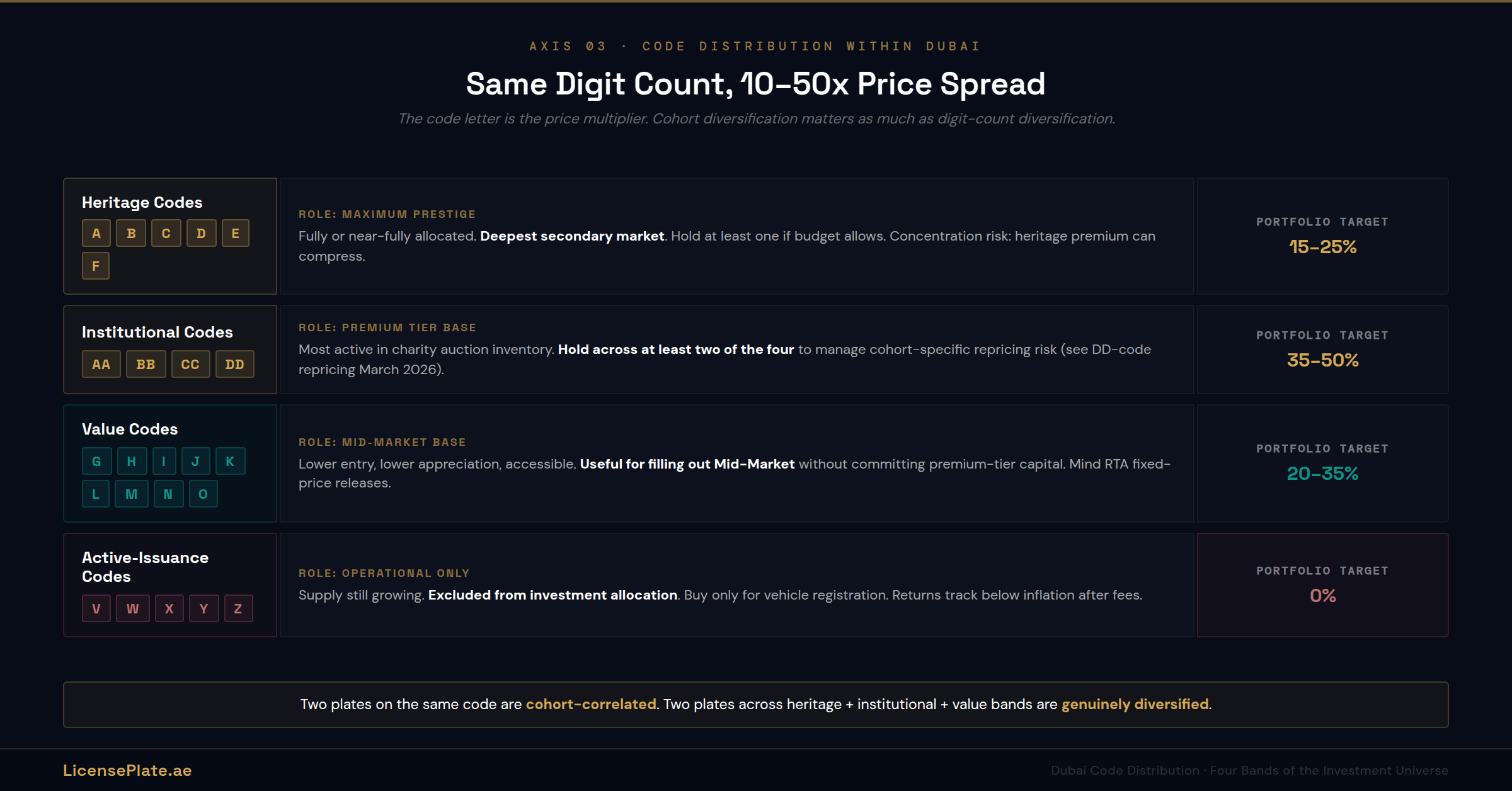

Axis 3: Code Distribution Within Dubai

The code letter is the price multiplier. Within Dubai, the same digit count on different codes can vary by 10-50x in price. Within a portfolio, code diversification is the third axis. The visual decoder covers how to read codes; here is how to allocate across them:

Single-letter early codes (A, B, C, D, E, F): These are the heritage codes. Fully or near-fully allocated for premium digit counts. Maximum prestige, maximum price, deepest secondary market. A portfolio should hold at least one early-code plate if budget allows. Concentration risk: heritage premium can compress if institutional buyers shift to double-letter codes.

Double-letter codes (AA, BB, CC, DD): These are the institutional codes. Premium tier base. Most active in charity auction inventory. The DD-code repricing in March 2026 (DD 16 at AED 9M reaching parity with BB/CC benchmarks) confirms that double-letter codes are trading as a coherent peer group rather than a hierarchy. A portfolio benefits from holdings across at least two of the four double-letter codes to manage cohort-specific repricing risk.

Single-letter mid codes (G, H, I, J, K, L, M, N, O): These are the value codes. Mid-Market tier base. Lower entry prices, lower appreciation rates, but proportionally accessible. Useful for filling out a portfolio at the Mid-Market tier without committing premium-tier capital. The mid-code 4-digit plates released by the RTA at AED 95K in May 2025 set a benchmark for this segment.

Single-letter late codes (V, W, X, Y, Z): These are the active-issuance codes. Excluded from investment allocation. Supply is still growing. Buy these only for operational vehicle registration, not portfolio construction.

Liquidity-Tier Matching: How Long Can You Lock Up Capital?

Liquidity-Tier Matching: How Long Can You Lock Up Capital?

Every plate tier has a different liquidity profile. Matching your portfolio’s tier mix to your capital lock-up tolerance is the fourth and most under-discussed dimension of plate portfolio construction.

Trophy Tier liquidity: indefinite. Single-digit plates trade every 5–15 years, often at charity auctions. If you need to exit within 24 months, do not buy Trophy.

Ultra-Premium Tier liquidity: 6–18 months to sell at fair value. Two-digit double-letter plates are sold via private sale, broker-mediated transactions, or strategic placement at charity auctions. Forced sales typically clear at 60–75% of fair value. Plan to hold at least 3 years.

Premium Tier liquidity: 2–6 months to sell at fair value. This is the most liquid premium-tier inventory in the UAE. The LicensePlate.ae marketplace lists thousands of three-digit plates with active buyer-side demand. Plan to hold at least 12 months.

Mid-Market Tier liquidity: 1–3 months to sell at fair value. Four-digit plates on early and mid codes have the broadest buyer pool and the most active secondary market. The how-to-sell guide covers the full process.

Entry Tier liquidity: 2–8 weeks. Five-digit plates clear quickly at low prices. Liquid but not appreciating.

The portfolio implication: if your investment horizon is 3 years, your portfolio should be heavily weighted toward Premium and Mid-Market. If your horizon is 10+ years, Ultra-Premium becomes appropriate. If your horizon is indefinite (a generational holding), Trophy becomes appropriate. Mismatching your liquidity profile to the tier mix is the single most common cause of forced losses in plate portfolios.

Correlation With Other UAE Asset Classes

Why hold plates at all when UAE real estate, gold, and equities are accessible? The plates vs gold vs real estate analysis covers the full comparison. The portfolio-relevant point: plates exhibit low correlation with each of these asset classes, which makes them additive to a UAE-focused alternative-asset portfolio rather than redundant. Three observations:

First, plates are uncorrelated with UAE real estate cycles. Real estate transactions are sensitive to interest rates, mortgage availability, and developer launch cycles. Plate transactions are not. Premium-tier plate appreciation continued through 2024–2025 even as Dubai luxury real estate experienced quarterly volatility.

Second, plates are uncorrelated with gold. Gold tracks global macro factors (USD strength, real rates, central bank flows). Plates track UAE-specific demand from luxury car buyers and charity auction participants. The Bryant University study on classic cars and fine wine identified ~5% alpha with near-zero systematic risk, and the structural similarities between classic cars and plates suggest a similar risk profile applies.

Third, plates are correlated with UAE luxury car demand. This is the one correlation that does exist and that does matter. DubiCars data showed 104% growth in the AED 600K–AED 1M car segment in H1 2025, which corresponded to strong premium-plate demand through the same period. The car-plate pairing economics piece documents the linkage. For portfolio risk monitoring, UAE luxury car sales data is the single most useful leading indicator for premium-plate demand.

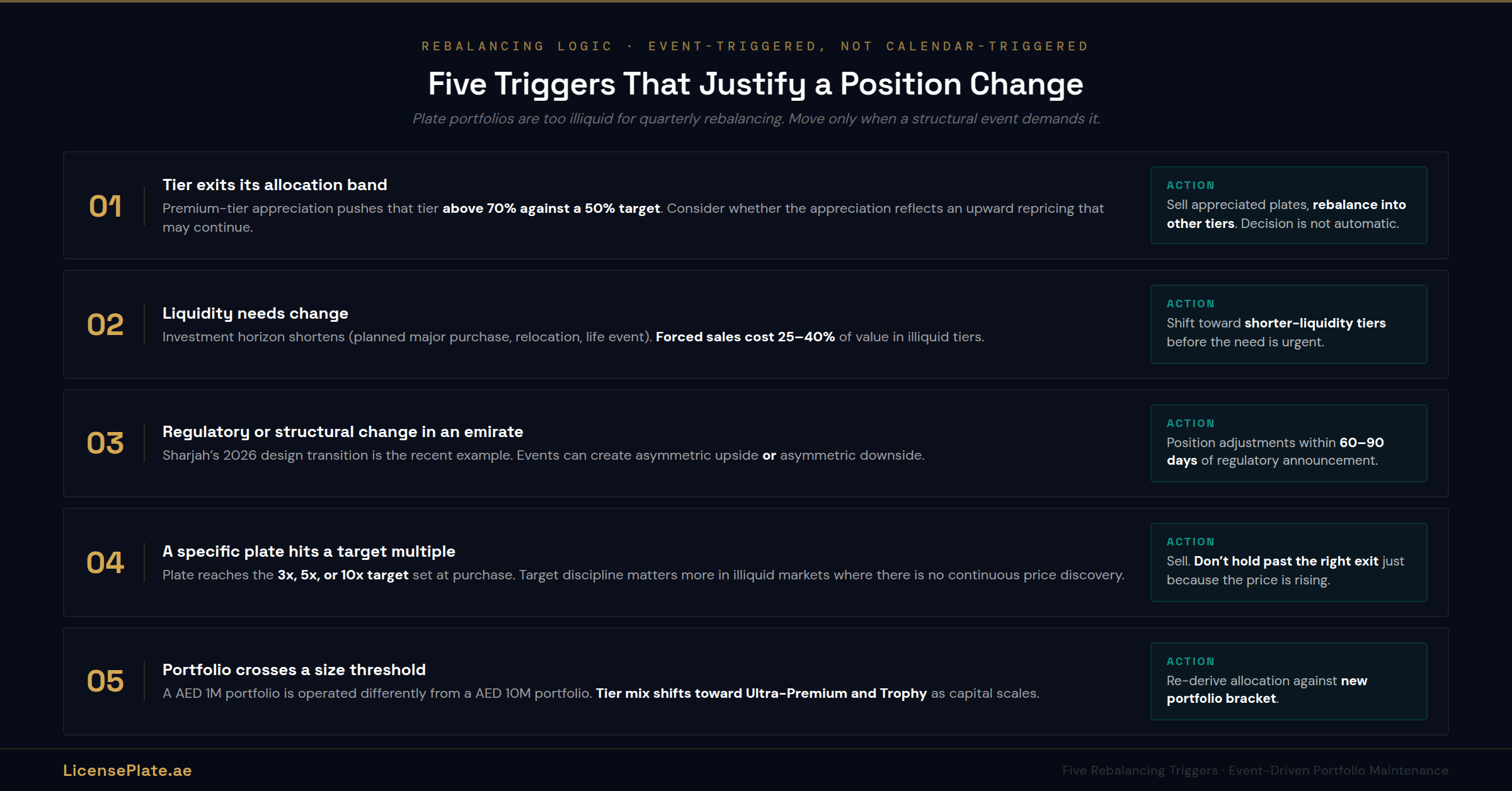

Rebalancing Logic: When to Sell, When to Add

Plate portfolios should not be rebalanced like equity portfolios. Transaction costs are too high (the transaction anatomy documents the full cost structure), and forced sales destroy value in illiquid tiers. The right approach is event-triggered rebalancing rather than calendar-triggered.

Trigger 1: A tier exits its allocation band. If Premium-tier appreciation pushes that tier above 70% of portfolio value (against a 50% target), consider whether to sell the appreciated plates and rebalance into other tiers. Note: the appreciation itself often reflects an upward repricing that may continue, so the rebalancing decision is not automatic.

Trigger 2: Liquidity needs change. If your investment horizon shortens (planned major purchase, relocation, life event), the portfolio mix should shift toward shorter-liquidity tiers before the need is urgent. Forced sales at the wrong moment cost 25–40% of value in illiquid tiers.

Trigger 3: A regulatory or structural change in an emirate. Sharjah’s 2026 design transition is a recent example. Such events can either create asymmetric upside (the pre-transition collector premium thesis) or asymmetric downside (if the transition creates depreciation in any specific category). Position adjustments should follow within 60–90 days of the regulatory announcement.

Trigger 4: A specific plate hits a target multiple. If you bought a plate with an explicit target return (3x, 5x, 10x), and the plate reaches that multiple, sell. Target discipline matters more in illiquid markets than in equity markets because the absence of continuous price discovery makes it easier to hold past the right exit.

Trigger 5: Your portfolio crosses a size threshold. A AED 1M plate portfolio is operated differently from a AED 10M plate portfolio. As capital scales, the right tier mix shifts toward Ultra-Premium and Trophy. The 5–10% allocation rule that fits a AED 1M portfolio may produce concentration when applied unchanged to a AED 10M portfolio.

Five Portfolio Mistakes That Cost Real Money

Mistake 1: Concentrating in a single emirate. Three Dubai plates in three different tiers is not diversified if all three depend on Dubai-specific regulatory and demand dynamics. The cross-emirate transfer guide covers how to add Abu Dhabi or Sharjah exposure if your portfolio currently runs Dubai-only.

Mistake 2: Treating two plates on the same code-and-digit-count as diversification. Holding AA 458 and AA 911 looks diverse but is not. Both plates are exposed to AA-code repricing, three-digit plate cohort effects, and Dubai-specific demand. True diversification requires the second plate to differ in at least one structural dimension (different code, different digit count, or different emirate).

Mistake 3: Buying late-code Mid-Market plates as investments. The May 2025 RTA release of 4-digit plates on codes L and M at AED 95K demonstrated that the RTA can release supply that compresses secondary-market pricing on comparable plates. Mid-Market should be early-code only. The ten expensive mistakes article covers this trap in depth.

Mistake 4: Ignoring transaction costs in expected returns. Plate transactions cost more than equity transactions. The cost of ownership breakdown documents the full fee structure. A plate that appreciates 15% but generates 5% in transaction costs at sale produces a 10% net return, not 15%. Build transaction cost assumptions into every target return.

Mistake 5: Not insuring or documenting the holdings. Plate ownership is documented through the RTA system, but physical plates can be damaged, lost, or affected by vehicle incidents. The plate insurance guide covers what protection exists and what does not. The inheritance guide covers what happens to plate holdings on the owner’s death. Both are non-negotiable for any portfolio above AED 1M.

Frequently Asked Questions

Q: What is the minimum portfolio size where construction matters?

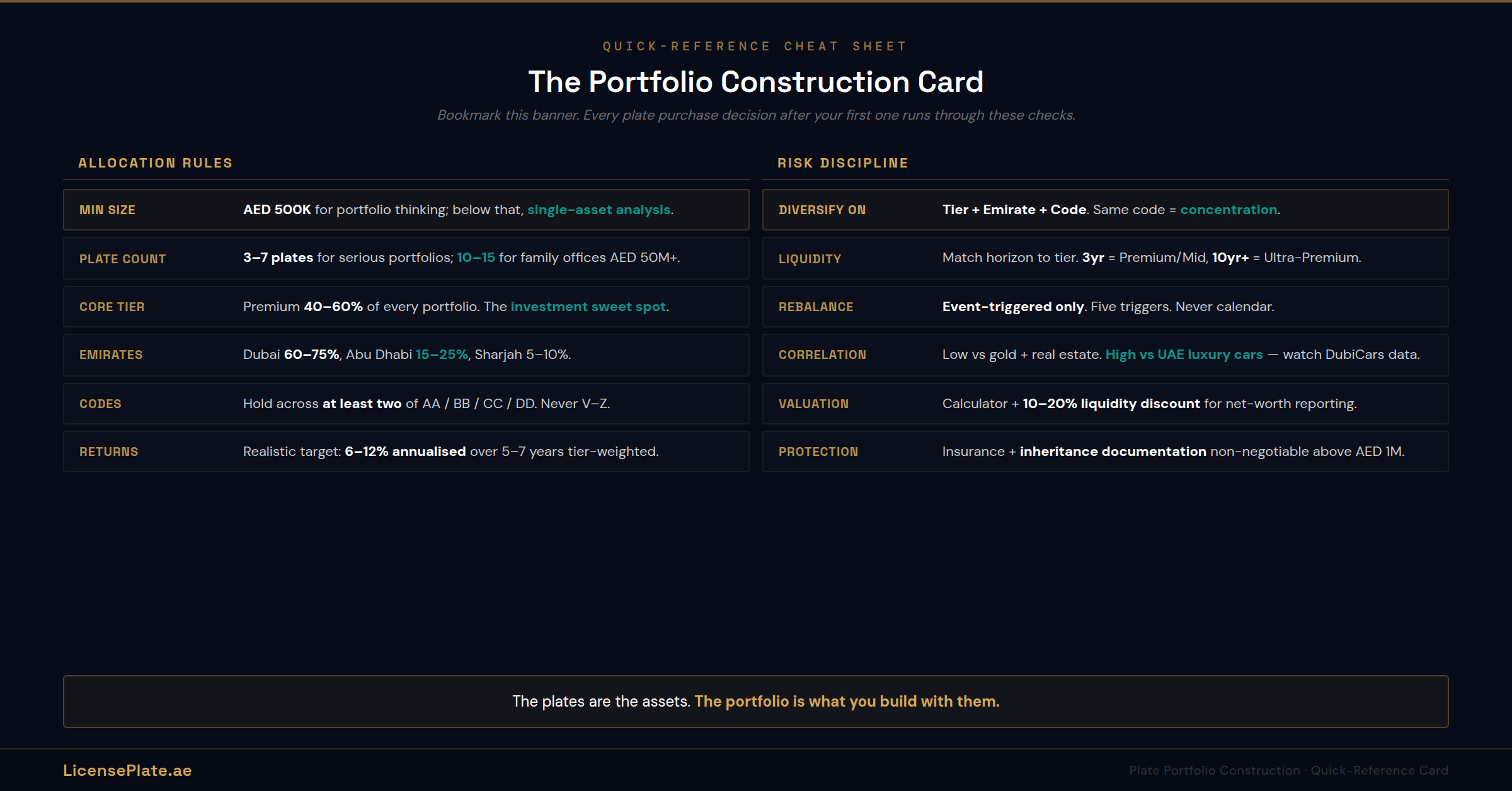

Approximately AED 500K. Below that level, you are buying one or two plates and the right framework is single-asset analysis (covered by the Investment Guide and the Price Check article). Above AED 500K, the question shifts from “which plate?” to “which combination of plates?” and portfolio construction becomes the relevant analysis.

Q: How many plates should a typical investor hold?

Three to seven for most serious portfolios. Three plates is the minimum for meaningful diversification across tiers, emirates, or codes. Seven is the practical maximum before management complexity outweighs the diversification benefit. Family offices managing AED 50M+ allocations may hold ten to fifteen plates.

Q: Should I hold plates in my personal name or through a structure?

For most UAE residents, personal ownership is the standard approach because UAE personal capital gains tax is 0%. Structure-based ownership (through a UAE company or DIFC vehicle) becomes relevant for portfolios above AED 5M, for non-residents, or where succession planning matters. Consult a UAE tax and legal advisor before structuring above AED 5M.

Q: How do I value an entire plate portfolio for net-worth purposes?

Use the LicensePlate.ae plate calculator for each plate as the base estimate, then apply a 10–20% liquidity discount for net-worth reporting purposes (because forced sales would clear below market). Update valuations quarterly using the Half-Year Review benchmarks as the data anchor.

Q: What rebalancing frequency makes sense?

No fixed frequency. Plates are too illiquid for calendar-driven rebalancing. Use event-triggered rebalancing as covered above: tier band breaches, liquidity needs, regulatory events, target multiples, or portfolio size thresholds.

Q: Can I borrow against my plate portfolio?

Yes, through plate-backed lending. The plate-backed lending piece covers the full UAE B2B credit market built on premium plate collateral. Typical loan-to-value ratios run 30–50% for Ultra-Premium plates with shorter tenors than mortgage-backed lending.

Q: Should I include plates in inheritance planning?

Yes, particularly for portfolios above AED 1M. The inheritance guide covers the legal mechanics. Plates pass through UAE inheritance law in the same manner as other personal assets, but the documentation requirements (Plate Ownership Certificates, traffic file records) are specific. Family offices should maintain a plate inventory document with current values updated quarterly.

Q: What is the realistic expected return for a diversified plate portfolio?

Tier-weighted, a properly constructed portfolio targets 6–12% annualised returns over a 5–7 year horizon, with material variance by tier and emirate. The 20% returns analysis breaks down where the higher historical returns came from (specific tier and code combinations) and where they did not. A portfolio averaging 6–12% with low correlation to UAE equities and real estate is the realistic positioning, not 20% across the board.

A plate portfolio is not built by buying more plates. It is built by buying plates that differ from each other in the structural dimensions that matter: tier, emirate, code, digit count, liquidity profile, and exposure to specific cultural or regulatory dynamics. Three plates that look different on paper but share the same structural exposures are still concentration. Three plates that differ along multiple axes are a portfolio.

The framework above is the first published architecture for that question. It will evolve as the market generates more data and as the LicensePlate.ae library publishes the methodology document and the Monthly Market Index that this piece anticipates. For now, use it as the structural lens for every plate purchase decision after your first one.

Start with the plate calculator for any specific plate you’re evaluating. Browse Dubai listings, Abu Dhabi listings, and Sharjah listings by tier rather than by individual plate when building a portfolio view. Read the Investment Guide for tier-specific data and the Half-Year Review for current 2026 benchmarks. The plates are the assets. The portfolio is what you build with them.

Delete Comment?

Are you sure you want to delete this comment? This action cannot be undone.

Delete Article?

Are you sure you want to delete this article? This will also delete all comments. This action cannot be undone.