What Happens to Your Number Plate if Your Car is Totalled? The UAE Insurance Guide Nobody Writes

April 09, 2026

Dubai

LicensePlate.ae Team

It is a Tuesday morning in March, around 8:20. A Dubai resident is driving east on Sheikh Zayed Road toward Downtown, heading to a meeting at the DIFC Gate building. Two lanes over, a driver in a rented SUV misjudges the traffic ahead, brakes late, and collides with the rear quarter panel of the resident’s Mercedes S-Class. The impact spins the Mercedes into the central barrier. Airbags deploy. Both drivers walk away. The Mercedes does not. By the time the tow truck arrives forty minutes later, the car is unrecognisable. Dubai Police issue a report. The insurer is called.

Four days later, the resident is sitting in his insurer’s claims office in Al Barsha. The adjuster has finished the valuation. The repair estimate exceeds 50% of the pre-accident market value of the car, which triggers the total-loss clause in the Unified Motor Vehicle Insurance Policy. The insurer offers a settlement. The Mercedes was worth AED 340,000 at the time of the accident. After the 20% depreciation deduction mandated by the policy and the proportional time adjustment for the partial insurance period, the payout comes to roughly AED 248,000. The resident signs the paperwork. The adjuster slides over an ownership transfer letter for him to sign over to the insurer, along with the keys.

Here is what nobody told the resident. The plate on that Mercedes was a Dubai O 4-digit he had bought at an RTA auction four years earlier for AED 45,000. The calculator on LicensePlate.ae now values that same plate at approximately AED 165,000. It is not mentioned in the settlement paperwork. It is not mentioned by the adjuster. It is not mentioned in the police report. It exists inside the vehicle registration file as a linked asset, and the moment he signs the ownership transfer letter, his legal ability to separate that plate from the vehicle enters a narrow window that most owners never know exists. If he signs without asking, the plate is handled by the system default, which in most cases means it gets released back into the RTA pool alongside the vehicle’s registration cancellation.

This article is for the people who haven’t had the accident yet. It is also for the people who are in the middle of one right now and don’t understand why none of the insurance articles they’re reading mention their plate. The UAE motor insurance system treats vehicles. Plates sit quietly inside the registration file, valued by nobody, mentioned by no policy document, and decided in seventy-two hours by default rules that nobody tells you exist.

What the Unified Motor Insurance Policy Actually Covers

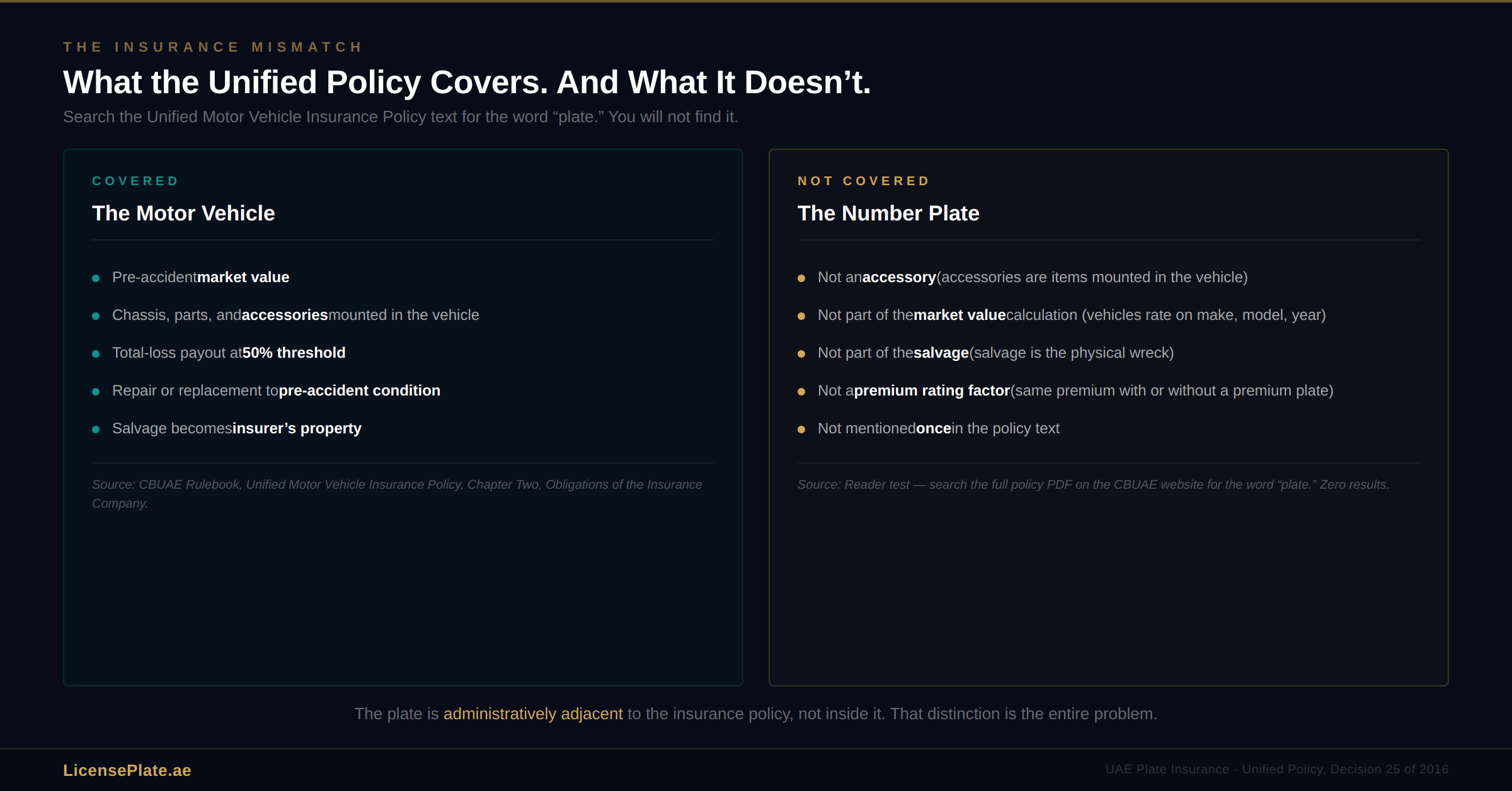

Every comprehensive motor insurance policy sold in the UAE is based on the Unified Motor Vehicle Insurance Policy Against Loss and Damage, issued under Insurance Authority Board of Directors’ Decision No. 25 of 2016. The Insurance Authority was absorbed into the Central Bank of the UAE (CBUAE) in 2021, and the CBUAE Rulebook now publishes this Unified Policy as the binding template for every motor insurer in the country. Read the full policy text and you will find detailed provisions covering the vehicle, the chassis, replacement parts, spare parts, depreciation schedules, salvage ownership, and dispute resolution. You will not find the word "plate" anywhere.

This is not an oversight. It reflects a structural reality of UAE motor insurance: the policy insures the motor vehicle, defined as the physical asset registered under a specific chassis number. The number plate is a separate administrative object that the RTA attaches to the vehicle registration file for identification purposes. The plate has its own ownership certificate, its own transfer process, and its own price tag. But it lives in a different administrative universe from the insurance policy that covers the car it is mounted on.

What the policy does cover

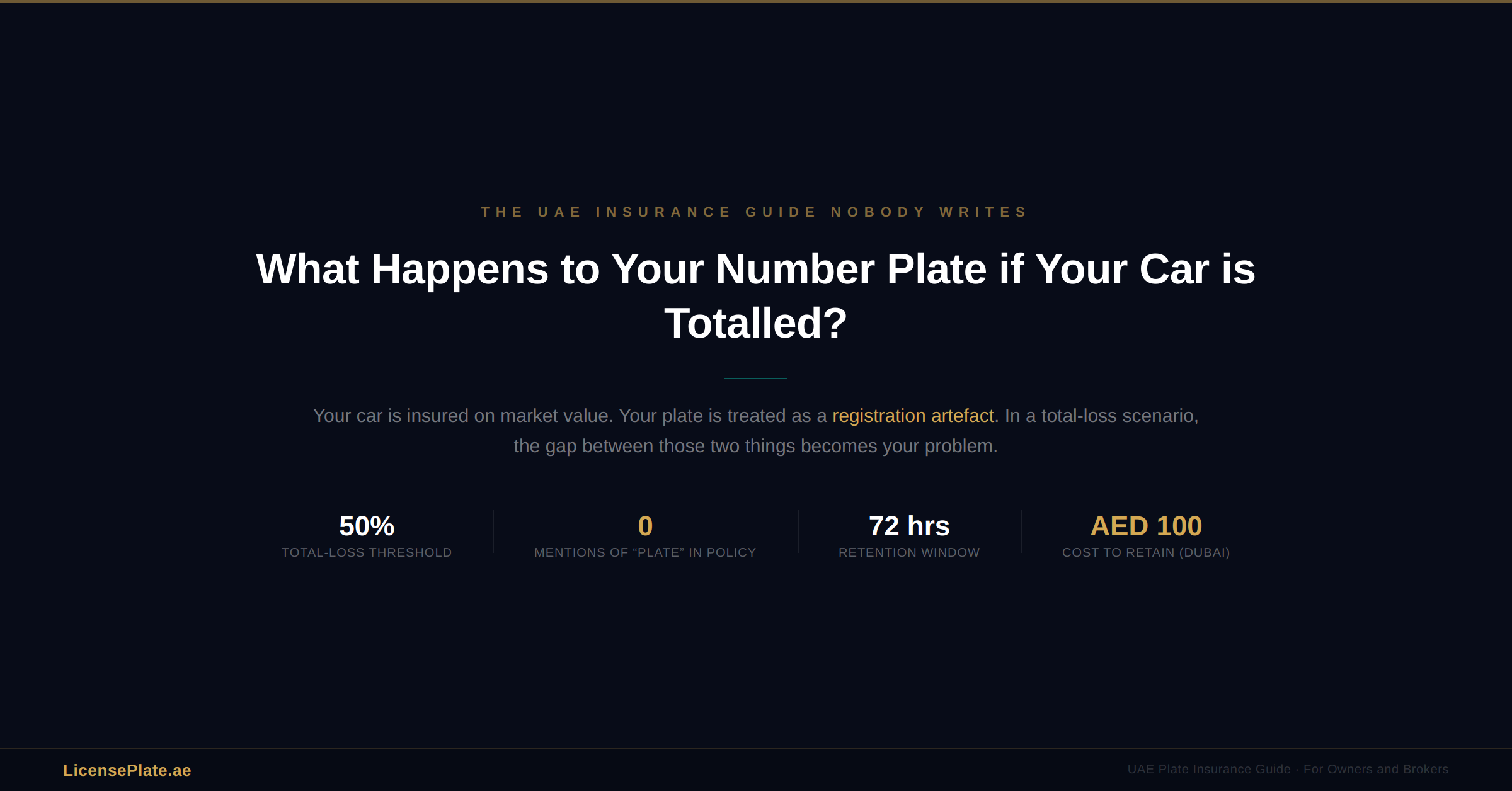

Chapter Two of the Unified Policy, which defines the insurer’s obligations, requires the company to compensate the insured for loss or damage to the vehicle and its accessories, restore the vehicle to its pre-accident condition through repair, or declare it a total loss when the repair cost threshold is crossed. The total-loss threshold is explicit: if the cost of repair exceeds 50% of the motor vehicle value before the accident, the vehicle is considered a total loss and the insured value becomes the basis for compensation, subject to a 20% depreciation deduction from the agreed insured value.

What the policy does not cover

The plate is not an "accessory" under any reasonable reading of the policy language, because accessories are defined as items mounted in the vehicle (sound systems, rear cameras, alloy wheels). The plate is not part of the vehicle’s market value calculation because insurers appraise vehicles on make, model, year, mileage, and condition, not on the administrative registration attached to them. The plate is not part of the salvage because salvage refers to the physical wreck, which the insurer takes possession of after settlement. Read the policy front to back and the plate simply does not appear, which is the problem.

The Total-Loss Process: What Actually Happens Step by Step

Understanding where the plate decision fits requires understanding the claim sequence as it runs in practice. The following is the standard flow for a total-loss claim in the UAE, reconstructed from the Unified Motor Vehicle Insurance Policy text, operational guidance published by major UAE insurance brokers including Savington, Policyhouse, and Insurance Market, and the CBUAE Rulebook.

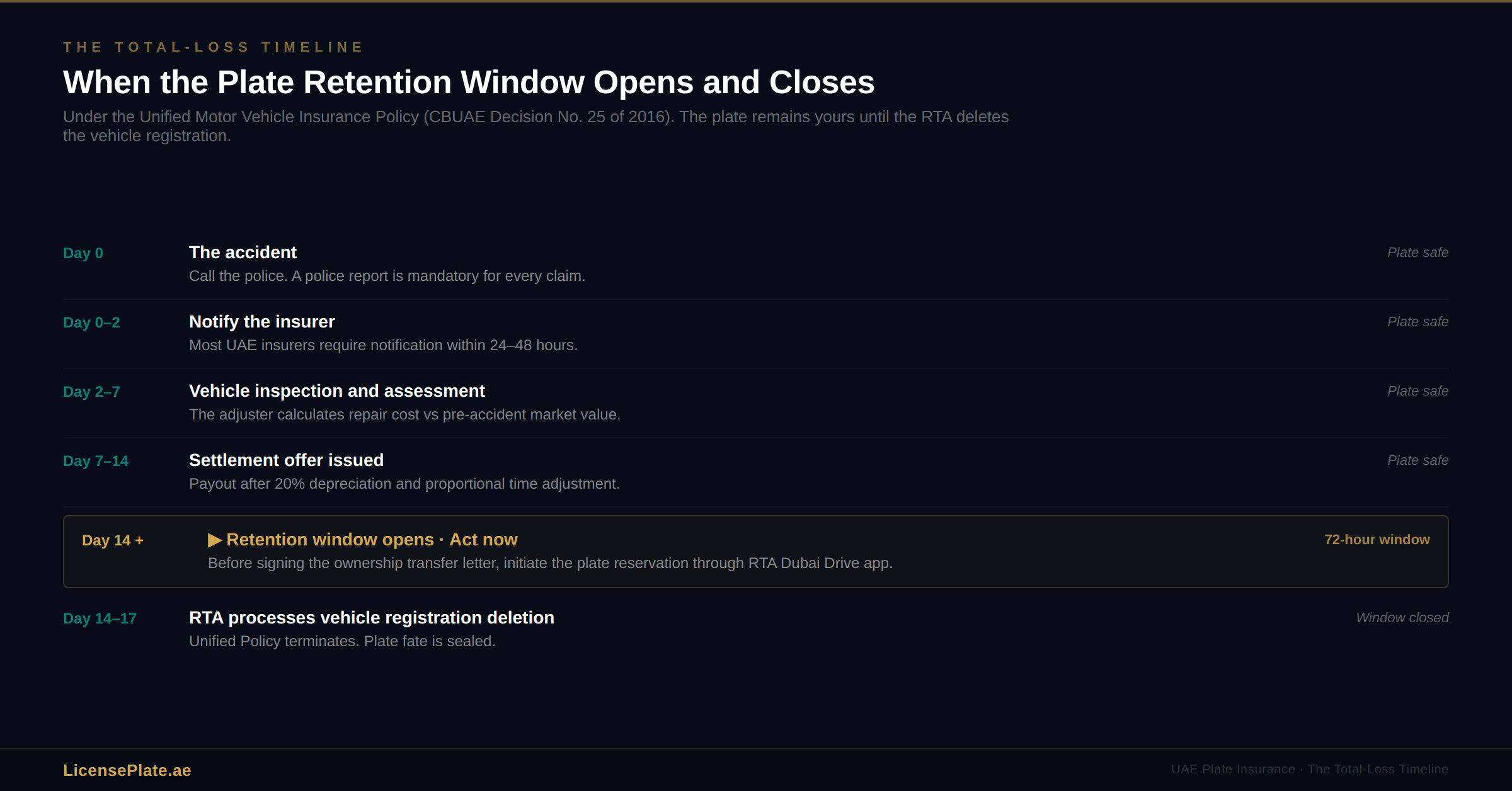

Day 0: The accident

Call the police. A police report is mandatory for every insurance claim in the UAE. No broker, no insurer, no court will accept a claim without one. The police issue a report that identifies the fault party, the circumstances, and the damage category. The report is your anchor document for everything that follows.

Day 0-2: Notify the insurer

Most UAE insurers require notification within 24 to 48 hours of the accident. Report by phone to the claims desk, provide the police report number, and follow up with photographs of the vehicle damage. The insurer assigns an adjuster.

Day 2-7: Vehicle inspection and assessment

The adjuster inspects the vehicle, usually at the insurer’s designated workshop or yard. They calculate the repair cost against the pre-accident market value. If the ratio crosses the 50% threshold under the Unified Policy (some insurers apply 60% or 75% under their specific policy variants, though 50% is the regulatory baseline), the vehicle is declared a total loss. This is the moment the conversation shifts from repair to settlement.

Day 7-14: The settlement offer

The insurer calculates the payout. Starting point: the agreed insured value or the pre-accident market value, whichever the policy specifies. Deductions: the 20% depreciation under Clause 3 of the Unified Policy, the compulsory excess (deductible), and any proportional adjustment for the partial insurance period. The adjuster presents the number. The owner accepts or negotiates.

Day 14 onward: The ownership transfer

This is the critical moment. Once the owner accepts the settlement, the insurer issues paperwork that includes a Vehicle Ownership Transfer Letter, which must be signed by the owner and handed over to the insurer along with the physical keys. The Unified Policy is explicit: "If the Insured Motor Vehicle is a total loss, and the Company compensates the Insured on that basis, the salvage will be deemed property of the Company." Once the ownership transfer letter is signed, the insurer takes possession of the vehicle, the wreck moves to their designated yard, and the administrative process of cancelling the vehicle registration begins at the RTA.

The Unified Policy further states: "This Policy shall be considered terminated in case of a total loss to the Motor Vehicle, provided that its registration is deleted with a report issued by the Road and Traffic Department confirming that it is unroadworthy." The registration deletion is the closing act. And it is at exactly this moment, often a few days before the registration deletion actually processes at the RTA, that the plate’s fate is decided.

The Plate Retention Step: What It Is, When to Do It, Why Nobody Tells You

Here is the procedural fact that changes everything. The RTA offers a service called "Reserve Vehicle Plate Number," available through the Ministry of Interior portal and the RTA Dubai Drive app, that allows any plate owner to hold a plate in reserve without attaching it to a vehicle. The service exists for several reasons: owners who are between cars, owners who want to gift a plate later, investors who treat plates as standalone assets, and critically, owners whose vehicles are about to have their registration deleted following a total-loss claim.

The reservation fees are published openly on the MOI and RTA service pages and are remarkably low for the service they provide:

Dubai: AED 20 for a 3-month reservation, AED 40 for 6 months, AED 80 for 1 year, plus AED 10 Knowledge fee and AED 10 Innovation fee.

Abu Dhabi: AED 500 for 3 months, AED 1,000 for 6 months, AED 2,000 for 1 year.

Sharjah: AED 300 for 6 months, AED 500 for 1 year.

Ajman: AED 200 for 3 months, AED 400 for 6 months.

Ras Al Khaimah: AED 120 for 6 months, AED 240 for 1 year.

Fujairah: AED 30 for 3 months, AED 60 for 6 months, AED 120 for 1 year.

Umm Al Quwain: AED 60 for 6 months, AED 120 for 1 year.

For a Dubai owner, the difference between losing a plate worth AED 165,000 and retaining it costs AED 100 and takes under ten minutes through the Dubai Drive app. Read that sentence again. The most important thing you can do to protect a plate asset worth six figures in a total-loss scenario costs the price of a modest dinner. The only reason owners lose plates in this scenario is that nobody tells them the option exists.

When to trigger the reservation

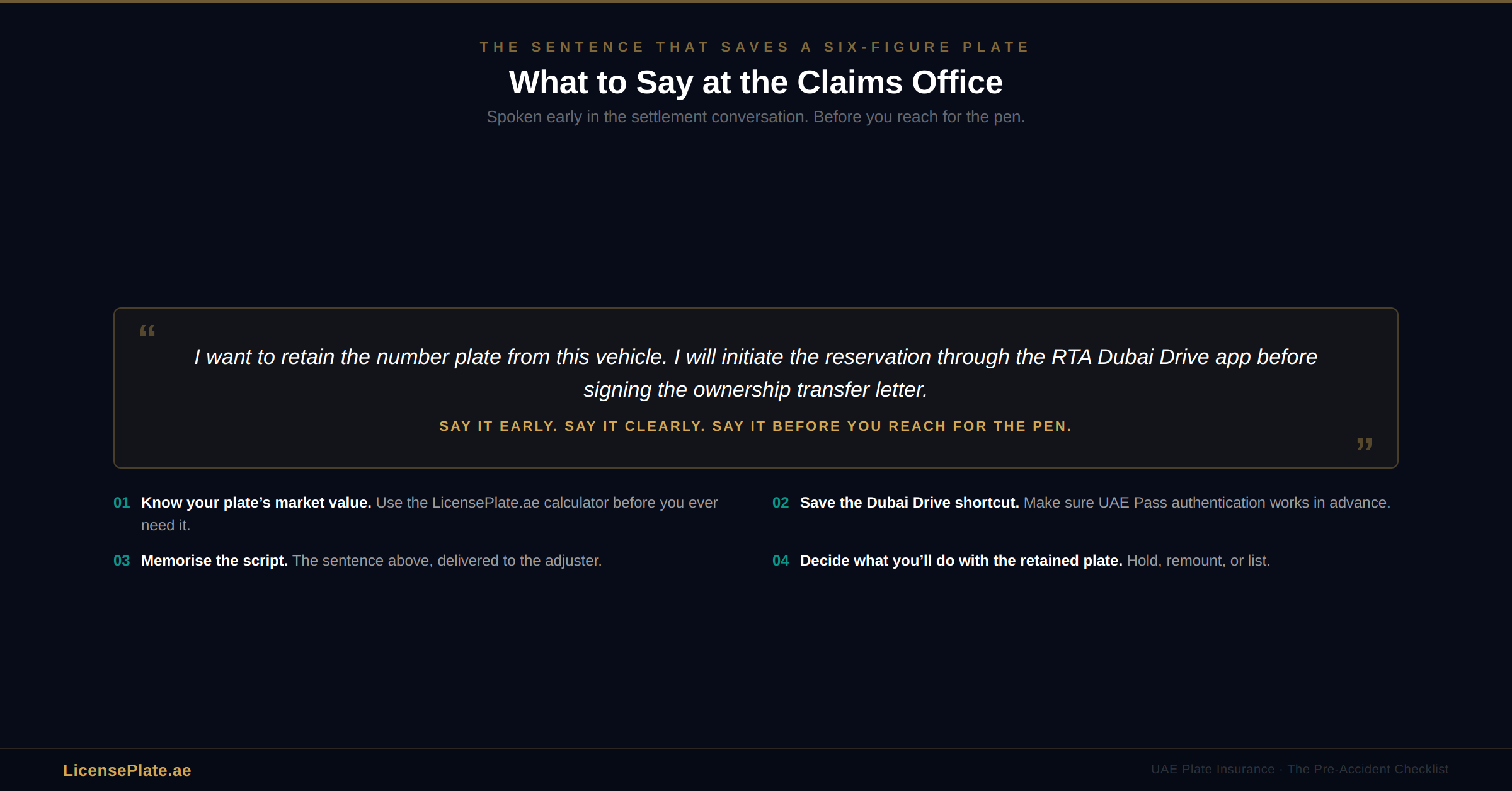

Timing is everything. The reservation must be initiated before the vehicle registration is deleted at the RTA, which means before the insurer finalises the ownership transfer process. In practice, this means the moment the adjuster tells you the car is being declared a total loss, you should pause before signing the ownership transfer letter and ask a specific question: "I want to retain the number plate. Can you confirm the administrative steps I need to take with the RTA before we finalise the vehicle transfer?"

A good adjuster will acknowledge the request immediately. Their internal process may or may not pause for your RTA step, but they have no legal or contractual reason to object. The plate is not theirs, not now and not after settlement. You can also contact the RTA directly through the Dubai Drive app, select the vehicle, navigate to Manage Vehicle Plates, and initiate the reservation for the specific plate number tied to your totalled vehicle. This creates a record that the plate should be preserved when the vehicle registration is deleted, rather than absorbed back into the RTA allocation pool.

The 72-hour window

Between the moment you accept the settlement and the moment the RTA processes the vehicle cancellation, there is usually a window of 48 to 72 hours, sometimes longer, depending on the insurer’s operational speed. This window is your retention window. Miss it by days or weeks and the plate is gone in the sense that recovering it requires navigating an RTA reinstatement process with uncertain outcomes. Hit it with even a single phone call and the plate is preserved under your traffic file indefinitely, ready to mount on your next vehicle or to list for sale on the open market through the LicensePlate.ae marketplace.

The Insurance Mismatch: Why Your Plate Is Invisible to Your Policy

Here is the structural problem that almost nobody in the UAE insurance industry talks about openly. A Dubai owner with a AED 80,000 car insured comprehensively against loss and damage and a AED 200,000 plate mounted on that car has a AED 280,000 total exposure on the road. In a total-loss scenario, the policy covers the AED 80,000. The AED 200,000 is recoverable only through the retention process described above, which is not mentioned in the policy document, not disclosed by the insurer, and not part of the standard adjuster script. The owner is effectively self-insured on AED 200,000 of asset value without knowing it.

This is not unique to Dubai or the UAE. Jurisdictions around the world with valuable private registration plates (the UK, Hong Kong, parts of mainland China) grapple with the same structural gap. The difference is that in the UAE, where plate values can easily exceed vehicle values by a factor of two, three, or ten, the gap matters more. Our Dubai vs London vs Hong Kong comparison covers the international context. Here is the UAE-specific consequence: a premium plate owner whose car is totalled discovers, for the first time, that the asset they thought was protected by their comprehensive motor insurance policy was never covered at all.

Does the premium plate affect your insurance cost?

In almost all cases, no. UAE motor insurers calculate premiums based on vehicle make, model, year, engine size, driver age, driving record, and No Claims Discount history. The plate attached to the vehicle is not a rating factor. A Mercedes S-Class with a AED 500 standard plate and an identical Mercedes S-Class with a AED 5,000,000 premium plate will typically carry the same insurance premium from the same insurer, all other factors equal. The insurer values the vehicle. The plate is invisible.

Can I insure the plate separately?

This is the question every owner eventually asks once they understand the gap. The short answer is: standalone plate insurance products do not exist in the UAE motor insurance market. The longer answer is that high-net-worth owners with multiple valuable plates sometimes include them under broader Personal Articles Policies or High-Value Asset Riders attached to their home insurance or private wealth management coverage. These are bespoke products arranged through brokers like AXA, Oman Insurance, or specialist high-net-worth advisors. They are not standard. They are not cheap. And they are worth investigating only if the total plate value sits in the mid-six-figures or higher. For the average plate owner, the retention step is the protection strategy. It is free, fast, and complete.

Five Scenarios Where the Plate-Insurance Gap Becomes Critical

The total-loss scenario is the obvious one, but it is not the only one where the gap matters. Here are five specific situations where UAE plate owners should understand the insurance treatment before it matters.

Scenario 1: Total-loss collision (the standard case)

Covered in sections above. The plate survives through the retention step initiated before the vehicle registration is deleted.

Scenario 2: Vehicle theft

When a car is stolen and not recovered within the period specified in the policy (commonly 60 to 90 days), the insurer processes it as a total loss and settles. The plate is still legally registered to the owner’s traffic file because the vehicle itself is missing from the system. The retention step is easier in this scenario because there is no physical vehicle for the insurer to take possession of. The owner should still initiate the reservation immediately after reporting the theft, because the administrative cancellation of the vehicle registration happens on the same timeline.

Scenario 3: Fire damage

Fire is covered under Chapter Two of the Unified Policy. A vehicle destroyed by fire is treated identically to a collision total loss for insurance purposes, meaning the same retention window applies. The plate, if physically melted beyond readability, can be reissued by the RTA under the same number because the owner retains ownership of the registration. Our Dubai Fees Guide documents the replacement costs for physically damaged plates.

Scenario 4: Flood damage

The April 2024 and April 2025 storms that hit the UAE put hundreds of vehicles through the total-loss process. Flood damage is covered under the Unified Policy under loss and damage provisions. The plate survives through the same retention step. Owners whose cars were written off during the 2024 storms and who didn’t initiate the retention lost premium plates in ways the insurance industry quietly acknowledged afterward but never publicised. This is the single most-preventable category of plate loss in the UAE, and most of the lost plates were on cars worth less than the plates themselves.

Scenario 5: Owner-initiated write-off (economic total loss)

A car that is technically repairable but economically not worth repairing (the repair cost is below the 50% threshold but still exceeds what the owner wants to spend) can be processed as a voluntary total loss by agreement with the insurer. This is rarer but happens. The same retention logic applies: initiate the plate reservation before signing the ownership transfer letter, and the plate is preserved. Our guide to what happens to your plate when you sell your car covers the related scenario where a car is sold rather than written off, which uses a similar retention workflow but runs through a different RTA service.

The Owner’s Pre-Accident Checklist

The time to understand this is before the accident, not after. If you are a current plate owner with a plate worth anything meaningful, here is what you should do this week.

1. Know your plate’s market value. Use the LicensePlate.ae plate calculator to get an honest range for your specific code, digit count, and pattern. Save the valuation screenshot somewhere your spouse or executor can find it. If your plate is worth less than AED 10,000, the retention step is still worth doing but the urgency is lower. If your plate is worth more than AED 50,000, the retention step is the most important five-minute task in your asset protection plan.

2. Save the RTA Dubai Drive app shortcut on your phone. The retention step is initiated through the app under Vehicle Licensing then Manage Vehicle Plates. Make sure you can log in with UAE Pass before you need to. In an emergency, you do not want to be troubleshooting your UAE Pass authentication from a claims office.

3. Know the script. If your car is ever declared a total loss, the sentence you need to say to the adjuster is this: "I want to retain the number plate from this vehicle. I will initiate the reservation through the RTA Dubai Drive app before signing the ownership transfer letter." This sentence, spoken early in the settlement conversation, protects the plate completely.

4. Document the plate in your insurance records. When you renew your motor insurance annually, note the plate’s current market value in your own records. This is not a claim document, but it is your own written evidence that you treated the plate as a separate asset. If the issue ever goes to mediation or dispute, this documentation supports your position.

5. Decide, in advance, what you would do with the retained plate. After a total-loss claim, the owner typically has no vehicle for several weeks while they arrange a replacement. The retained plate sits in the traffic file at essentially zero cost, as documented in our Cost of Ownership guide. You can mount it on the new car when it arrives, hold it for a future purchase, or list it for sale immediately if you’d rather crystallise the value. Knowing your preference in advance removes decision friction at the worst possible time.

The Misconceptions Most Owners Carry

"My comprehensive policy covers everything on the car, including the plate." It does not. The policy covers the vehicle and its accessories. The plate is neither. Read the policy document, search for the word "plate," and you will find nothing. The Unified Motor Vehicle Insurance Policy published in the CBUAE Rulebook confirms this by omission.

"The insurer will handle the plate as part of the claim, I don’t need to do anything." The insurer will handle the salvage. The plate is not part of the salvage. The insurer has no legal obligation or incentive to preserve a plate that is not their asset, and the adjuster processing your claim is trained to complete the vehicle settlement, not the plate retention. If you don’t raise the issue, it does not get raised.

"I paid extra for a premium plate, so my insurance must have factored it in." It did not. Your premium is based on the vehicle, not the plate. This is verifiable: call your insurer, ask them to quote you on an identical car with a standard plate and then on the same car with your actual plate. The quotes will be identical in almost every case.

"If I don’t retain the plate, I can just buy it back later from whoever gets it." Not really. Plates released back to the RTA pool after a vehicle cancellation enter a different administrative track than plates sold at auction. The specific combination you lost may or may not reappear, and if it does, it is years later through channels you cannot predict. A plate you could have retained for AED 100 cannot be repurchased for any predictable amount.

"This is an edge case that affects very few people." It affects every UAE plate owner who ever has a total-loss claim, which in a city where plate values now regularly exceed vehicle values and traffic density produces thousands of total-loss claims per year, is not an edge case. It is a structural gap nobody has written a complete guide to closing.

Frequently Asked Questions

Q: What happens to my number plate if my car is declared a total loss in the UAE?

The plate does not transfer to the insurer with the vehicle. It remains tied to your traffic file until the vehicle registration is deleted at the RTA. If you initiate a plate reservation through the Dubai Drive app before that deletion happens, the plate is preserved under your name indefinitely. If you do not, the plate is typically released back into the RTA allocation pool when the vehicle cancellation processes.

Q: Does UAE car insurance cover the value of a premium number plate?

No. The Unified Motor Vehicle Insurance Policy (issued under CBUAE Decision No. 25 of 2016) insures the motor vehicle and its accessories. The plate is treated as a registration artefact linked to the vehicle, not as a separately insured asset. This means a comprehensive policy on a AED 80,000 car with a AED 500,000 plate mounted on it still covers only the AED 80,000 vehicle in a total-loss scenario.

Q: How do I retain my number plate after a total-loss accident?

Log into the RTA Dubai Drive app with UAE Pass, go to Vehicle Licensing, then Manage Vehicle Plates, select the plate you want to retain, and initiate the Reserve Vehicle Plate Number service. Dubai fees: AED 20 for 3 months, AED 40 for 6 months, AED 80 for 1 year, plus knowledge and innovation fees. Initiate this step before signing the vehicle ownership transfer letter to the insurer.

Q: What is the 50% threshold for a total-loss declaration in the UAE?

Under Chapter Two of the Unified Motor Vehicle Insurance Policy, a motor vehicle is considered a total loss when the cost of repair exceeds 50% of the motor vehicle value before the accident. The insurer then compensates based on the insured value agreed in the policy, subject to a 20% depreciation deduction and proportional time adjustment for the partial insurance period.

Q: Does a premium plate affect my insurance premium in Dubai?

In almost all cases, no. UAE motor insurers calculate premiums based on vehicle make, model, year, engine size, driver age, driving record, and No Claims Discount history. The plate attached to the vehicle is not a standard rating factor. A Mercedes with a standard plate and an identical Mercedes with a multi-million dirham plate will typically carry the same premium.

Q: Can I insure a number plate separately from the car in the UAE?

Standalone plate insurance products do not exist in the UAE motor insurance market. High-net-worth owners sometimes include premium plates under Personal Articles Policies or High-Value Asset Riders arranged through specialist brokers. These are bespoke products worth investigating only for plate portfolios in the mid-six-figures or higher. For most owners, the RTA retention step is the complete protection strategy.

Q: What is the cost of reserving a plate in Dubai?

AED 20 for a 3-month reservation, AED 40 for 6 months, and AED 80 for a 1-year reservation, plus AED 10 Knowledge fee and AED 10 Innovation fee. Total cost for a 1-year reservation: AED 100. These fees are published on the Ministry of Interior and RTA service pages and apply to any owner who wants to hold a plate without mounting it on a vehicle.

Q: How long do I have to retain my plate after a total-loss claim?

The retention must be initiated before the vehicle registration is deleted at the RTA, which typically happens 48 to 72 hours after the insurer processes the ownership transfer. In practice, the window is from the moment the adjuster tells you the car is a total loss to the moment the RTA processes the vehicle cancellation. Act immediately when you learn the car is being written off.

Q: What is the Unified Motor Vehicle Insurance Policy in the UAE?

The Unified Motor Vehicle Insurance Policy Against Loss and Damage, issued under Insurance Authority Board of Directors’ Decision No. 25 of 2016, is the binding template for comprehensive motor insurance in the UAE. It is published in the CBUAE Rulebook and sets the baseline terms every UAE motor insurer must follow. The policy governs total-loss thresholds, depreciation, salvage, and claim procedures.

Q: If my plate is physically damaged in the accident but I retain ownership, can I get a replacement plate with the same number?

Yes. The RTA Manage Vehicle Plates service allows replacement of lost or damaged plates. Because the owner retains legal ownership of the plate number itself, the replacement physical plate carries the same number. Replacement fees are documented in our Dubai Fees Guide. This works only if the retention step was completed before the vehicle registration was deleted.

A Final Thought, Returning to Sheikh Zayed Road

The resident from the opening paragraph, the one whose Mercedes ended up spun into the central barrier on a Tuesday morning in March, does not exist. The details are synthetic, assembled from common claim profiles and real UAE insurance clauses. But versions of that resident exist everywhere in the UAE insurance system. The adjusters have seen them. The brokers have watched the conversation from the other side of the desk. The plate owner arrives at the claims office thinking the hard part is negotiating the settlement number. They leave having lost something they didn’t realise was at stake.

The UAE motor insurance system is competent, regulated, and operationally efficient. The Unified Motor Vehicle Insurance Policy published by the CBUAE is a substantive document that protects vehicle owners in real ways. What it does not do, and was never designed to do, is protect plate owners from a gap the insurance industry inherited from a regulatory framework that predates the transformation of plates into serious asset classes. The gap is not the insurer’s fault. It is not the policy’s fault. It exists because number plates crossed a value threshold that the insurance framework was never updated to address, and nobody along the way added the plate-retention conversation to the standard claims script.

The good news is that closing the gap requires no regulatory reform, no new product, and no negotiation with the insurer. It requires one sentence at the claims office and one service request through the Dubai Drive app. The readers of this article who remember nothing else should remember the sentence: "I want to retain the number plate from this vehicle. I will initiate the reservation through the RTA Dubai Drive app before signing the ownership transfer letter." Say it early. Say it clearly. Say it before you reach for the pen.

Comments (1)

Please log in to leave a comment

Log In

Car 1

منذ شهر

Car1.ae is the ultimate platform for car buyers in Dubai. Whether you're ready to <a href="https://car1.ae/sell-my-car-online">Sell Your Car</a> or just exploring your options, Car1.ae makes it effortless. Simply list your vehicle, receive an instant quote, and get paid on the spot. Selling your car has never been faster, easier, or more convenient than with Car1.ae!

Delete Comment?

Are you sure you want to delete this comment? This action cannot be undone.

Delete Article?

Are you sure you want to delete this article? This will also delete all comments. This action cannot be undone.