Plate-Backed Lending in the UAE: The B2B Credit Market Built on Premium Plate Collateral

April 16, 2026

Dubai

LicensePlate.ae Team

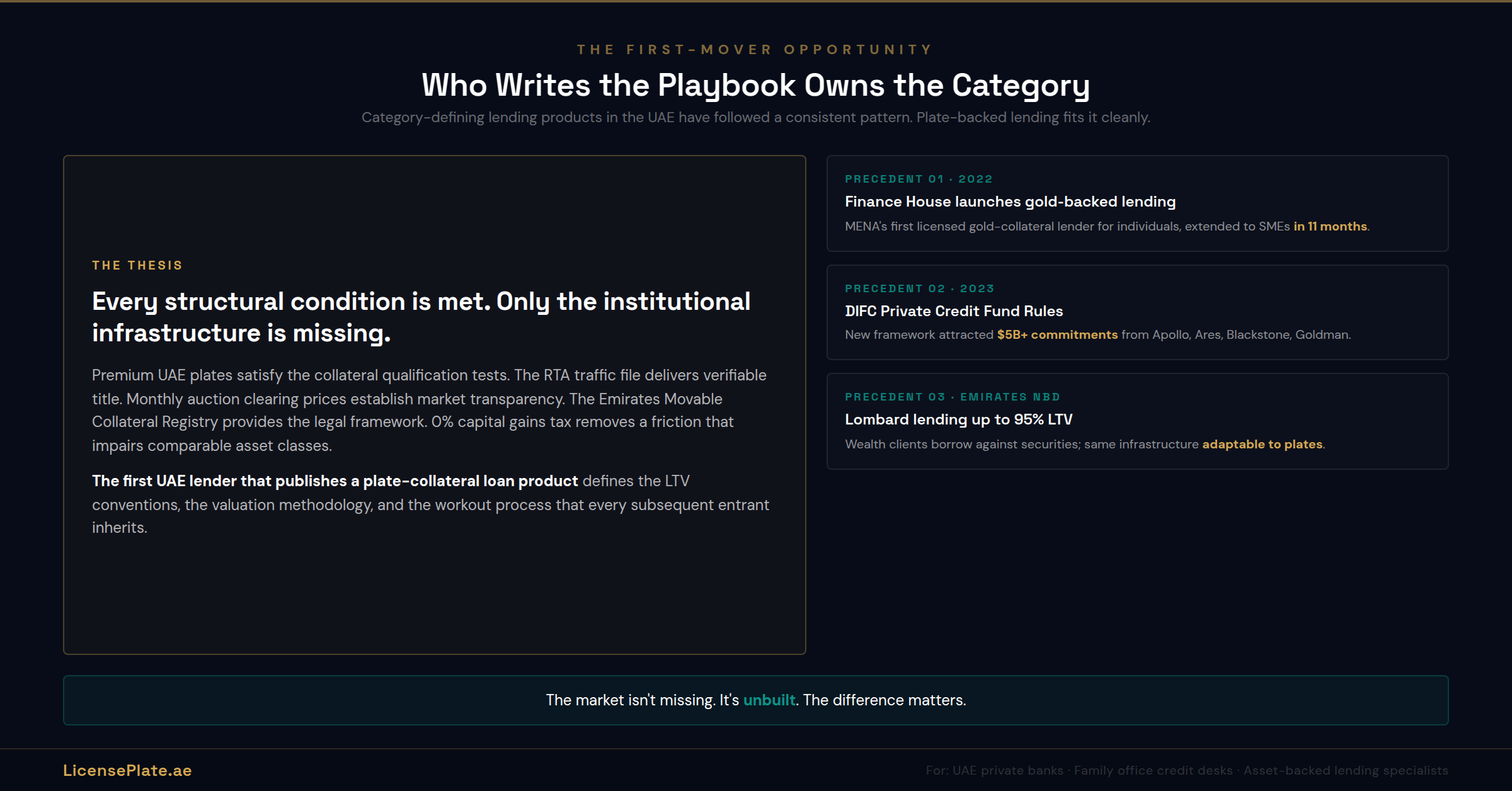

In January 2022, a UAE-based investment firm called Finance House announced it had become the MENA region’s first licensed lender to offer gold-backed loans to individuals. Eleven months later, the company extended the product to SME owners, pitching it in language that stood out: the loan is “accessible to any type of customer, regardless of credit history, business plan, or development strategy,” so long as the borrower can provide suitable gold as collateral and is registered in the UAE. The structural insight behind the product was simple. Gold is a verifiable asset with a transparent market price, a liquid global secondary market, and a fixed-weight standard that makes valuation a matter of a scale and a price feed. Everything else that determines whether a lender will extend credit, including the borrower’s income history or business plan, becomes secondary when the collateral itself carries enough certainty.

The question this article asks is whether UAE premium number plates could, in principle, occupy the same position. Plates have an observable market price with multi-year auction history. They have fixed supply on early codes. They transfer through a central government registry (the RTA traffic file) that verifies ownership with a single database lookup. At the top of the market, they trade in units of AED 3 million, AED 10 million, AED 35 million, AED 55 million, large enough to justify the origination costs of a private credit facility and to move materially on the balance sheet of a UAE high-net-worth client. A premium plate portfolio, for a family office with AED 100 million in UAE plate holdings, looks on the surface like an ideal candidate for Lombard-style asset-backed finance.

It isn’t, yet. And the reason is not that banks don’t want to lend against plates. It is that a specific provision of UAE federal law, combined with the plate-registry architecture at the RTA, creates a structural constraint that neither the borrower nor the lender can solve alone. Understanding the constraint is the first step to understanding the three pathways through which plate-backed lending can emerge in the UAE anyway. This article maps all three. It is written for the UAE private banker, family office credit officer, and asset-backed lending desk evaluating whether the UAE plate market is a category worth building a product against, or a category that will stay bespoke for the foreseeable future.

What UAE Lenders Already Accept as Collateral

Before examining whether plates can serve as collateral, the baseline: what UAE banks currently accept, and on what terms. The landscape is more developed than most outside observers assume, but also more narrowly defined.

The Mainstream: Securities-Backed Lending

Every major UAE private bank offers Lombard-style lending against marketable securities. Emirates NBD’s Lending Against Secured Assets facility extends credit up to 95% of the pledged asset value against shares, equities, and fixed deposits, with a Sharia-compliant Tawarruq version available for Islamic banking clients. ADCB’s Private Banking tailored lending offers similar structures: facilities held against shares listed on the Abu Dhabi Exchange and Dubai Financial Market, against fixed deposits and walaka deposits, against international securities portfolios, and against universal life insurance policies issued by A-rated carriers. Standard Chartered UAE’s Wealth Lending accepts fixed deposits, mutual funds, bonds, insurance policies, and structured products as collateral, with typical loan-to-value ratios on mutual funds around 70%. These are the off-the-shelf products. Every HNW client of a UAE private bank has access to them.

The Specialist Brokers: Complex and Cross-Border Facilities

A tier above the bank products, specialist finance brokers structure bespoke lending against assets that retail banks cannot underwrite. GSB Capital, a DIFC-based private finance firm authorised by the UK Financial Conduct Authority, arranges facilities typically starting at GBP 1 million, working with a selective network of private banks and specialist lenders on cross-border transactions. Enness Global in Dubai brokers securities-backed finance including Lombard loans against listed equities, pre-IPO loans, unlisted stock loans, and loans against single lines of stock, with terms typically 12 to 24 months. These specialists operate in the space between mainstream banking and private-deal structuring. They are the firms that would write the first plate-backed facility when conditions allow.

The Non-Traditional Precedents: Gold, Artwork, Vehicles

Beyond securities, the UAE has functioning precedents for lending against physical luxury collateral. The Finance House gold loan programme is the cleanest example: a regulated UAE lender extending credit against a physical commodity with a transparent global price. Artwork is legally pledgeable under UAE law. Analysis by M&Co Legal confirms that artwork qualifies as tangible movable property under Federal Decree Law No. 4 of 2020 on Securing Rights in Movable Property, and that a pledge over artwork can be registered on the Emirates Movable Collateral Registry to create a priority interest enforceable against third parties. Vehicles, strictly speaking, cannot, because they fall under a special register excluded from the EIRC framework. This is the exact same exclusion that applies to plates, and it is the central technical constraint this article has to address.

The Legal Architecture: Why Plates Are Not a Standard EIRC Pledge

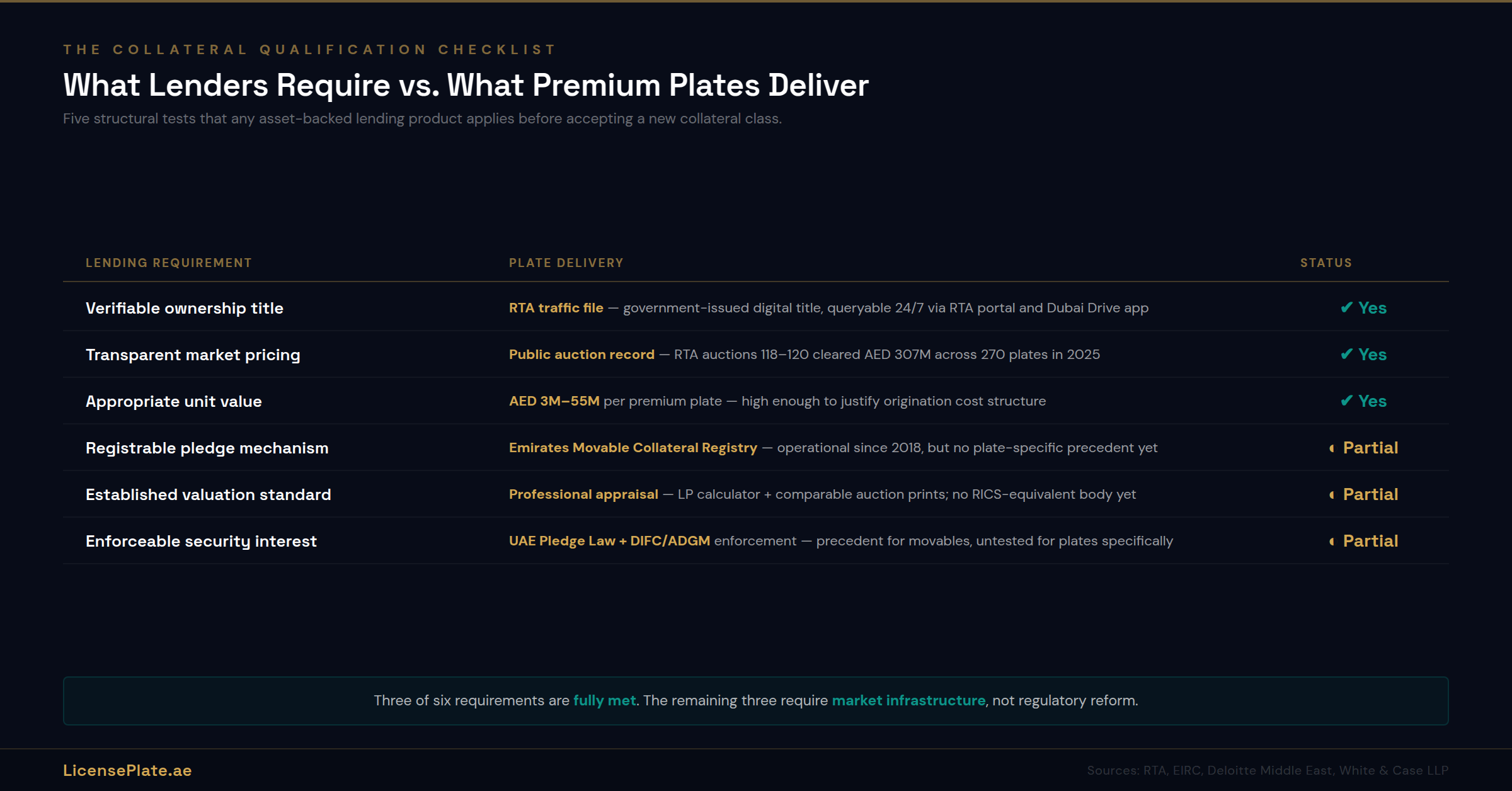

UAE secured lending against movable property operates under two primary frameworks. The federal onshore framework is governed by Federal Decree Law No. 4 of 2020 on Securing Rights in Movable Property, which replaced the earlier 2016 Pledge Law, with executive regulations set out in Cabinet Decision No. 29 of 2021. The DIFC and ADGM financial free zones operate their own common-law security frameworks, and UAE federal movable property law does not apply within those zones.

Under the federal framework, the Emirates Movable Collateral Registry, now operated by the Emirates Integrated Registries Company under the Emirates Development Bank, serves as the public registry where security interests over movable property are recorded. Registration on the EIRC is what makes a pledge enforceable against third parties. It is the equivalent, for movable property, of the land mortgage registry that governs real estate secured lending. The list of assets that can be registered is broad: equipment, accounts receivable, bank account deposits, commercial papers, inventory, raw materials, agricultural products, goodwill, trade names, intellectual property. Under Article 3 of the law, tangible movable property including artwork, collectibles, and vehicles is explicitly in scope.

The Special Register Exclusion

The exclusion that matters for plates is specified in the same body of law. As analysed by Lexology, the Movable Security Law does not apply to movable assets in relation to which interest is recorded in a special register under applicable UAE laws. The examples the law and subsequent legal commentary name explicitly are motor vehicles, ships, and aircraft. These assets have their own dedicated registries (the RTA vehicle registry in Dubai, the ICP vehicle registry federally, the federal ships registry, the GCAA aircraft registry). Pledges against those assets operate under the specific framework of those registries, not under the EIRC.

Number plates fall into exactly this category. The plate is recorded in the RTA traffic file. The RTA traffic file is a special register. The plate’s ownership transfers through the RTA system, not through the EIRC system. The consequence is that a lender who wanted to take a registered pledge over a premium plate cannot walk into the EIRC and file a notice. The EIRC does not recognise the plate as a registrable asset under the Movable Security Law framework.

What This Does Not Mean

The exclusion is not a prohibition. UAE law does not forbid lending against plates. It merely routes any such transaction outside the standard EIRC pledge mechanism into three alternative pathways, each with its own legal basis and its own operational constraints. The critical distinction is between: first, taking a direct registered pledge over the plate itself (currently not available through the standard framework), and second, structuring the transaction so that the plate’s economic value serves as the credit support even though the formal security interest attaches to a different legal object.

The Three Pathways Through Which Plate-Backed Lending Can Emerge

Given the constraint, the interesting question is how plate-backed lending would actually work if a UAE bank or specialist lender wanted to offer it. The three pathways below are each legally viable today. They differ in structural complexity, in which party bears the enforcement risk, and in how close they come to a true pledge-over-plate transaction. A lender considering this market should evaluate all three and choose the one that fits their operational capabilities.

Pathway One: The Bailment and Possession Model

Under Article 10 of the Movable Security Law, a security interest can be made enforceable against third parties by three methods: registration with the EIRC, delivery of possession of the collateral to the secured creditor, or control of the collateral by the secured creditor. Registration is the standard mechanism. Possession is the alternative.

In a plate context, possession is structurally awkward because a plate is a government-issued identification, not a physical object the way a watch or a piece of art is. But the concept has a workable analogue: the RTA allows a plate to be transferred to an account held by the lender (or by a nominee company controlled by the lender) for the duration of the loan, and transferred back to the borrower on full repayment. The lender holds the plate in its own traffic file during the loan term. Default triggers nothing more than the lender retaining the plate it already holds, with the option to sell it through an RTA transfer to a third-party buyer.

The mechanism is legally clean: the plate is in the lender’s name, full stop. There is no security interest to enforce against third parties because the lender is the recorded owner. The borrower holds a contractual right to receive the plate back on repayment, which functions economically as a repurchase option. Structurally this is closer to a repo transaction than to a secured loan, and lenders familiar with repo structures can underwrite it without novel legal analysis. The costs are the two RTA transfer fees at loan origination and loan maturity, which are trivial at the transaction sizes involved (a one-time AED 120 to AED 350 per transfer).

The trade-off is regulatory. A lender holding AED 50 million of plates on its own traffic file is, in regulatory terms, holding luxury goods on its balance sheet. UAE Central Bank prudential requirements for banks treat such holdings differently from securities or cash, and may require specific regulatory approval depending on the lender’s licence category. Specialist lenders operating outside the Central Bank’s direct supervision (DIFC-regulated finance firms, ADGM-regulated firms) face lower regulatory friction on this structure. Onshore UAE banks face higher friction.

Pathway Two: The DIFC or ADGM Holding Company Structure

The DIFC and ADGM financial free zones operate under English-law-style security frameworks that are independent of the federal Movable Security Law. As analysed by White & Case, creditors can take registrable security over the shares of ADGM and DIFC entities under those zones’ own rules, and these structures have been increasingly adopted in UAE private credit transactions as alternatives to the traditional “friendly jurisdictions” of Cayman, BVI, Jersey, and Luxembourg. Chambers and Partners confirms that foreign lenders can hold security in the DIFC and that DIFC and ADGM both maintain real property registries distinct from the onshore framework.

The structural move is to form a DIFC or ADGM special purpose vehicle that holds the plate (through an onshore nominee arrangement, since the plate itself has to remain on an RTA traffic file, but the beneficial ownership of the plate sits with the SPV). The lender then takes a registered share pledge over the SPV under DIFC or ADGM law. Default on the loan triggers the lender’s right to enforce the share pledge, take control of the SPV, and liquidate the plate through the SPV’s onshore nominee.

This structure is more legally complex, requires SPV formation and ongoing maintenance costs, and involves a longer documentation timeline. But it delivers two things the bailment model does not: first, the lender does not hold the plate on its own balance sheet, which solves the regulatory treatment issue; second, the security interest is a proper registered pledge under DIFC or ADGM law, which provides cleaner enforcement mechanics in a default scenario, particularly if the default involves a contested claim by the borrower.

The economics work at scale. For a single AED 2 million plate, the SPV costs (formation, ongoing maintenance, legal documentation) are prohibitive relative to the loan size. For a portfolio facility of AED 50 million collateralised by multiple plates, the SPV costs amortise cleanly. The natural borrower for a Pathway Two transaction is a family office or corporate plate portfolio holder rather than an individual with a single plate. Our women in the Dubai plate market analysis documents the growing cohort of female plate-portfolio holders in the UAE, a particularly relevant demographic for this structure given the ownership-transparency advantages of SPV holdings. The Binghatti case study on corporate plate acquisition documents another likely borrower profile: developers and corporate entities holding premium plates as brand assets, where SPV-based financing would allow liquidity extraction without disrupting the corporate ownership record.

Pathway Three: The Dealer-Guarantor Indirect Model

The third pathway avoids pledging the plate at all. Instead, the lender extends credit to a plate-market dealer (not the ultimate borrower) who uses the loan proceeds to acquire plates and then forward-sells them on commercial terms. The dealer carries the commercial risk, the plates sit on the dealer’s inventory, and the lender takes security against the dealer’s balance sheet rather than against any specific plate.

This is closest to a working-capital line of credit for a plate trading business, secured by the dealer’s general assets, trade receivables, and potentially by inventory pledges over plates held as stock (where the plates are held in the dealer’s traffic file and can be structurally addressed through the bailment logic of Pathway One). It does not give individual plate owners access to credit against their own plates, but it does channel capital into the plate market at the wholesale level, which increases market depth and liquidity for the retail buyers and sellers downstream. Several UAE bank relationship managers have informally told us that they already extend general working-capital lines to plate dealers under this model, without categorising the facility as “plate-backed” because the security package is the standard corporate one.

The value of naming Pathway Three explicitly is that it is the pathway most likely to expand first. It requires no new product development by the lender (it is a corporate-lending product with a specific industry profile), no novel legal structuring, and no regulatory approval beyond the lender’s existing commercial lending mandate. If UAE private credit is going to grow into plate exposure, it will do so through this channel first. Pathways One and Two follow later, when the market has established enough transaction depth for individual-plate lending to become operationally efficient.

Valuation, Loan-to-Value, and the Underwriting Parameters a Lender Would Apply

Any plate-backed facility requires a defensible valuation methodology. The lender needs to know, at origination and throughout the loan term, what the collateral is worth under a conservative assumption set. The UAE plate market provides stronger valuation data than most non-traditional luxury asset classes, but it is still meaningfully less liquid and less transparent than listed equities or gold.

The Valuation Hierarchy

For premium UAE plates, three valuation sources of descending reliability are available. The most reliable is a named recent auction clearance for a substantially identical plate: the same digit count, same code family, same pattern type. These are documented in our Dubai plate price check article and in our all-time records article. Examples from 2024–2026 include BB12 at AED 9.66M (December 2025, 120th RTA auction), AA25 at AED 8.04M (same event), BB88 at AED 14M (September 2025), and AA707 at AED 3.31M (April 2025). A lender underwriting a three-digit AA code plate has multiple recent comparable clearances as a valuation anchor.

The second-tier valuation source is the LicensePlate.ae plate calculator, which takes a specific code and digit pattern and returns an estimated value band based on market data. This is comparable to an automated valuation model in real estate: useful as a second opinion, not a standalone underwriting basis. The third-tier source is secondary market asking prices visible on the public marketplaces, which set a ceiling rather than a clearing price and have to be discounted for the typical asking-to-sale gap.

Suggested Loan-to-Value Ratios

A prudent UAE lender pricing a plate-backed facility would apply significantly more conservative LTV ratios than the 70–95% range available on listed securities. Plates are less liquid, have wider bid-ask spreads, and can take weeks to months to sell at a predictable price. Based on our analysis of the secondary market velocity documented in our RTA auction versus secondary market analysis, the following LTV structure reflects what a conservative lender would underwrite in 2026:

Trophy tier (single-digit, AED 50M+): 50–60% LTV. Extremely limited buyer pool, very long time-to-sell (months to over a year), concentration risk means distressed sale would likely clear well below recent comparable. Only the most experienced specialist lenders should underwrite this tier at all.

Ultra-premium tier (two-digit on double-letter codes, AED 7–40M): 55–65% LTV. Market depth is improving (multiple comparable clearances per year) but still thin enough that distressed sale timing matters materially. The Most Noble Numbers auction series provides the clearest repeated pricing evidence for this tier.

Premium tier (three-digit double-letter or two-digit single-letter, AED 200K–6M): 60–70% LTV. The sweet spot for plate-backed lending. Multiple comparable auction clearances per year, multiple active secondary-market listings, predictable time-to-sell of 4–12 weeks for well-priced plates. A lender building a plate-backed product should focus here.

Mid-market tier (four-digit plates, AED 95K–250K): 50–60% LTV, and only for plates on early codes (A through D) where the supply constraint supports valuation. Four-digit plates on mid-to-late codes should not be underwritten for plate-backed lending because of their exposure to RTA fixed-price supply releases, as documented in our coverage of the May 2025 AED 95,000 release on L and M codes.

Entry tier (five-digit plates): Not viable. The per-unit value is too low to amortise origination costs, and the asset class does not appreciate. A lender would not write a plate-backed facility against five-digit inventory.

Mark-to-Market Discipline and Margin Calls

Every plate-backed facility requires ongoing valuation monitoring equivalent to the mark-to-market discipline applied to securities-backed facilities. In Standard Chartered UAE’s Wealth Lending disclosures, the bank explicitly reserves the right to adjust LTV ratios within a short period of time based on market conditions and to trigger margin calls requiring the borrower to post additional collateral or repay part of the outstanding facility. Plate valuations are less volatile than equities but are not constant, and a major auction clearance well below or above expectations could shift the valuation of comparable plates by 15–30% in a single event. A plate-backed facility should include quarterly valuation review clauses at minimum, with ad-hoc revaluation triggers tied to major auction events.

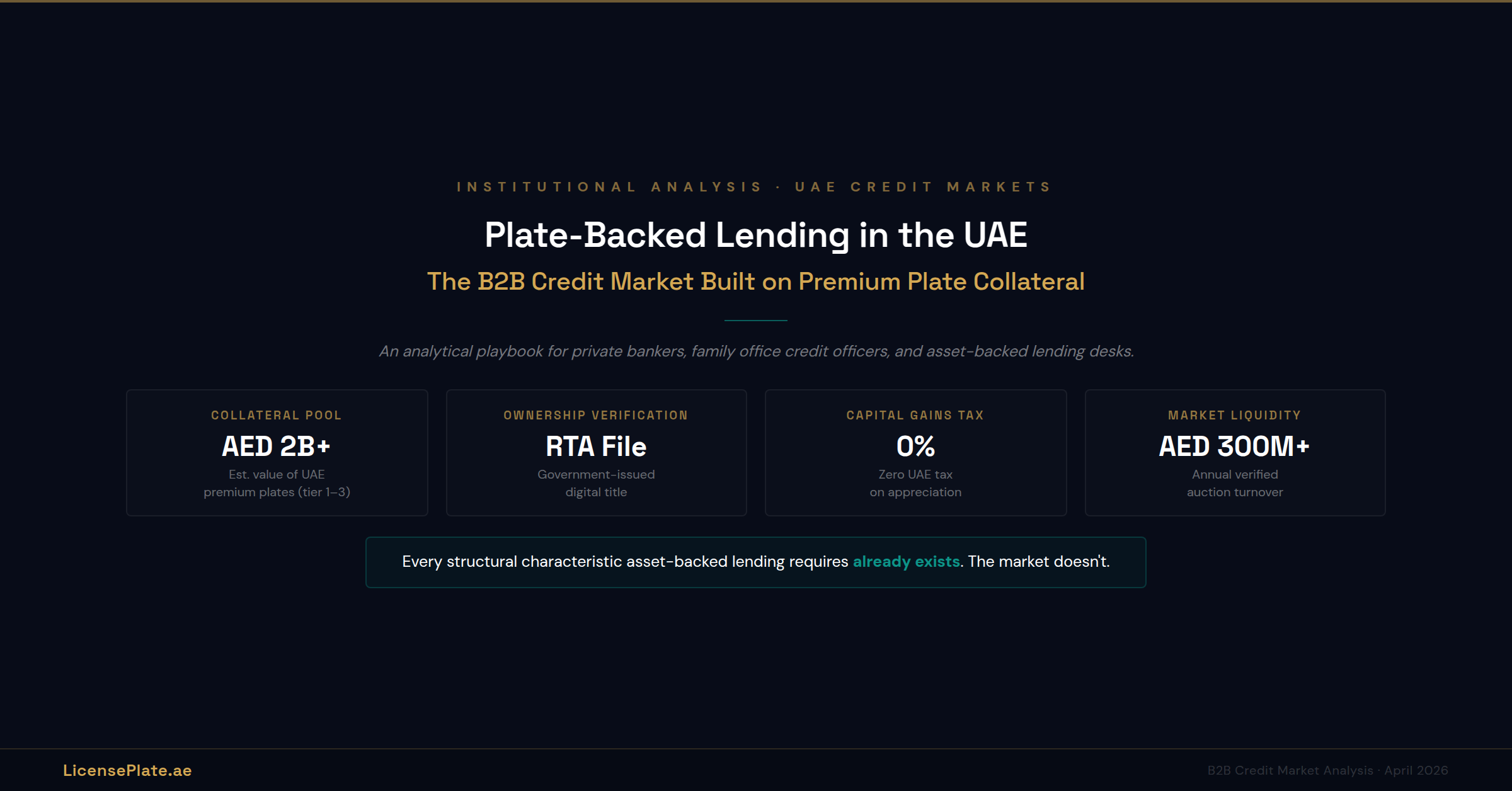

The Market Size Question: How Big Could Plate-Backed Lending Get?

Sizing a market that functionally does not exist yet requires some assumption. The publicly verifiable data provides a floor. The three consecutive RTA auctions in 2025 cleared a combined AED 307 million from approximately 270 plates. The Most Noble Numbers 2025 event cleared an additional AED 75.9 million from RTA plates alone, across five DD-series lots. Published auction totals for 2025 exceed AED 400 million. This is the primary-market issuance volume, equivalent to IPO volume in a public equities market. Our RTA auction calendar tracks every scheduled event and historic result, providing the cadence data any lender would need to model plate-market liquidity across a facility tenor.

The secondary market is materially larger. LicensePlate.ae, xPlate, Dubizzle, Numbers.ae, and smaller platforms collectively list tens of thousands of active plates. Conservative estimate of the total UAE plate market capitalisation, counting all plates across all emirates on all codes, is in the range of AED 20–40 billion at 2026 prices, with perhaps AED 5–10 billion concentrated in the premium and ultra-premium tiers where plate-backed lending would be most viable.

If even 5% of the premium-tier inventory eventually becomes the collateral base for plate-backed facilities, the addressable market is AED 250–500 million in outstanding credit. At a blended 60% LTV and typical facility tenors of 12–24 months, that translates to an annual origination volume of AED 125–250 million. This is not a large market by UAE banking standards (the UAE banking system had consolidated assets exceeding AED 4 trillion in 2024), but it is a defensible specialist niche for one or two dedicated lenders, comparable in scale to the art-finance niches operated by Sotheby’s Financial Services or Athena Art Finance in major global markets.

The growth trajectory is what matters more than the current size. The UAE plate market has shown expanding depth, documented in our analysis of the 20% returns claim and in our comparison of plates against real estate and gold as alternative assets. The same factors that are driving the plate market’s maturation (institutional ownership, cross-border buyer interest, higher absolute values, growing auction totals) are the factors that create the conditions under which plate-backed lending becomes viable. A lender moving first into this category today is underwriting not the current market but the market three to five years from now.

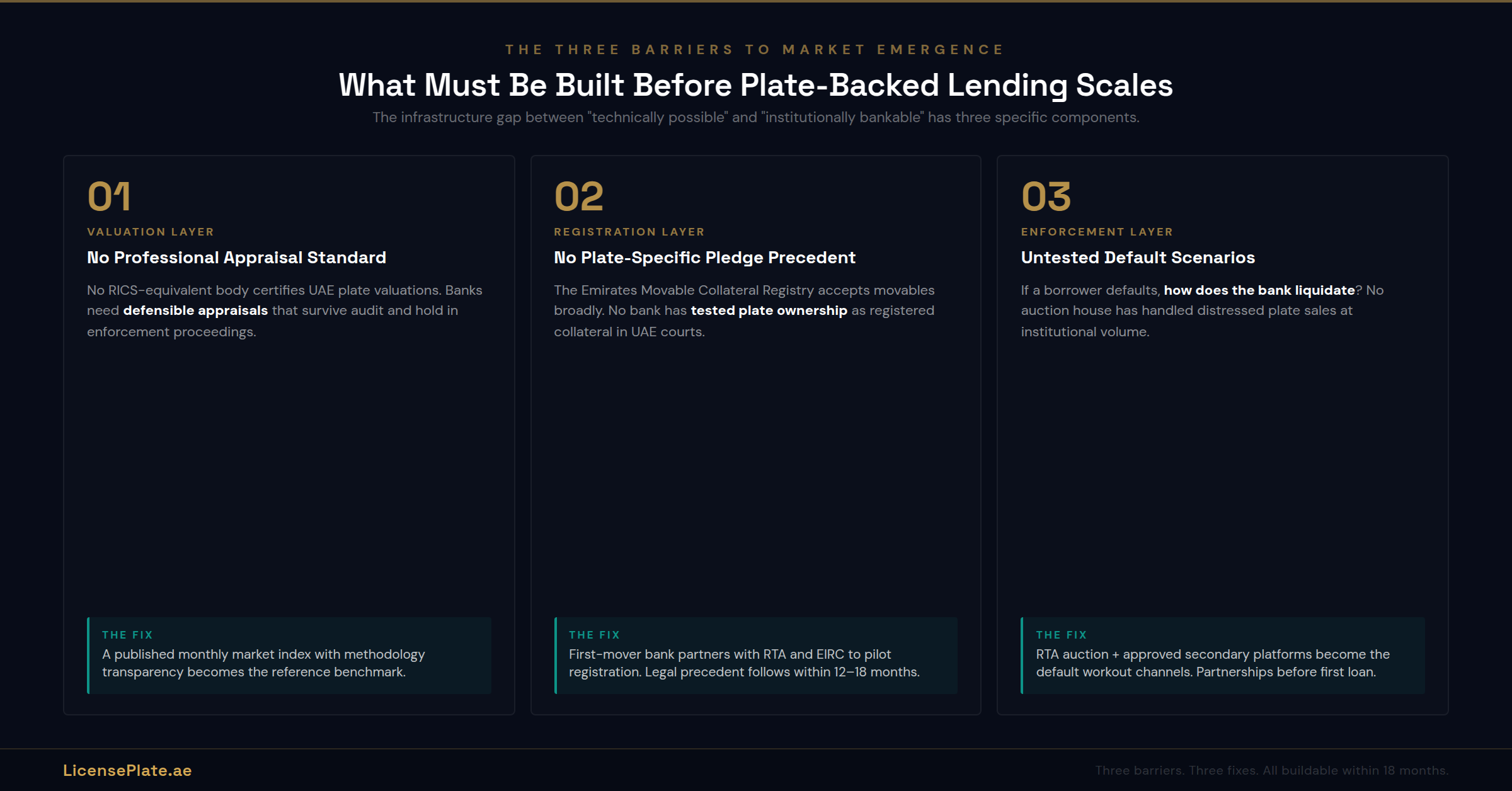

What Has to Happen for Plate-Backed Lending to Become a Category

The market moves from zero to category when three specific conditions are met. All three are achievable within 24–36 months under the right execution. None is structurally blocked.

Condition One: A Reference Valuation Source Emerges

No lender will underwrite plate-backed facilities at scale without an authoritative valuation reference that they can cite in credit memos, use in revaluation workflows, and defend in regulatory inspections. Currently, no such reference exists. The LicensePlate.ae plate calculator and the published auction records in our Dubai plate price check article are the closest approximations in the market, but neither is yet cited in formal lender documentation. The emergence of a monthly or quarterly UAE Plate Market Index, published with transparent methodology, is the single most important precondition for institutional plate-backed lending. This is the niche that LicensePlate.ae is structurally best positioned to fill.

Condition Two: A First Mover Writes the Precedent Deal

Markets like this move on precedent. The first publicly reported plate-backed facility in the UAE, structured by a named lender against a named borrower with disclosed terms, will be covered by the UAE business press and will create the reference transaction that subsequent deals refer to. Until that first deal is documented, every prospective lender is evaluating the category as a pure greenfield, which is a much harder credit committee decision than evaluating against a precedent. The likely first mover is a specialist DIFC-based private credit firm using the Pathway Two structure on a portfolio facility of AED 20–50 million against a family-office-held plate portfolio. It has not happened yet. It is not far off.

Condition Three: Regulatory Guidance from the UAE Central Bank

The UAE Central Bank has not issued specific guidance on the treatment of plate collateral for onshore licensed banks. Until it does, onshore banks will remain reluctant to build products in this space because the prudential capital treatment is uncertain. DIFC and ADGM regulated firms can operate under their own regulators’ frameworks and do not need this guidance to the same degree. But the expansion from a handful of specialist-lender transactions to a mainstream onshore-bank product requires regulatory clarity on how plate collateral is risk-weighted and how plate holdings on a bank’s balance sheet are treated. The Central Bank’s guidance will most likely follow the first documented precedent deal rather than precede it. This is the sequence the gold-backed lending market followed in 2022.

Frequently Asked Questions

Q: Can I currently get a loan from a UAE bank using my premium plate as collateral?

As an off-the-shelf retail banking product, no. No UAE bank publicly advertises plate-backed lending as a standard product category. For HNW clients with existing private banking relationships, bespoke structures are possible under the three pathways described above, most commonly through specialist lenders rather than mainstream banks. The typical minimum transaction size for a bespoke plate-backed facility would be AED 5 million or higher, reflecting the origination costs of a non-standard structure.

Q: What is the structural barrier to plate-backed lending in the UAE?

UAE Federal Decree Law No. 4 of 2020 on Securing Rights in Movable Property excludes from its scope assets recorded in a special register under UAE law. The RTA traffic file is a special register. As a result, a plate cannot be pledged through the standard Emirates Integrated Registries Company (EIRC) framework the way artwork, gold, equipment, or inventory can. This is a legal structure issue, not a market willingness issue. Three workaround pathways are legally viable.

Q: Which is the most likely structure for the first plate-backed loan in the UAE?

The DIFC or ADGM holding company structure (Pathway Two in this article) is the most likely first-deal structure. It provides the cleanest legal security for the lender, isolates the plate from the lender’s onshore balance sheet, and operates under common-law security frameworks that institutional private credit providers are already familiar with. The likely first borrower is a family office or corporate plate portfolio holder rather than an individual, because the SPV costs only amortise at portfolio scale.

Q: What loan-to-value ratio should a plate-backed facility offer?

Substantially more conservative than securities-backed lending. Based on UAE plate market liquidity and secondary-market time-to-sell data, prudent LTVs are: 50–60% for single-digit trophy plates, 55–65% for two-digit ultra-premium, 60–70% for three-digit premium (the sweet spot for this lending category), and 50–60% for four-digit plates on early codes only. Five-digit plates should not be underwritten.

Q: How does the RTA transfer fee structure affect plate-backed lending economics?

Transfer fees are trivial relative to facility sizes. The RTA charges AED 120 to AED 350 per transfer depending on the specific transaction type, as documented in our plate cost of ownership article. On a AED 10 million facility, two transfers (at origination and at maturity) cost AED 240–700 combined, which is immaterial. The fee structure supports rather than constrains the economics of plate-backed lending.

Q: What happens if the borrower defaults on a plate-backed loan?

The answer depends on the pathway. Under the bailment model (Pathway One), the lender already holds the plate and can sell it directly through the RTA to a third-party buyer. Under the DIFC or ADGM SPV structure (Pathway Two), the lender enforces its registered share pledge over the SPV, takes control of the SPV, and liquidates the plate through the SPV’s onshore nominee. Under the dealer-guarantor model (Pathway Three), enforcement operates against the dealer’s general corporate assets, with the plates forming part of that asset base. All three pathways have workable default mechanics.

Q: Would UAE Sharia compliance affect a plate-backed lending product?

Yes, and the pathways accommodate it. The Islamic banking equivalent of Lombard lending, the Tawarruq structure already used by Emirates NBD and ADCB for securities-backed facilities, is adaptable to plate collateral. The underlying commodity trade in the Tawarruq structure can be any Sharia-compliant asset, and plates qualify because they are not intrinsically linked to any prohibited activity. The operational mechanics require a specialist Islamic finance structuring team, but no fundamental Sharia obstacle exists.

Q: How does LicensePlate.ae relate to the plate-backed lending market?

LicensePlate.ae’s role is to provide the market-data layer that institutional plate-backed lending requires. The platform publishes auction results, transaction data, and valuation methodology that a lender’s credit committee can cite. As the plate-backed lending market develops, LicensePlate.ae is positioned to be the reference valuation source that lenders default to for collateral-value determinations, comparable to the role that the Art Market Research Index plays for art-backed lending. See our investment guide for the portfolio construction logic that underpins valuation.

A Final Note on Building Markets Before They Exist

Plate-backed lending in the UAE will emerge. The structural ingredients are present, and the demand conditions are accumulating. What is not yet present is the first deal, the reference valuation, and the regulatory clarity that together convert a category of bespoke transactions into a product line. Each of those three ingredients is achievable within a 24–36 month window under the right execution.

The lender who writes the first publicly documented plate-backed facility in the UAE acquires two things of lasting value. First, a body of structuring experience that no competitor has. Second, the narrative position of having defined the category. Both are meaningful competitive advantages in a UAE private credit market that has grown substantially since the introduction of the Private Credit Fund Rules in 2023, with Mubadala committing over USD 5 billion across multiple international partnerships, Lunate operating at USD 110 billion in alternative assets, and Chimera’s USD 2 billion private credit joint venture with Alpha Wave establishing the model for large-scale UAE-anchored private credit. Against that backdrop, a specialist plate-backed lending programme is a small but defensible niche that a single dedicated firm could own for a decade.

For family offices and UHNW plate owners reading this article, the practical takeaway is that the category is still bespoke. Access to credit against a plate portfolio today requires direct engagement with a specialist lender (likely DIFC-based) on a negotiated structure. The published auction data and the methodology we document in our investment guide and cost of ownership analysis give your lender the valuation basis to build the facility. For portfolio holders exploring succession and generational transfer alongside credit considerations, our inheritance guide documents how plate ownership transfers through the RTA traffic file in ways that directly affect how a lender’s security position survives an ownership change. The LicensePlate.ae plate calculator and live Dubai secondary market listings provide the real-time valuation inputs a credit committee can use as the starting point for any bespoke facility discussion. The path from “interesting question” to “signed facility agreement” is shorter than most UAE HNW clients assume. It just requires the right counterparty and the willingness to structure around the current legal framework rather than waiting for it to change.

For the broader market, the conditions under which plate-backed lending becomes an ordinary product rather than a bespoke transaction are knowable and observable. LicensePlate.ae will continue to publish the market data that makes those conditions easier to satisfy. The first documented deal, whenever it comes, will close faster than the second, and the second faster than the third. This is how markets build.

Delete Comment?

Are you sure you want to delete this comment? This action cannot be undone.

Delete Article?

Are you sure you want to delete this article? This will also delete all comments. This action cannot be undone.